In the rapidly evolving landscape of aerial technology, high-end remote sensing and mapping drones represent more than just flight hardware; they are significant capital assets. For businesses specializing in geospatial data, precision agriculture, or industrial inspection, understanding the financial lifecycle of these machines is as critical as mastering their flight controllers. When tax season or fiscal year-end reporting arrives, the question of “what line is prior year depreciation” becomes a central focus for fleet managers and CTOs alike. Within the realm of tech and innovation, managing the depreciation of sophisticated equipment like LiDAR-equipped UAVs, multispectral sensors, and autonomous mapping platforms requires a blend of accounting precision and technological foresight.

The Financial Landscape of Advanced Mapping and Remote Sensing Tech

The acquisition of remote sensing technology often involves a substantial upfront investment. Unlike consumer quadcopters, professional-grade mapping drones equipped with Real-Time Kinematic (RTK) positioning, thermal imaging, or hyper-spectral sensors can cost tens of thousands of dollars. Because these tools have a high initial cost and a predictable (albeit short) functional lifespan due to the pace of innovation, they are treated as depreciable assets rather than simple operating expenses.

Defining the Professional Drone as a Business Asset

In the eyes of financial regulators and tax authorities, a drone used for remote sensing is classified as “5-year property” under systems like the Modified Accelerated Cost Recovery System (MACRS). This classification recognizes that while a drone might physically last longer, its technological relevance in the “Tech & Innovation” sector often diminishes after five years as newer, more efficient sensors and AI-driven processing capabilities emerge.

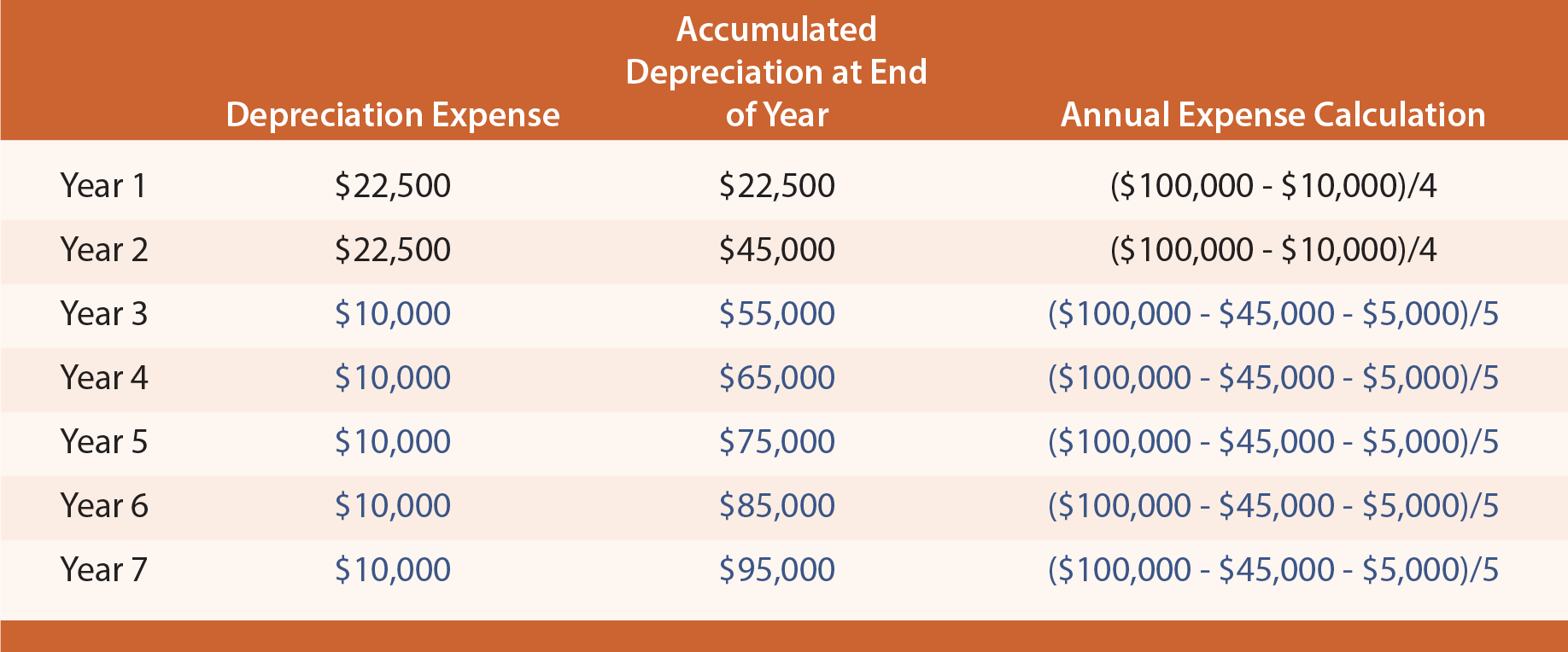

Prior year depreciation refers to the cumulative amount of value that has been written off in previous reporting periods. For a mapping firm, keeping an accurate record of this figure is essential for determining the current “book value” of their fleet. If you are operating a fleet of autonomous mapping drones, the prior year depreciation is typically found on the depreciation schedule of your tax return, specifically on Form 4562, Line 17, for assets placed in service in previous years.

The Role of Rapid Technological Obsolescence

In the tech and innovation niche, depreciation isn’t just a tax strategy; it’s a reflection of the innovation curve. A drone purchased three years ago for remote sensing might still be flight-worthy, but if its sensor resolution or AI obstacle avoidance systems have been eclipsed by two generations of newer technology, its market value drops faster than its physical wear would suggest. This “functional obsolescence” is why professional drone operators must be meticulous about tracking prior year depreciation. It allows a business to understand when the tax benefits of an older asset have been exhausted, signaling that it may be time to reinvest in newer, more autonomous hardware.

Asset Tracking and the Role of Depreciation in Tech Innovation

To maintain a competitive edge in mapping and remote sensing, firms must continuously rotate their hardware. The technical complexity of these systems—incorporating GPS, IMUs, and sophisticated data-links—means that maintenance costs can rise as the asset ages. Depreciation helps offset these costs by reducing the business’s taxable income, effectively “funding” the next generation of technological adoption.

Navigating Form 4562 for Drone Fleets

When addressing the specific question of “what line” to use, it is important to distinguish between new acquisitions and existing inventory. For most drone-based tech companies, “Prior Year Depreciation” for assets already in use is reported on Line 17 of IRS Form 4562. This line serves as the catch-all for MACRS deductions for assets placed in service in tax years beginning before the current year.

However, the “R” in the original query often points toward “Recovery” property or specific “Remote” sensing categories in internal accounting ledgers. If your firm uses specialized software for asset management, the “R” might also refer to “Rental” equipment if the drones are leased out for specific mapping contracts. Regardless of the internal coding, the objective remains the same: accurately reflecting the loss in value of high-tech sensors and airframes over time.

Section 179 and Bonus Depreciation in the Drone Industry

Technological innovation is often incentivized through aggressive depreciation schedules. In many jurisdictions, “Section 179” allows a business to deduct the full purchase price of a remote sensing drone in the year it was purchased, rather than spreading it out over five years. While this is fantastic for immediate cash flow, it means that in subsequent years, the “prior year depreciation” for that specific asset will equal its total cost, leaving no further deductions. For mapping companies scaling their operations with AI-driven autonomous fleets, choosing between standard MACRS and Section 179 is a strategic decision that impacts the company’s ability to innovate in the future.

Navigating Technical Specs: Why Prior Year Records Matter for Fleet Upgrades

When a mapping company decides to upgrade from a standard photogrammetry setup to a sophisticated LiDAR (Light Detection and Ranging) system, the financial history of the existing fleet dictates the feasibility of the transition. The prior year depreciation records provide the baseline for calculating the “gain” or “loss” upon the sale or trade-in of old equipment.

Integrating AI and Autonomous Systems

Modern remote sensing drones are increasingly defined by their software and AI capabilities rather than just their rotors and frames. Autonomous flight modes, real-time data processing, and AI-driven feature extraction are now standard in high-end tech. From an accounting perspective, the challenge arises in whether to bundle the software costs with the hardware depreciation.

If the software is “embedded” (i.e., the drone cannot function without it), it is typically depreciated alongside the hardware on Line 17. However, if the software is a standalone AI platform for remote sensing analysis, it may be treated differently. Keeping these lines clear is vital for tech firms that rely on high-frequency hardware turnover to stay at the forefront of the industry.

The Impact of Remote Sensing Precision on Asset Value

The “R” in your equipment list—whether it stands for Remote Sensing, RTK, or a specific Robotic platform—carries a high value because of its precision. A drone with centimeter-level accuracy maintains its value longer than a consumer-grade unit. Consequently, the depreciation schedule should be reviewed annually to ensure it reflects the actual utility of the device. If a sensor suffers from “burn-in” or a gimbal system becomes less reliable, the business might even look into accelerated impairment, though this is less common than standard depreciation.

Optimizing Your Tech Investment: From Remote Sensing to ROI

Ultimately, the goal of tracking depreciation on professional drone equipment is to maximize the Return on Investment (ROI) while staying at the cutting edge of innovation. The “Tech & Innovation” sector moves too fast for stagnant hardware. By understanding exactly where prior year depreciation sits on your financial statements, you can better plan for the “sunset” of older technology and the “sunrise” of new autonomous systems.

Future-Proofing with Intelligent Asset Management

As we move toward a future dominated by Beyond Visual Line of Sight (BVLOS) operations and fully autonomous remote sensing swarms, the complexity of asset management will only increase. Future drones may involve modular components where the “brain” (AI module) and the “eyes” (sensors) are upgraded at different intervals. This will require even more granular tracking of depreciation lines.

For now, the standard remains clear:

- Identify the asset class: Most mapping and remote sensing drones fall under a 5-year recovery period.

- Locate the line: Use Line 17 on Form 4562 to account for the depreciation taken in prior years for your existing fleet.

- Analyze the tech cycle: Compare the remaining book value of your drones against the performance of the latest models available in the market.

Closing the Innovation Loop

The intersection of finance and flight technology is where successful drone businesses are built. Whether you are mapping a construction site, performing a volumetric analysis of a mine, or conducting environmental remote sensing, your hardware is a tool that loses financial value as it gains operational data. By mastering the nuances of prior year depreciation, you ensure that your business remains financially healthy enough to adopt the next wave of innovation, whether that be AI-integrated flight systems or the next generation of high-resolution remote sensors.

In the world of professional UAVs, staying informed about the “what line” questions is just as important as knowing the “what altitude” questions. Both are essential for a smooth, sustainable flight toward technological leadership.