Understanding the Core Concept for Tech Investments

The Weighted Average Cost of Capital (WACC) stands as a pivotal financial metric for any enterprise, especially those deeply embedded in the rapidly evolving landscape of technology and innovation, such as drone development and application. It quantifies the average rate a company expects to pay to finance its assets, representing the blended cost of all capital sources, including common stock, preferred stock, bonds, and other forms of debt. For companies pioneering in autonomous flight, advanced sensor integration, or sophisticated aerial mapping solutions, understanding their WACC is not merely an accounting exercise; it’s a strategic imperative that dictates investment decisions, project viability, and ultimately, sustainable growth.

Imagine a startup developing next-generation AI-powered drone navigation systems or an established firm investing heavily in a fleet of remote sensing UAVs for agricultural analytics. Both require significant capital. This capital isn’t free; it comes with a cost. Equity investors expect a return on their shares, and debt holders demand interest payments. WACC aggregates these individual costs into a single, comprehensive percentage, providing a crucial hurdle rate for new projects. If a proposed drone-based mapping project or the development of a new micro-drone for urban delivery is expected to generate returns below the company’s WACC, it implies that the project will destroy value for shareholders, making it an economically unviable endeavor. Conversely, projects with anticipated returns above the WACC are generally considered value-creating and therefore worth pursuing.

Components of the WACC Formula

The WACC formula is expressed as:

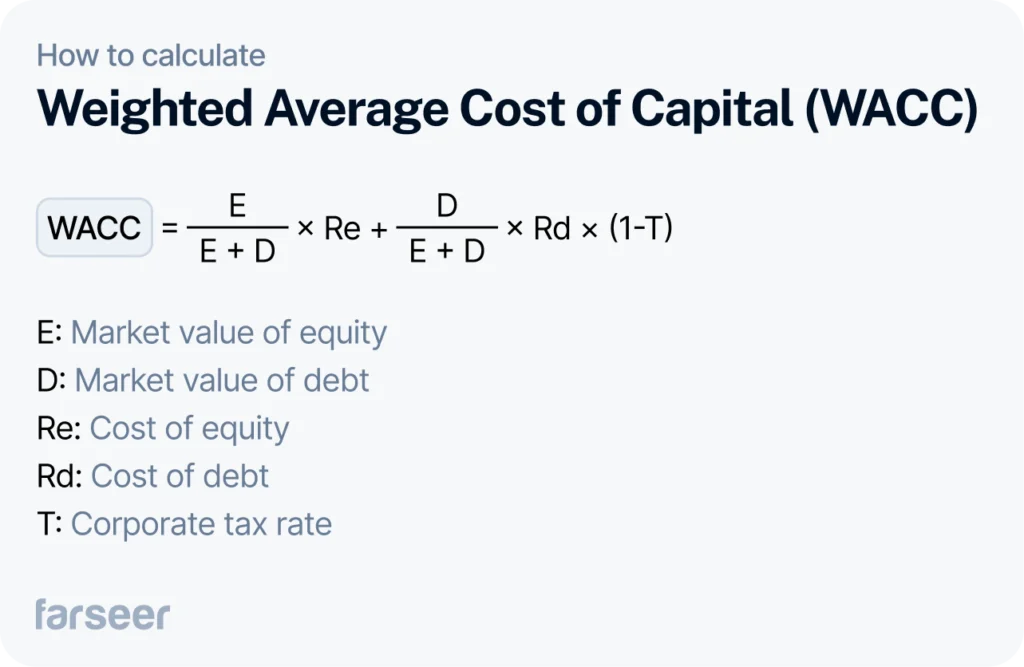

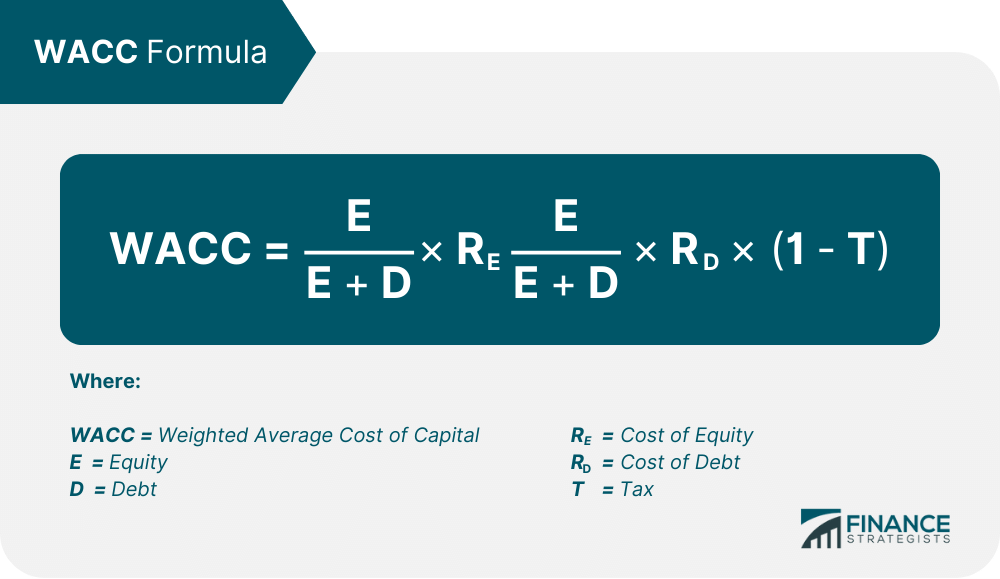

WACC = (E/V) * Re + (D/V) * Rd * (1 – Tc)

Let’s break down each component, contextualizing it within the drone technology sector:

-

Re (Cost of Equity): This is the return required by equity investors (shareholders) for their investment in a drone company. For a startup focused on FPV racing drone innovation, this could be exceptionally high due to the inherent risks and speculative nature of new tech markets. For a mature firm manufacturing enterprise-grade UAVs, it might be lower. It’s often calculated using the Capital Asset Pricing Model (CAPM): Re = Rf + β * (Rm – Rf), where Rf is the risk-free rate (e.g., government bond yield), β (Beta) measures the drone company’s stock volatility relative to the market, and (Rm – Rf) is the market risk premium. High-beta drone tech stocks, often associated with rapid innovation and competitive disruption, will inherently have a higher Re.

-

Rd (Cost of Debt): This represents the effective interest rate a drone manufacturer or service provider pays on its debt, such as bank loans taken out to fund a new drone production facility, or bonds issued to finance R&D into advanced obstacle avoidance systems. This is typically the yield to maturity on the company’s outstanding debt.

-

E (Market Value of Equity): This is the total market value of a drone company’s outstanding common stock. For a publicly traded drone software firm, it’s simply the current share price multiplied by the number of shares outstanding. For private drone ventures, valuation methods become more complex, often involving discounted cash flow (DCF) models applied to projected revenue from drone services or hardware sales.

-

D (Market Value of Debt): This is the total market value of a drone company’s debt. For a firm like one specializing in long-endurance surveillance drones, this would include the market value of its bonds and other interest-bearing liabilities.

-

V (Total Market Value of Capital): This is the sum of the market value of equity and the market value of debt (V = E + D). It represents the total capitalization of the drone technology enterprise.

-

Tc (Corporate Tax Rate): Interest payments on debt are typically tax-deductible. The (1 – Tc) component accounts for this tax shield, effectively reducing the true cost of debt for the company. For a drone logistics company, this tax benefit makes debt a cheaper source of capital than equity, given identical risk profiles.

Applying WACC in Drone Technology Ventures

The practical application of WACC extends far beyond theoretical calculations in the drone technology sector. It is an indispensable tool for strategic decision-making, particularly in a domain characterized by rapid technological advancement and significant capital expenditure.

Capital Budgeting for Drone Fleets

Consider a precision agriculture company planning to invest in a fleet of advanced sensor-equipped drones for crop health monitoring and yield prediction. This capital investment decision is a classic application for WACC. The company must estimate the future cash flows generated by this drone fleet (e.g., revenue from subscription services, cost savings from optimized pesticide application). These cash flows are then discounted back to their present value using the company’s WACC as the discount rate. If the Net Present Value (NPV) of the project is positive, it indicates that the project is expected to generate returns greater than the cost of the capital used to fund it, making it a viable investment. This ensures that the investment in high-end UAVs and their accompanying data analytics platforms is economically sound.

Similarly, a firm specializing in urban air mobility (UAM) concepts, developing eVTOL (electric Vertical Take-Off and Landing) aircraft, would use WACC to evaluate the colossal investment required for R&D, prototyping, certification, and eventual manufacturing. Each stage of development represents a project that must clear the WACC hurdle to justify its allocation of scarce capital.

Evaluating Innovation Projects: AI, Autonomous Systems, and Sensor Development

Innovation is the lifeblood of the drone industry. Companies are constantly pouring resources into developing smarter AI for autonomous drone operation, more sophisticated sensors for environmental monitoring, or advanced battery technologies for extended flight times. These R&D projects often have uncertain outcomes and long gestation periods. WACC helps in providing a quantitative framework for evaluating these initiatives.

When a drone manufacturer considers a multi-million dollar investment into an R&D project to develop a fully autonomous, BVLOS (Beyond Visual Line of Sight) drone for package delivery, they need to project the potential future cash flows from this innovation. These might include future licensing revenues, increased market share, or cost reductions. By discounting these projected cash flows using the WACC, the company can determine if the expected returns from groundbreaking innovations outweigh the capital cost and associated risks. This systematic approach prevents emotional or purely technological enthusiasm from overriding sound financial judgment, ensuring that even the most ambitious tech advancements are economically justifiable.

The Significance of Cost of Capital in Drone Ecosystem Growth

The prudent application of WACC is not just an internal financial exercise; it profoundly impacts a drone company’s external perception, its ability to attract investment, and its long-term strategic positioning within the global drone ecosystem.

Investor Confidence and Strategic Planning

A clear understanding and transparent calculation of WACC signal financial acumen to potential investors, whether venture capitalists eyeing a promising drone startup or institutional investors assessing a publicly traded UAV giant. Investors use WACC as a benchmark to gauge management’s efficiency in deploying capital. Companies that consistently undertake projects generating returns above their WACC are seen as value creators, commanding higher valuations and attracting more capital, which is crucial for scaling drone operations or funding extensive R&D.

For strategic planning, WACC helps companies define their acceptable risk-return profile. A drone company with a high WACC, perhaps due to a volatile market or significant debt, will need to pursue projects with higher expected returns. This might steer them towards niche, high-margin drone applications (e.g., specialized industrial inspection) rather than broader, lower-margin markets. Conversely, a company with a lower WACC has more flexibility to invest in a wider range of projects, including those with slightly lower but stable returns, such as expanding a drone-as-a-service (DaaS) offering.

Risk Assessment and Project Viability in Emerging Drone Markets

The drone industry is dynamic, with emerging markets in areas like urban air mobility, drone delivery, and comprehensive remote sensing. These markets often carry higher intrinsic risks – regulatory uncertainties, nascent technologies, and unpredictable competitive landscapes. The WACC formula inherently incorporates some of these risks through the cost of equity (Re) and cost of debt (Rd) components.

For instance, a lender providing debt to a company developing cutting-edge drone surveillance technology for a sensitive security application might demand a higher interest rate (higher Rd) due to perceived regulatory or market adoption risks. Similarly, equity investors in a company attempting to disrupt air cargo with heavy-lift drones might demand a higher return (higher Re) to compensate for the significant technological and market penetration risks. By using a WACC that reflects these specific risks, drone companies can make more realistic assessments of project viability. If the expected returns from a revolutionary drone concept cannot exceed a WACC that accurately prices in its unique risks, the project may need re-evaluation or even abandonment, preventing misallocation of precious capital in an industry where innovation is both costly and crucial.

Calculating WACC for a Drone Tech Company Example

Let’s consider a hypothetical drone manufacturing and software integration company, “AeroView Solutions Inc.,” specializing in mapping and inspection drones for the energy sector. AeroView needs to raise capital for a new initiative: developing an AI-powered autonomous inspection system for wind turbines, reducing human risk and increasing efficiency.

Assume the following financial data for AeroView Solutions Inc.:

- Market Value of Equity (E): AeroView has 50 million shares outstanding, currently trading at $20 per share. So, E = 50,000,000 * $20 = $1,000,000,000.

- Market Value of Debt (D): The company has outstanding bonds with a total market value of $400,000,000.

- Total Market Value of Capital (V): V = E + D = $1,000,000,000 + $400,000,000 = $1,400,000,000.

- Cost of Equity (Re): Using CAPM, assume the risk-free rate is 3%, AeroView’s Beta is 1.5 (reflecting its position in a growth industry), and the market risk premium is 6%.

Re = 3% + 1.5 * 6% = 3% + 9% = 12%. - Cost of Debt (Rd): The company’s average yield to maturity on its debt is 5%.

- Corporate Tax Rate (Tc): AeroView’s effective corporate tax rate is 25%.

Now, let’s plug these values into the WACC formula:

WACC = (E/V) * Re + (D/V) * Rd * (1 – Tc)

-

Calculate the weight of equity (E/V):

E/V = $1,000,000,000 / $1,400,000,000 ≈ 0.7143 -

Calculate the weight of debt (D/V):

D/V = $400,000,000 / $1,400,000,000 ≈ 0.2857 -

Calculate the after-tax cost of debt:

Rd * (1 – Tc) = 5% * (1 – 0.25) = 5% * 0.75 = 3.75% -

Combine the components:

WACC = (0.7143 * 12%) + (0.2857 * 3.75%)

WACC = 0.085716 + 0.01071375

WACC ≈ 0.09642975

Therefore, AeroView Solutions Inc.’s WACC is approximately 9.64%.

This 9.64% represents the minimum rate of return AeroView’s new AI-powered wind turbine inspection system project must generate to satisfy its investors (both equity and debt holders). If the project’s expected internal rate of return (IRR) is higher than 9.64%, it’s considered a value-adding investment. If it’s lower, the company would be destroying shareholder value by pursuing it, suggesting a re-evaluation of the project’s scope, technology, or funding structure. This systematic evaluation empowers drone companies to make financially sound decisions amidst the dynamic technological advancements of the industry.