Understanding the nuances of retirement savings plans is crucial for anyone looking to secure their financial future. While the terms “401(k)” and “403(b)” are often used interchangeably, and both offer tax advantages for retirement savings, they cater to different types of employees and have distinct features. This article aims to demystify these two popular employer-sponsored retirement plans, highlighting their key differences and similarities to empower you to make informed decisions about your retirement strategy.

The Foundational Similarities: Pillars of Retirement Security

At their core, both 401(k) and 403(b) plans serve the fundamental purpose of enabling individuals to save for retirement on a tax-advantaged basis. This shared foundation means they offer significant benefits that far outweigh individual savings accounts for long-term wealth accumulation.

Tax Advantages: The Primary Appeal

The most compelling reason for the widespread adoption of both 401(k) and 403(b) plans is their inherent tax advantages. These plans allow contributions to grow tax-deferred, meaning you don’t pay taxes on the investment earnings each year.

Pre-Tax Contributions (Traditional Plans)

For traditional 401(k) and 403(b) plans, contributions are made on a pre-tax basis. This means the money you contribute is deducted from your taxable income in the year you earn it, effectively lowering your current tax bill. For instance, if you earn $60,000 and contribute $6,000 to your 401(k) or 403(b), your taxable income for that year is reduced to $54,000. This immediate tax relief can be a significant financial benefit.

Tax-Deferred Growth

Once the money is in your retirement account, it can grow through investments without being subject to annual taxes on dividends, interest, or capital gains. This compounding effect, where your earnings also generate earnings, is a powerful engine for wealth creation over the long term. The longer your money stays invested and compounds, the more significant the impact of this tax-deferred growth.

Taxation on Withdrawal

The tax advantage shifts in retirement. When you withdraw money from a traditional 401(k) or 403(b) in retirement, both your contributions and earnings are taxed as ordinary income. This is often beneficial because individuals are typically in a lower tax bracket during retirement than during their peak earning years.

Catch-Up Contributions

For individuals nearing retirement age, both plan types offer “catch-up” contributions. This allows those aged 50 and over to contribute an additional amount beyond the standard annual contribution limit. This provision is designed to help workers who may have started saving later in their careers or who want to bolster their savings in their final working years. The specific catch-up contribution amount is set by the IRS and can be adjusted annually.

Contribution Limits

The IRS sets annual limits on how much individuals can contribute to their 401(k) and 403(b) plans. These limits are designed to prevent overly aggressive tax deferrals and are subject to change each year. While the core limits are often the same for both plan types, there can be slight variations or nuances based on specific plan rules.

The Divergent Paths: Who Offers What?

The most significant differentiator between a 401(k) and a 403(b) lies in the type of employer that offers them. This distinction dictates the pool of potential participants and, consequently, the regulatory frameworks and investment options that may be available.

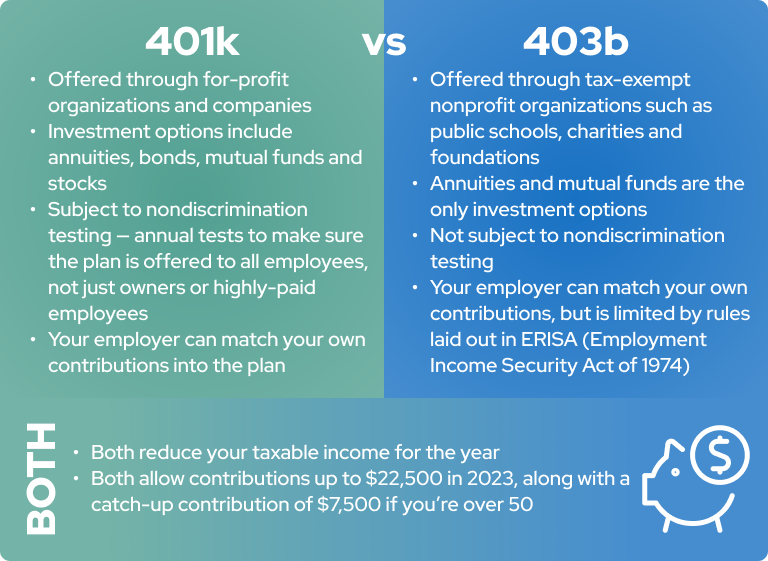

401(k) Plans: The Corporate Realm

The 401(k) plan is predominantly offered by for-profit private sector employers. It’s the flagship retirement savings vehicle for companies of all sizes, from small businesses to large multinational corporations. The “401(k)” designation comes from the section of the Internal Revenue Code that governs these plans.

Employer Sponsorship

Companies that offer 401(k) plans do so as a benefit to their employees, encouraging saving and providing a way to attract and retain talent. The employer often plays an active role in administering the plan, selecting investment options, and sometimes offering matching contributions.

Investment Options

The investment choices within a 401(k) plan are typically curated by the employer or their chosen plan administrator. These usually include a range of mutual funds, exchange-traded funds (ETFs), and sometimes company stock. The breadth and quality of these options can vary significantly from one employer to another.

403(b) Plans: The Non-Profit and Public Sector Domain

In contrast, 403(b) plans are offered by tax-exempt organizations, primarily in the public education sector and certain non-profit organizations. This includes:

- Public schools and universities: Teachers, administrators, and support staff in public school districts and state colleges/universities often have access to 403(b) plans.

- Hospitals and healthcare organizations: Many non-profit hospitals and healthcare systems offer 403(b) plans to their employees.

- Churches and religious organizations: Employees of qualifying religious institutions can also participate in 403(b) plans.

- Certain other tax-exempt organizations: A broader category of non-profits that meet specific IRS criteria can also sponsor 403(b) plans.

Employer Sponsorship in the Non-Profit Sector

Similar to 401(k)s, 403(b) plans are offered by these organizations as an employee benefit. The administration and investment selection are handled by the sponsoring organization, though the landscape can sometimes be more fragmented due to the diversity of these institutions.

Investment Options in 403(b) Plans

Historically, 403(b) plans were often characterized by a more limited set of investment options, primarily annuities and mutual funds. However, in recent years, many 403(b) plans have expanded their offerings to include a broader array of investment choices, bringing them closer to the typical 401(k) offerings. Annuities, in particular, have been a common feature of 403(b) plans, offering a guaranteed income stream in retirement.

Key Distinctions in Plan Features and Regulations

Beyond who offers the plan, there are several other important differences in how 401(k)s and 403(b)s operate, particularly concerning regulations, investment choices, and administrative considerations.

Regulatory Oversight and ERISA

A significant distinction lies in the regulatory framework governing these plans.

401(k)s and ERISA

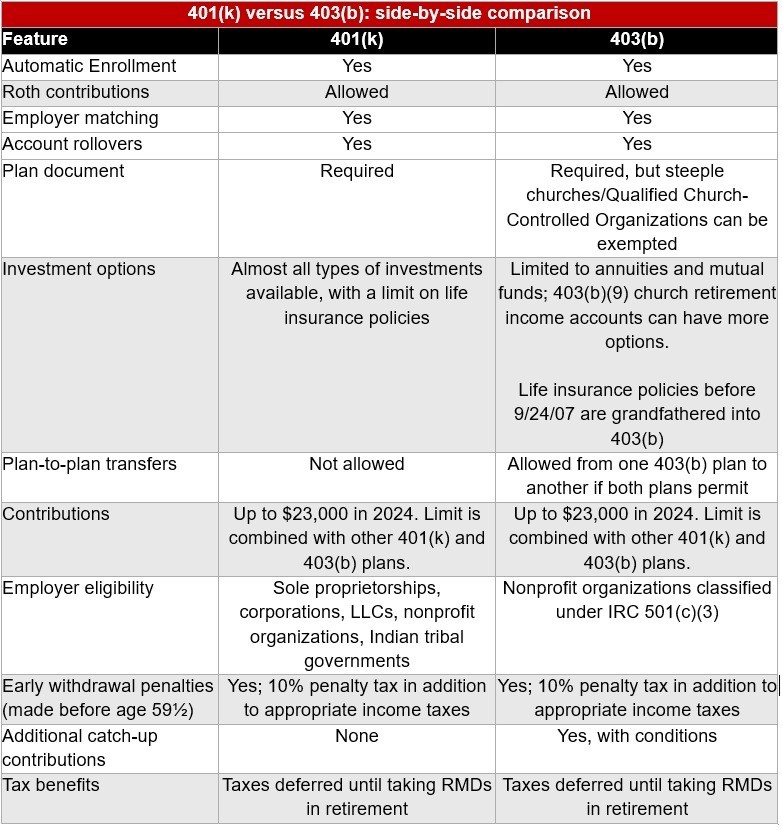

Most 401(k) plans are subject to the Employee Retirement Income Security Act of 1974 (ERISA). ERISA is a comprehensive federal law that sets minimum standards for most voluntarily established retirement and health plans in the private industry to provide protection for individuals in these plans. ERISA imposes fiduciary responsibilities on plan sponsors and administrators, requiring them to act in the best interest of plan participants. This includes prudent investment management, proper plan administration, and timely disclosure of plan information.

403(b)s and ERISA

While many 403(b) plans are also subject to ERISA, there are exceptions, particularly for governmental plans and some church plans. Plans offered by public schools and state universities, for instance, are typically not subject to ERISA. This can mean that the level of fiduciary protection and regulatory oversight may differ. However, even non-ERISA 403(b) plans are subject to various IRS regulations.

Investment Vehicles

While the lines have blurred, historical and common differences in investment vehicles exist.

Annuities in 403(b) Plans

As mentioned, annuities have traditionally been a more prevalent investment option within 403(b) plans. Annuities are insurance contracts that can provide a guaranteed stream of income during retirement. They can come with various features, including death benefits and riders, but often come with higher fees and surrender charges than typical mutual funds.

Mutual Funds and ETFs in 401(k) Plans

401(k) plans have generally focused on a broader array of mutual funds and, more recently, ETFs as the primary investment vehicles. These are typically selected by plan administrators based on performance, diversification, and expense ratios.

Administrative Complexity and Costs

The administrative structure and associated costs can also vary.

Plan Administration

401(k) plans, particularly those offered by larger corporations, often have sophisticated administrative platforms managed by third-party administrators (TPAs) or recordkeepers. These providers handle everything from payroll deductions to participant statements and compliance.

403(b) Administration

403(b) administration can sometimes be more fragmented. In some cases, multiple vendors may offer investment products to employees within the same organization, requiring individuals to navigate different platforms. This can sometimes lead to higher administrative costs passed on to participants, although efforts are underway to streamline these processes.

Roth Options and Other Considerations

Both plan types have evolved to offer additional features and flexibility.

Roth Contributions: Tax-Free Withdrawals in Retirement

Both 401(k) and 403(b) plans now commonly offer a “Roth” option.

Roth 401(k) and Roth 403(b)

With Roth contributions, you pay taxes on your contributions in the year you make them, similar to a Roth IRA. However, the significant advantage is that qualified withdrawals of both contributions and earnings in retirement are tax-free. This can be a highly attractive option for individuals who expect to be in a higher tax bracket in retirement than they are during their working years.

Employer Matching Contributions

Employer matching is a common feature of both plan types, acting as a powerful incentive for employees to save. An employer might match a certain percentage of an employee’s contribution up to a specific limit. For example, an employer might match 50% of employee contributions up to 6% of their salary. This “free money” can significantly boost retirement savings.

Loan Provisions

Many 401(k) and 403(b) plans allow participants to take loans against their vested account balance. While this can provide access to funds in an emergency, it’s generally advisable to avoid borrowing from your retirement savings due to potential tax implications and the loss of potential investment growth.

Rollover Options

When you leave an employer, you typically have the option to roll over your 401(k) or 403(b) balance into an IRA or your new employer’s retirement plan (if they offer one). This allows your retirement savings to continue growing without interruption.

Conclusion: Choosing the Right Path for Your Retirement

While the underlying goal of encouraging retirement savings is the same, the distinction between a 401(k) and a 403(b) hinges on the type of employer offering the plan. For-profit businesses offer 401(k)s, while non-profits and public sector entities typically provide 403(b)s.

Understanding these differences is crucial. If you’re employed by a public school or a non-profit hospital, you’ll likely be navigating a 403(b). If you work for a technology company or a retail giant, a 401(k) is probably on the table. The core benefits of tax advantages, potential employer matches, and long-term growth are present in both. However, the specific investment options, regulatory oversight, and administrative nuances can vary. Always take the time to understand the specifics of your employer’s plan, review the investment choices, and consider consulting with a financial advisor to ensure your retirement savings strategy is robust and aligned with your long-term financial goals.