Understanding the implications of canceling a credit card is crucial for maintaining a healthy financial standing and achieving your long-term financial goals. While the act of canceling may seem straightforward, its ripple effects can be significant, impacting your credit score, your access to future credit, and even your budgeting strategies. This article delves into the multifaceted consequences of closing a credit card account, providing a comprehensive overview to help you make informed decisions.

Impact on Your Credit Score

Canceling a credit card can directly affect your credit score in several ways, primarily related to the factors that credit bureaus consider when calculating your score.

Credit Utilization Ratio

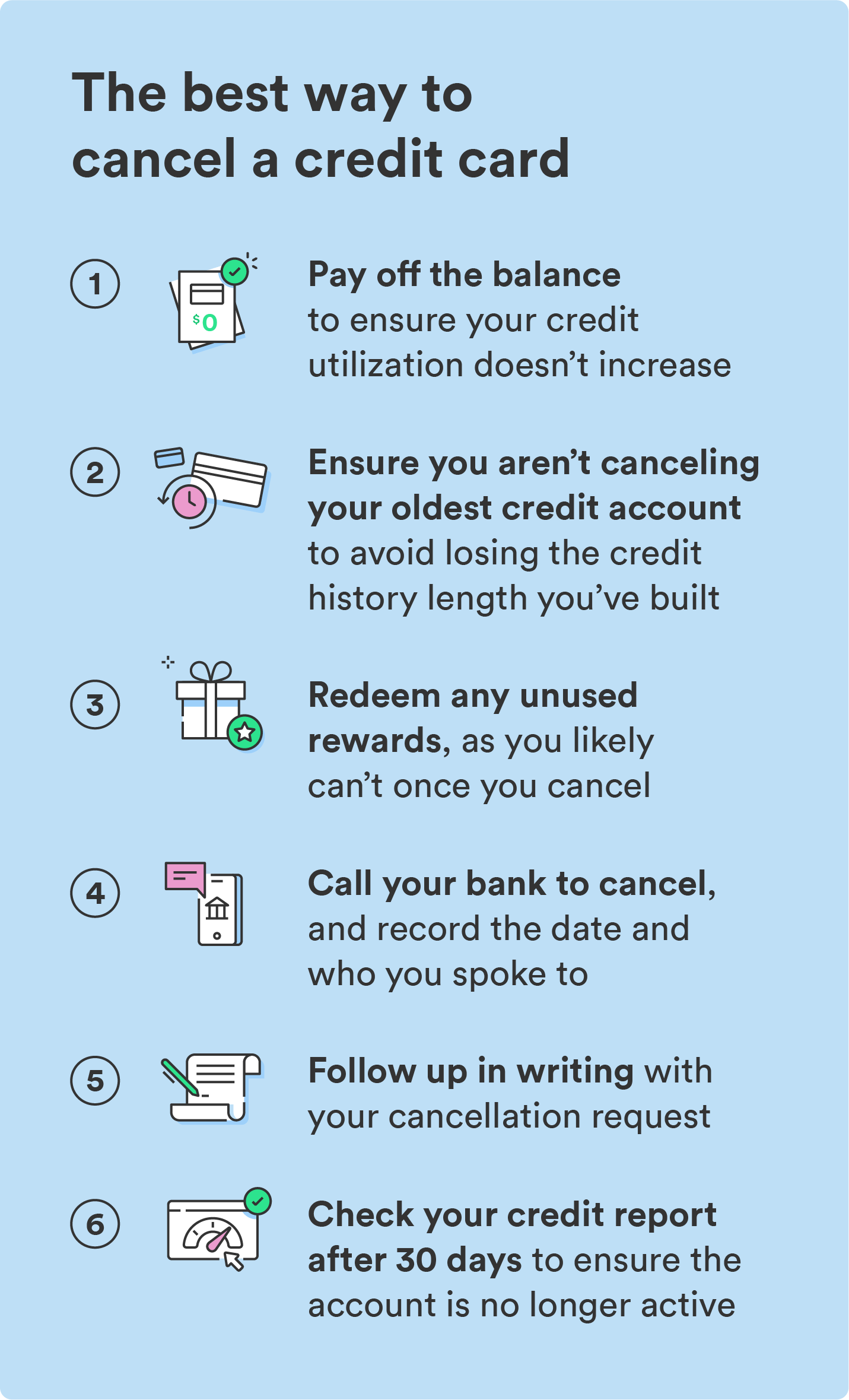

One of the most immediate and significant impacts of canceling a credit card is the effect on your credit utilization ratio. This ratio represents the amount of credit you are currently using compared to your total available credit. For example, if you have two credit cards with a limit of $5,000 each, your total available credit is $10,000. If you carry a balance of $2,000 on one card, your utilization is 20% ($2,000 / $10,000).

When you cancel a credit card, especially one with a significant credit limit, you effectively reduce your total available credit. If you have outstanding balances on your other cards, this reduction in available credit will cause your credit utilization ratio to increase. For instance, if you cancel a card with a $5,000 limit, your total available credit drops to $5,000. If you still owe $2,000 on your remaining card, your new utilization becomes 40% ($2,000 / $5,000), which is a substantial increase. Lenders generally prefer a credit utilization ratio below 30%, and a higher ratio can signal to lenders that you are over-extended and potentially a higher risk, leading to a lower credit score.

Length of Credit History

The length of your credit history is another vital component of your credit score. Responsible management of credit accounts over an extended period demonstrates reliability to lenders. When you cancel a credit card, particularly an older one, you may be shortening the average age of your credit accounts. Credit scoring models favor longer credit histories. If the canceled card was one of your oldest accounts, its closure can disproportionately affect the average age of your credit, potentially lowering your score. This is because the account’s positive payment history and its establishment date will no longer contribute to the overall length of your credit experience.

Credit Mix

While less impactful than utilization and length of history, your credit mix also plays a role in your credit score. Having a variety of credit types, such as installment loans (mortgages, car loans) and revolving credit (credit cards), can be beneficial. Canceling a credit card reduces the diversity of your credit accounts. If credit cards represent a significant portion of your credit mix, closing one may lead to a slightly less diverse profile, which could have a minor negative effect on your score. However, this impact is generally minimal compared to changes in utilization or credit history length.

Loss of Benefits and Perks

Beyond the direct impact on your credit score, canceling a credit card often means forfeiting valuable benefits and rewards that you may have accumulated or could have continued to enjoy.

Rewards Programs

Many credit cards offer rewards programs, such as cashback, travel points, or airline miles. If you have accumulated a significant balance of rewards, canceling the card before redeeming them could result in their forfeiture. It’s crucial to check the terms and conditions of your rewards program before canceling to ensure you redeem all eligible rewards. Some issuers may allow you to transfer rewards to another card with them, or provide a grace period for redemption after account closure, but this is not always the case.

Other Cardholder Benefits

Credit cards often come with a host of additional benefits that can provide significant value. These might include:

- Purchase Protection: This can cover newly purchased items against damage or theft for a specified period.

- Extended Warranty: Some cards extend the manufacturer’s warranty on eligible purchases.

- Travel Insurance: This can encompass trip cancellation/interruption insurance, lost luggage reimbursement, and rental car insurance.

- Concierge Services: High-end cards may offer a concierge service to assist with booking travel, making reservations, or purchasing tickets.

- Airport Lounge Access: Premium travel cards often provide access to airport lounges, offering a more comfortable travel experience.

By canceling the card, you lose access to these benefits, which may have been a primary reason for choosing the card in the first place. It’s essential to weigh the value of these perks against the reasons for canceling before making a decision.

Future Credit Implications

The decision to cancel a credit card can also have ramifications for your ability to obtain credit in the future and the terms under which you can obtain it.

Application Approvals

While canceling a card doesn’t prevent you from applying for new credit, it can influence your approval odds. A reduced credit history length and a potentially higher credit utilization ratio on your remaining cards could make lenders view you as a riskier borrower. This might lead to higher interest rates, lower credit limits, or outright rejections on future credit applications.

Credit Limits

When applying for new credit cards or loans, lenders assess your overall creditworthiness. Having a history of responsible credit management, including keeping older, unused accounts open (even with zero balances), can demonstrate a solid credit foundation. Canceling accounts, especially those with established credit limits, reduces your overall available credit. If you later apply for a significant loan, such as a mortgage, a lower total available credit might be a factor lenders consider, though it’s usually less critical than your income, debt-to-income ratio, and credit score.

Building Credit Over Time

For individuals looking to build or rebuild their credit, strategically managing credit cards is key. Canceling a card, particularly an older one that shows a long history of on-time payments, can hinder the process of demonstrating long-term credit responsibility. It’s often more beneficial to keep older, well-managed accounts open, even if they are not actively used, to contribute positively to your credit history and average age of accounts.

When It Makes Sense to Cancel a Credit Card

Despite the potential downsides, there are circumstances where canceling a credit card is a sound financial decision.

High Annual Fees Without Justified Benefits

If a credit card carries a high annual fee, and you are no longer utilizing the benefits or rewards it offers to offset that cost, it can be a drain on your finances. For example, if you have a premium travel card with a $500 annual fee but no longer travel frequently, the fee is likely not worth the minimal benefits you receive. In such cases, canceling the card can save you money.

Poor Customer Service or Dissatisfaction

Persistent issues with customer service, problematic transaction handling, or a general lack of satisfaction with the card issuer’s policies can be valid reasons to cancel. If a card consistently causes frustration or financial inconvenience due to its management, moving to a provider with better service can be beneficial.

Unmanageable Debt

If a credit card is associated with high-interest debt that you are struggling to manage, canceling it might be part of a larger debt reduction strategy. However, this should be approached with caution. If the cancellation simply removes an account without addressing the underlying spending habits or a repayment plan, it may not solve the core problem and could negatively impact your credit. It is often more advisable to focus on paying down the debt on that card first, perhaps by transferring the balance to a lower-interest card or a debt consolidation loan, before considering cancellation.

Identity Theft Concerns

If you suspect your credit card information has been compromised and are unable to secure the account or the issuer is unresponsive to your concerns, canceling the card may be a necessary step to prevent further fraudulent activity. In such situations, opening a new card with a different issuer is often the best course of action.

Alternatives to Canceling

Before making the decision to cancel, explore alternative options that can help you retain the benefits of a credit card account without incurring unnecessary costs or negative credit impacts.

Downgrading to a No-Annual-Fee Card

Many credit card issuers allow you to downgrade to a no-annual-fee version of the same card. This allows you to keep the account open, preserving your credit history and average age of accounts, without paying an annual fee. You may lose some of the premium rewards and benefits, but it’s often a worthwhile trade-off to maintain your credit profile.

Not Using the Card

If your only concern is that a card is unused, and it has no annual fee, simply stop using it. An inactive card with a good payment history can still positively contribute to your credit score by increasing your total available credit and potentially lengthening your credit history. Just be aware that some issuers may eventually close inactive accounts, usually with advance notice.

Balance Transfer

If the reason for considering cancellation is a high-interest balance, explore balance transfer options. You might be able to transfer the balance to a new credit card with a 0% introductory APR for a promotional period, allowing you to pay down the debt more efficiently without accruing significant interest. This approach should be carefully considered, factoring in any balance transfer fees.

Conclusion

Canceling a credit card is a decision with far-reaching consequences. While it can be a practical step in managing finances when faced with high fees or unmanageable debt, it’s imperative to understand the potential negative impacts on your credit score, including your credit utilization ratio and the length of your credit history. Furthermore, you risk losing valuable rewards and benefits. Before proceeding with a cancellation, thoroughly evaluate your financial situation, consider alternatives such as downgrading or balance transfers, and consult your card issuer’s terms and conditions. A well-informed approach will help you make the best decision for your long-term financial health.