Interest, in the context of a loan, is the cost of borrowing money. It’s essentially a fee that a lender charges a borrower for the privilege of using their funds over a period of time. This fee is calculated as a percentage of the principal loan amount and is paid in addition to the repayment of the original borrowed sum. Understanding interest is fundamental to comprehending any borrowing transaction, from a personal loan for a new car to a business loan for expansion. In the world of finance and economics, interest is a core concept that influences investment decisions, consumer spending, and the overall health of the economy.

The concept of interest is deeply ingrained in our financial systems. Lenders, whether they are banks, credit unions, or individual investors, expect to be compensated for the risk they undertake by lending out their capital. This compensation comes in the form of interest. For borrowers, interest represents the price they pay for immediate access to funds they might not otherwise have. This can be crucial for achieving significant life goals, such as purchasing a home, funding education, or starting a business.

The Mechanics of Interest: How it’s Calculated and Applied

At its core, interest is a mathematical calculation. The most common way interest is expressed and applied is through the Annual Percentage Rate (APR). The APR represents the yearly cost of borrowing, including not just the basic interest rate but also any associated fees. This provides a more comprehensive picture of the true cost of a loan.

Principal and Interest Rate: The Foundation of Calculation

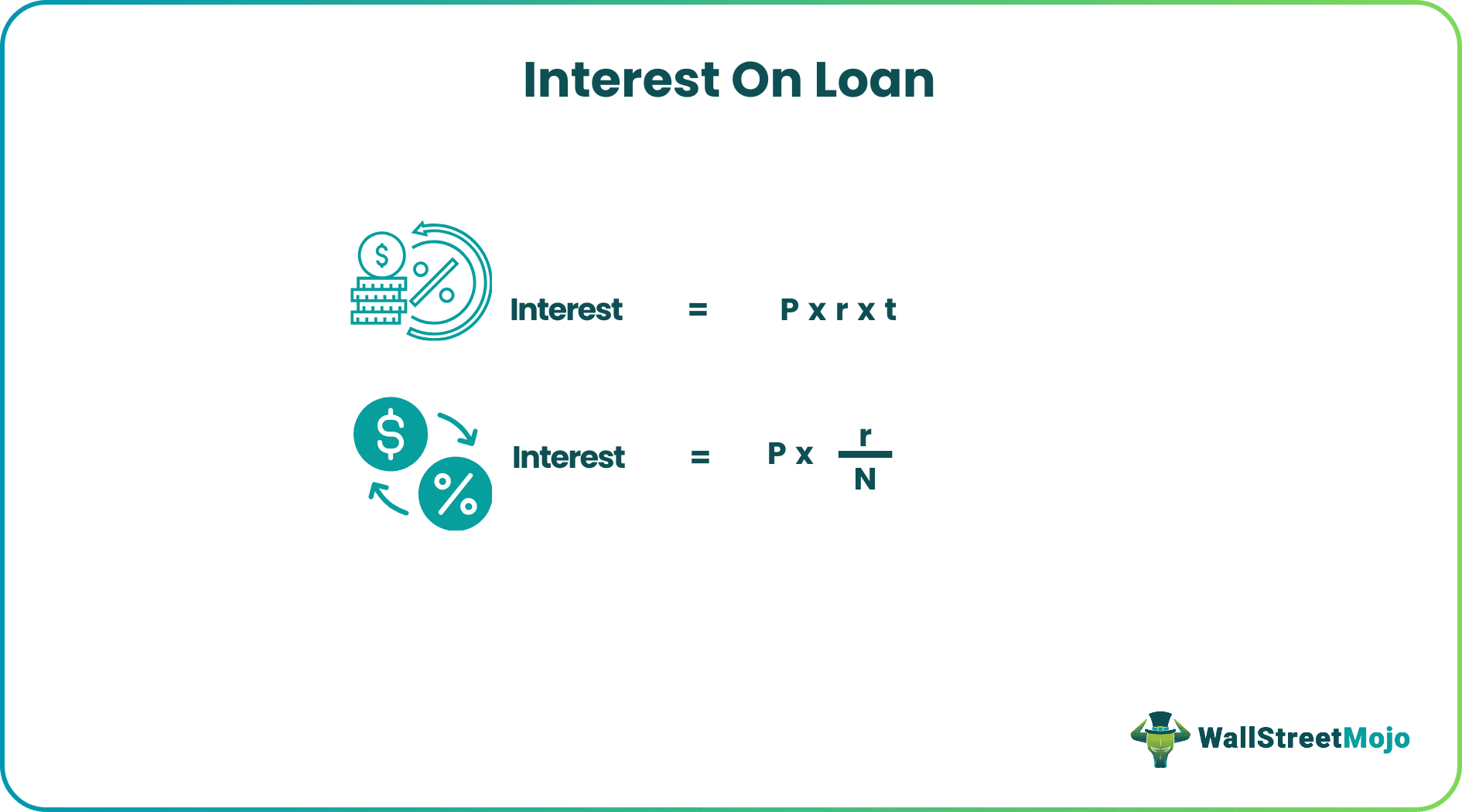

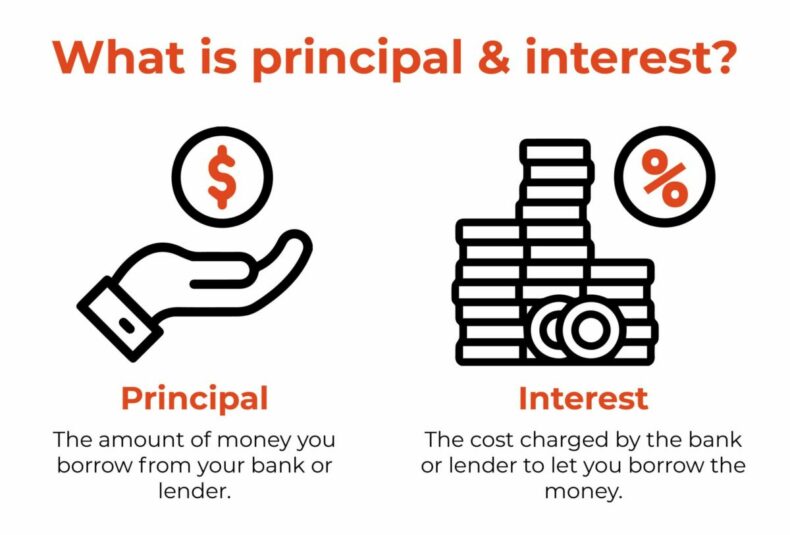

The principal is the initial amount of money borrowed. This is the base figure upon which interest is calculated. The interest rate is the percentage charged on the principal. For example, if you borrow $10,000 at an interest rate of 5% per year, you will owe $500 in interest for that year, assuming no compounding.

Simple vs. Compound Interest: The Power of Time

There are two primary ways interest accrues: simple and compound.

-

Simple Interest: This is calculated only on the original principal amount. If you have a loan with simple interest, the amount of interest you pay each period remains constant. For instance, on a $10,000 loan at 5% simple annual interest, you’d pay $500 in interest each year, regardless of how much of the principal you’ve repaid. While conceptually straightforward, simple interest is less common for most consumer loans.

-

Compound Interest: This is interest calculated on the principal amount and also on the accumulated interest from previous periods. This is often referred to as “interest on interest.” Compound interest can significantly increase the total amount repaid over time, especially for longer-term loans or investments. For example, if you have a $10,000 loan at 5% annual interest compounded annually, in the first year you’d pay $500 interest. In the second year, you’d pay 5% on $10,500 ($525), and so on. The more frequently interest compounds (e.g., monthly, quarterly), the faster the balance grows.

Amortization Schedules: Tracking Repayments Over Time

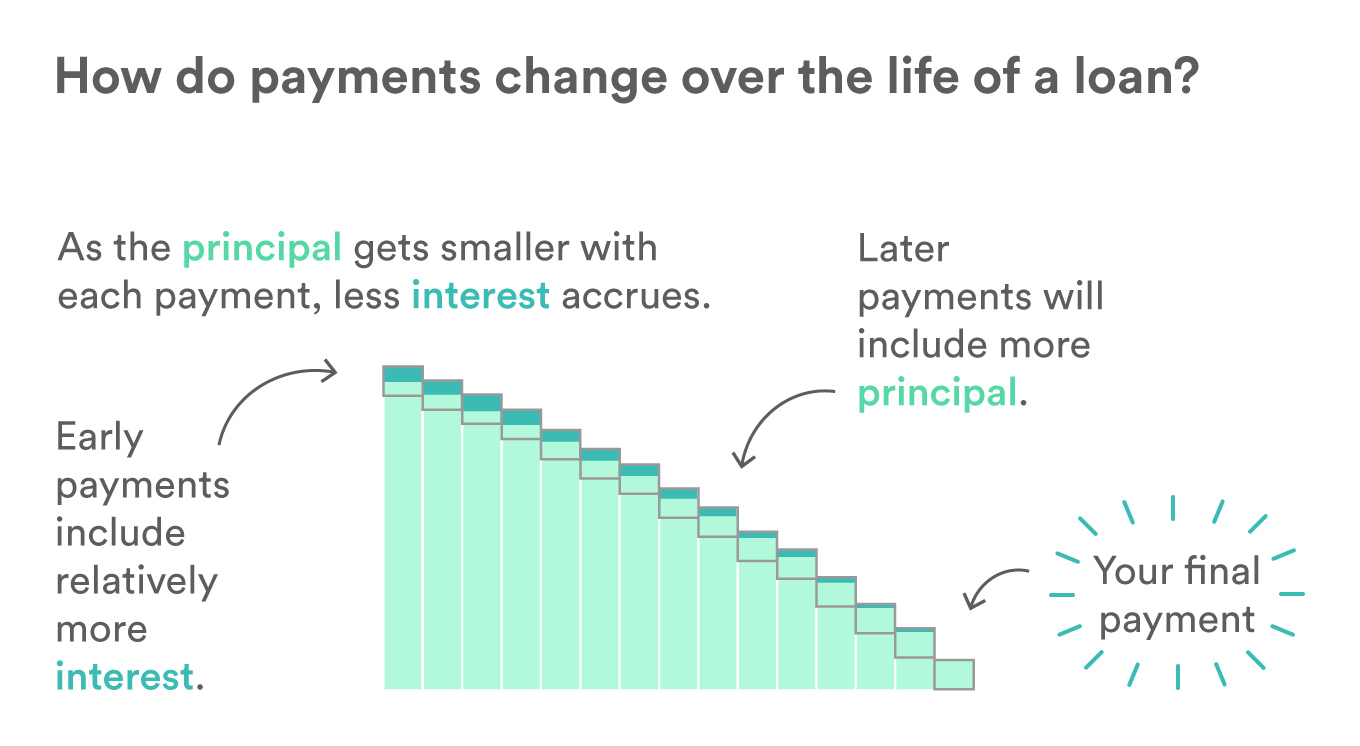

For most installment loans (like mortgages or car loans), interest is paid over the life of the loan through amortization. An amortization schedule details how each loan payment is divided between principal and interest. In the early stages of a loan, a larger portion of each payment goes towards interest, while as you progress through the loan term, a greater portion is applied to reducing the principal balance. This means that over the life of a loan, you will typically pay more in interest than you would if you could pay off the principal faster.

Factors Influencing Loan Interest Rates

The interest rate you are offered on a loan is not arbitrary. It’s a reflection of several key factors that lenders consider to assess risk and determine appropriate compensation.

Borrower’s Creditworthiness: A Key Determinant

One of the most significant factors influencing interest rates is the borrower’s creditworthiness. This is typically assessed through a credit score and a credit report.

-

Credit Score: A numerical representation of your credit history, a credit score (like FICO or VantageScore) indicates how likely you are to repay borrowed money. Higher credit scores generally signal lower risk to lenders, leading to more favorable interest rates. Conversely, lower credit scores suggest a higher risk of default, resulting in higher interest rates or even loan denial.

-

Credit Report: This document provides a detailed history of your borrowing and repayment activities, including past loans, credit card usage, payment timeliness, and any instances of default or bankruptcy. Lenders review this report to gain a deeper understanding of your financial behavior.

Loan Type and Term: Risk and Duration

The type of loan and its term (length of time to repay) also play a crucial role in determining the interest rate.

-

Loan Type: Different loan products carry varying levels of risk. For example, secured loans (backed by collateral, like a mortgage or auto loan) typically have lower interest rates than unsecured loans (like personal loans or credit cards) because the lender has a tangible asset to seize if the borrower defaults.

-

Loan Term: Generally, longer loan terms tend to have higher interest rates. This is because the lender is exposed to risk for a longer period, and there’s an increased chance of unforeseen economic changes or borrower financial difficulties over an extended duration.

Market Conditions and Lender’s Risk Premium

Beyond the borrower’s individual circumstances, broader economic factors and the lender’s specific risk assessment also influence interest rates.

-

Market Interest Rates: The prevailing interest rates in the economy, often influenced by central bank policies (like the Federal Reserve in the US), set a baseline for all lending. When overall market rates are high, loan interest rates will also be higher, and vice-versa.

-

Lender’s Risk Premium: Each lender has its own internal policies and risk tolerance. They will add a risk premium to the base interest rate to account for their specific operational costs, desired profit margins, and their assessment of the overall economic climate.

The Significance of Interest: Economic and Personal Implications

Interest is not merely a financial calculation; it has profound implications for both individuals and the broader economy.

For Individuals: Enabling Goals and Managing Debt

For individuals, understanding interest is essential for making informed financial decisions.

-

Enabling Major Purchases: Loans with interest allow individuals to finance significant purchases like homes, vehicles, or education, which might otherwise be unattainable. This access to capital can dramatically improve one’s quality of life and long-term financial well-being.

-

Debt Management: Properly understanding how interest accrues is critical for effective debt management. Choosing loans with lower interest rates, prioritizing repayment of high-interest debt, and making extra payments can significantly reduce the total cost of borrowing and the time it takes to become debt-free.

For the Economy: Driving Investment and Consumption

Interest rates are a powerful tool for influencing economic activity.

-

Stimulating or Slowing the Economy: Central banks use interest rates to manage inflation and economic growth. Lowering interest rates makes borrowing cheaper, encouraging businesses to invest and consumers to spend, thereby stimulating the economy. Conversely, raising interest rates makes borrowing more expensive, which can help to curb inflation by slowing down spending and investment.

-

Facilitating Capital Allocation: Interest acts as a signal in the economy, directing capital to where it is deemed most productive. Higher interest rates might encourage saving and investment in fixed-income assets, while lower rates might push investors towards riskier assets or consumption.

In conclusion, interest is the fundamental cost of borrowing money, a critical component of any loan. Understanding its mechanics, the factors that influence its rates, and its far-reaching economic and personal implications is paramount for navigating the financial landscape effectively. Whether you are a borrower or a lender, a firm grasp of interest empowers you to make sound financial decisions and achieve your economic objectives.