The Modern Dilemma: Navigating Digital Security When Memory Fails

In an increasingly digital financial landscape, the debit card Personal Identification Number (PIN) remains a cornerstone of transaction security. Yet, in an era saturated with passwords, passcodes, and biometric authentications, forgetting a PIN is a common, albeit frustrating, occurrence. While seemingly a simple lapse of memory, the challenge of a forgotten PIN underscores broader themes in Tech & Innovation: the evolving balance between security and user convenience, the development of robust FinTech solutions, and the ongoing push towards more intelligent, resilient authentication systems. Understanding the technological pathways available when this happens is crucial for maintaining financial fluidity and protecting your assets.

The issue of a forgotten PIN is not merely a personal inconvenience; it highlights the critical role of user-centric design in financial technology. Banks and financial institutions continually invest in innovative solutions to streamline account management while upholding stringent security protocols. This delicate dance informs everything from the architecture of mobile banking applications to the implementation of AI-driven customer support. For the individual, navigating this technological ecosystem efficiently can transform a potential crisis into a minor hurdle, demonstrating the power of modern FinTech in resolving common pain points.

Leveraging Digital Banking Innovations for PIN Recovery

When a debit card PIN slips from memory, the first and most technologically advanced recourse is often through your bank’s digital channels. Financial institutions have poured significant resources into developing sophisticated online portals and mobile applications that empower users with a range of self-service options, including PIN management. This represents a significant shift from the past, where such issues almost invariably required an in-person visit or a lengthy phone call.

Online Banking Portals

Most major banks offer comprehensive online banking platforms accessible via web browsers. These portals are secured with multi-factor authentication (MFA), often involving a combination of passwords, security questions, and one-time passcodes sent to a registered mobile device or email. Once authenticated, users can typically navigate to a “Card Services” or “Account Management” section. Here, innovative features are increasingly common:

- PIN Reminder Request: Some banks allow you to request a reminder of your existing PIN. This isn’t usually the PIN itself, but rather a secure mail delivery of the PIN to your registered address. This process leverages secure digital communication to initiate a physical mail delivery, ensuring the PIN is not transmitted insecurely over digital channels. The technology behind this involves encrypted databases and automated postal service integration.

- PIN Reset/Change: A more direct approach is often a PIN reset or change option. This feature is heavily fortified with security protocols, often requiring further verification steps beyond the initial login. This might include answering additional security questions, entering a temporary code generated by the bank, or even speaking with a live agent via a secure chat interface embedded within the portal. The underlying technology ensures that only the legitimate cardholder can authorize such a critical change, often involving real-time identity verification algorithms.

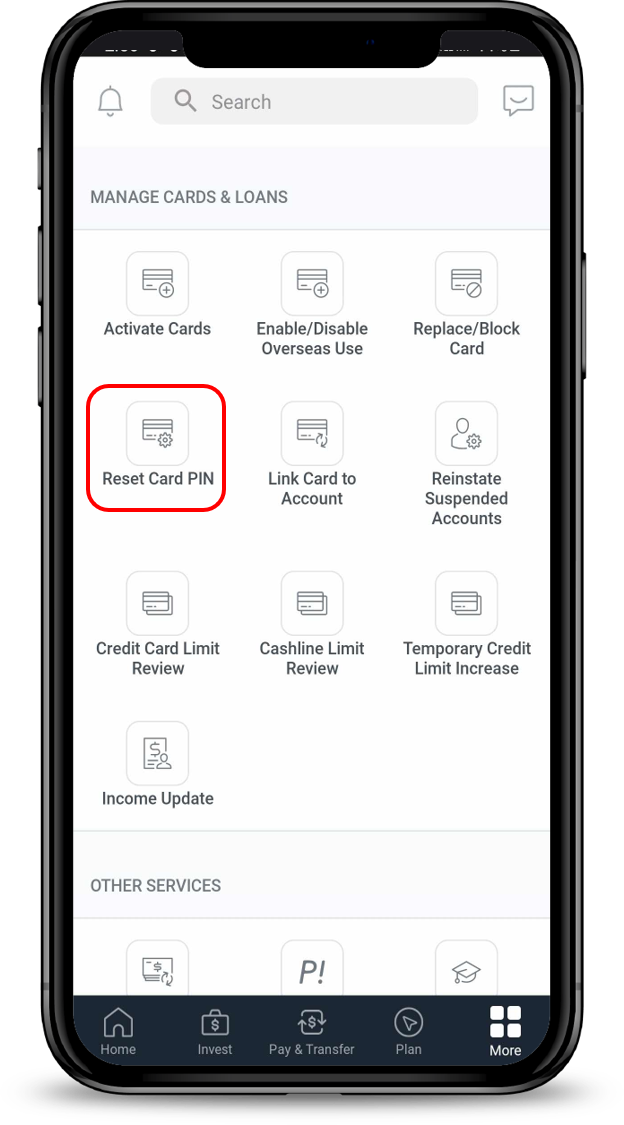

Mobile Banking Applications

Mobile banking apps represent a frontier of FinTech convenience. Engineered for on-the-go access, these applications integrate advanced security features like biometric authentication (fingerprint or facial recognition) for login, making access both swift and secure. Within these apps, PIN management is often even more streamlined than on desktop portals:

- Instant PIN View (Limited): A growing number of mobile banking apps offer a feature allowing users to securely view their PIN within the app. This is typically protected by an additional layer of authentication, such as re-entering your app password, using biometric data again, or a one-time passcode. The technology facilitating this ensures that the PIN is decrypted and displayed only momentarily and never stored locally on the device in an unencrypted form.

- Mobile PIN Reset/Change: Similar to online portals, mobile apps provide functionality to reset or change your PIN. This process is equally secure, often prompting for re-authentication using biometrics or a dedicated app PIN. The convenience of doing this anytime, anywhere, underscores the innovative power of mobile-first banking. This capability relies on robust API integrations with the bank’s core systems, ensuring real-time updates and secure data exchange.

Advancements in Authentication: Beyond the Traditional PIN

While PINs remain prevalent, the broader realm of Tech & Innovation is actively exploring and deploying alternatives and enhancements to traditional authentication. The challenge of a forgotten PIN is, in many ways, driving the accelerated adoption of these newer technologies, aiming to mitigate such issues entirely.

Biometric Authentication

Biometrics offer a compelling solution to the PIN dilemma by replacing knowledge-based authentication with inherent user characteristics. Fingerprint scanners, facial recognition, and iris scans are already common features on smartphones and are increasingly integrated into payment terminals and ATMs.

- Seamless Transactions: Imagine a future where your face or fingerprint is your sole authentication for a debit card transaction, rendering a numerical PIN obsolete. This vision is rapidly becoming a reality, particularly with contactless payment systems.

- Enhanced Security: Biometric data is inherently harder to steal or replicate than a PIN. Advanced liveness detection and anti-spoofing technologies, often leveraging AI and machine learning, make these systems remarkably secure, significantly reducing the risk associated with forgotten or compromised PINs.

- Integration with FinTech: The integration of biometric sensors into payment hardware and mobile devices is a prime example of FinTech innovation simplifying user experience while fortifying security.

AI and Machine Learning in Fraud Prevention and Account Access

Artificial Intelligence (AI) and Machine Learning (ML) are silently revolutionizing how financial institutions manage security and customer support, directly impacting scenarios like forgotten PINs.

- Intelligent Chatbots and Virtual Assistants: Many banks now deploy AI-powered chatbots on their websites and within mobile apps. These virtual assistants can guide users through the PIN recovery process, answer common questions, and even initiate secure calls with human agents when necessary. Their ability to understand natural language and provide instant, relevant information significantly improves the user experience.

- Adaptive Authentication: AI algorithms continuously analyze user behavior and transaction patterns. If a login attempt or PIN reset request deviates from typical behavior, the system can automatically trigger additional verification steps, like sending a security code to a registered device or prompting for specific historical transaction details. This adaptive security framework helps prevent fraudulent PIN resets even if some personal information has been compromised.

- Fraud Detection and Prevention: Beyond PIN recovery, AI is critical in identifying and preventing unauthorized access attempts. By learning normal user patterns, AI can flag suspicious activity related to account access or PIN changes, alerting both the bank and the cardholder to potential fraud before it escalates.

Future-Proofing Your Financial Access: Best Practices and Emerging Tech

Beyond reactive measures, Tech & Innovation also focuses on proactive strategies to prevent the inconvenience of a forgotten PIN. While not always directly related to advanced drone technology, the principles of intelligent systems, autonomous processes, and robust data management from that field find parallels in personal finance security.

Secure PIN Management Practices

- Digital Wallets and Tokenization: Adopting digital wallets (like Apple Pay, Google Pay, Samsung Pay) significantly reduces reliance on physical cards and PINs for in-store transactions. These platforms use tokenization, replacing your actual card number with a unique, encrypted token for each transaction, enhancing security. While some still require a device PIN/biometric for access, it’s a step away from the debit card PIN itself.

- Password Managers: While primarily for online accounts, robust password managers can securely store PINs alongside other credentials, encrypted and accessible only through a master password or biometric authentication. This is a personal tech innovation that helps manage digital clutter.

- Regular Review of Bank Security Features: Financial institutions continually update their security protocols and user interfaces. Regularly reviewing your bank’s website or app for new features related to PIN management, biometric login options, and security alerts ensures you leverage the latest protective measures.

The Road Ahead: Seamless and Invisible Security

The future of financial access, driven by innovation, points towards increasingly seamless and even “invisible” security. Technologies like continuous authentication, where systems constantly verify user identity based on behavior, location, and device patterns, could eventually make discrete PINs or even explicit biometric prompts less frequent. Distributed Ledger Technology (DLT), while still nascent in retail banking, holds promise for secure, immutable record-keeping that could further enhance identity verification processes.

In essence, forgetting a debit card PIN, while an inconvenience, serves as a real-world reminder of the vital interplay between human memory and technological solutions. The sophisticated digital infrastructure, innovative FinTech offerings, and emerging security paradigms developed within the broader Tech & Innovation sphere are not just about recovering access; they are about building a more secure, intuitive, and resilient financial ecosystem for everyone.