Understanding the Basics of Social Security Tax Withholding

Social Security tax, often referred to as FICA (Federal Insurance Contributions Act) tax, is a mandatory payroll deduction that funds retirement, disability, and survivor benefits for eligible individuals. Understanding how this tax is withheld is crucial for both employees and employers to ensure accurate payroll processing and compliance with federal regulations. This deduction is a significant portion of an individual’s gross pay, and its impact on net pay warrants a clear and comprehensive understanding.

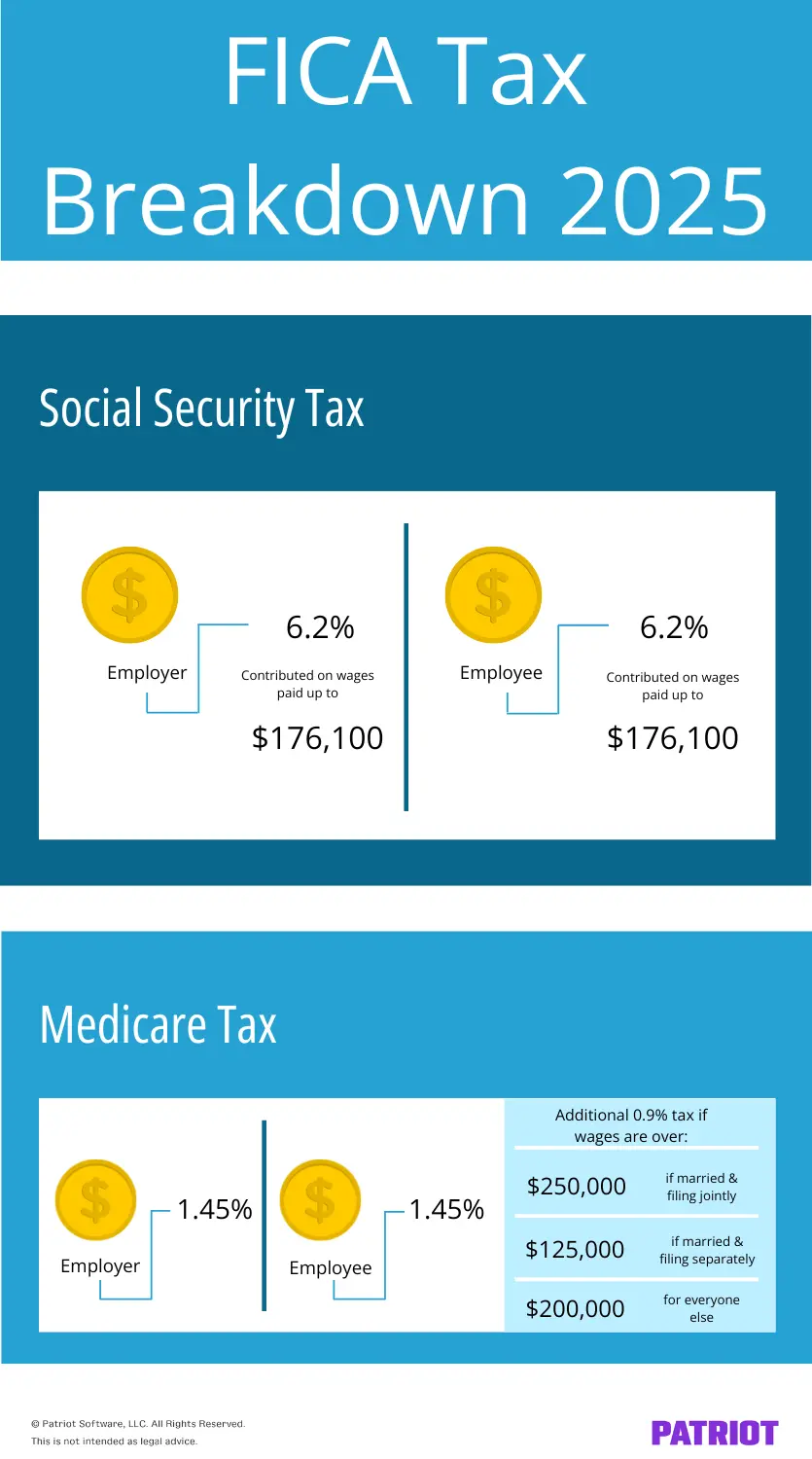

The FICA Tax Structure

The FICA tax is composed of two distinct components: Social Security and Medicare. For employees, the Social Security portion is currently set at 6.2% of gross wages, up to an annual wage base limit. The Medicare portion is 1.45% of all gross wages, with no wage limit. Together, this results in a combined employee contribution of 7.65% on earnings up to the Social Security wage base. Employers are required to match these contributions, effectively doubling the amount sent to the Social Security Administration (SSA) and the Centers for Medicare & Medicaid Services (CMS).

Social Security Tax Rate and Wage Base

The Social Security tax rate has remained relatively stable over the years, though adjustments to the wage base limit are made annually to account for inflation. This limit is the maximum amount of earnings subject to Social Security tax in a given year. Once an individual’s earnings reach this threshold, no further Social Security tax is withheld for the remainder of the calendar year. This provision means that higher earners contribute a smaller percentage of their total income to Social Security compared to lower earners.

Medicare Tax Rate and its Unlimited Application

Unlike the Social Security tax, the Medicare tax is applied to all earnings, regardless of the amount. This ensures that all workers contribute to the Medicare program, which funds hospital insurance and medical insurance for individuals aged 65 and older, as well as for younger people with certain disabilities. The consistent application of the Medicare tax helps to maintain the financial stability of this vital healthcare program.

How Social Security Tax is Withheld from Paychecks

The withholding of Social Security tax is a straightforward process managed by employers through their payroll systems. Every pay period, the employer calculates the employee’s taxable wages and applies the applicable FICA tax rates. The withheld amounts are then remitted to the relevant government agencies.

Employee’s Responsibilities and Information

Employees typically do not need to actively do anything to have Social Security tax withheld, as it is an automatic deduction based on their employment status. However, it is essential for employees to ensure their tax information is accurate, particularly when starting a new job. This includes providing their Social Security number (SSN) correctly on tax forms like the W-4, which is used by employers to determine the correct amount of tax to withhold from wages. An incorrect SSN can lead to issues with tracking contributions and receiving benefits in the future.

Employer’s Role in Withholding and Remittance

Employers play a critical role in the Social Security tax system. They are responsible for accurately calculating, withholding, and remitting the FICA taxes to the IRS. This involves maintaining up-to-date payroll software that reflects the current wage base limits and tax rates. Employers must also file quarterly employment tax returns (Form 941) and an annual return (Form 940) to report the taxes withheld and paid. Failure to comply with these obligations can result in significant penalties and interest.

Understanding Your Paystub and Withholdings

A paystub is a vital document that details an employee’s earnings, deductions, and net pay. Examining your paystub regularly can help you verify that the correct amount of Social Security tax has been withheld and understand how it impacts your take-home pay.

Identifying Social Security Tax on Your Paystub

On most paystubs, Social Security tax withholding is clearly itemized. You will typically see a line item labeled “Social Security Tax,” “OASDI” (Old-Age, Survivors, and Disability Insurance), or “FICA-SS.” The amount withheld will be a percentage of your gross taxable wages for that pay period, up to the annual limit. It is important to differentiate this from the Medicare tax, which may be listed separately as “Medicare Tax” or “FICA-Med.”

The Impact of Social Security Withholding on Net Pay

The Social Security tax deduction directly reduces an employee’s net pay, meaning the amount of money they receive after all withholdings. While this reduction is necessary for future benefits, it is important for individuals to budget accordingly. Understanding the exact amount of Social Security tax withheld can help in financial planning and ensuring that immediate financial needs are met while still contributing to long-term security.

Exceptions and Special Circumstances in Social Security Tax Withholding

While the general rules for Social Security tax withholding apply to most employees, there are certain exceptions and special circumstances that individuals should be aware of. These can affect how much tax is withheld or whether it is withheld at all.

Non-Resident Aliens and Social Security Tax

The treatment of Social Security tax for non-resident aliens can be complex and often depends on their visa status and the length of their stay in the United States. Generally, non-resident aliens are exempt from Social Security and Medicare taxes if they are in the U.S. on an F, J, M, or Q visa and are performing services to carry out the purpose of their visa. However, there are specific rules and durations of exemption, and it is crucial for both the non-resident alien and their employer to consult IRS guidelines or a tax professional to ensure compliance.

Self-Employment Tax and its Relation to Social Security

Individuals who are self-employed are not subject to FICA tax withholding from an employer. Instead, they are responsible for paying self-employment tax, which covers both the employee and employer portions of Social Security and Medicare taxes. This tax is calculated on net earnings from self-employment and is reported on Schedule SE of Form 1040. The self-employment tax rate is 15.3% (12.4% for Social Security up to the annual limit, and 2.9% for Medicare with no limit). While this seems higher than the employee’s FICA rate, it represents the combined contribution.

Military Service and Social Security Contributions

Active duty military personnel also contribute to Social Security. Their base pay is subject to FICA tax withholding, just like civilian employees. For members of the uniformed services, these contributions are credited to their Social Security earnings record, and they are eligible for benefits based on their service. This ensures that military service contributes to the individual’s future Social Security eligibility.

Maximizing Your Social Security Benefits

Understanding Social Security tax withholding is the first step towards a secure retirement. The taxes you pay throughout your working life contribute directly to your future benefits. Beyond simply withholding, there are strategies and considerations that can help you maximize the benefits you receive.

Social Security Wage Base and its Long-Term Impact

The annual Social Security wage base limit directly impacts the total amount of Social Security tax paid over a career. For individuals who consistently earn above this limit, reaching it each year means their Social Security contributions plateau. This has implications for their eventual benefit calculation. While the Medicare tax continues indefinitely, the Social Security portion is capped. Understanding this cap helps in long-term financial planning and estimating future Social Security income.

The Importance of Accurate Record-Keeping for Benefits

The Social Security Administration maintains a record of your earnings throughout your working life. This record is used to calculate your retirement, disability, and survivor benefits. It is essential to ensure that your earnings are reported accurately. You can access your earnings record by creating an account on the SSA website and viewing your Statement. Periodically reviewing this statement can help identify any discrepancies and allow you to take corrective action promptly.

Planning for Retirement and Social Security Income

Social Security is designed to be a foundation for retirement income, not the sole source. Understanding your estimated Social Security benefits, which can be found on your annual Social Security Statement, is a critical component of retirement planning. This estimate is based on your earnings history and the assumption that you will continue earning at a similar rate. Adjusting your savings and investment strategies based on this estimate helps ensure a comfortable and financially secure retirement. Knowing what Social Security tax is withheld provides clarity on one piece of this crucial retirement puzzle.