Ratio analysis is a powerful quantitative technique used to evaluate the performance, financial health, and operational efficiency of a business. By comparing different financial statement line items, it provides a standardized way to assess a company’s strengths and weaknesses, allowing for meaningful comparisons with past performance, industry benchmarks, and competitor data. This analytical approach is indispensable for investors, creditors, management, and even regulators seeking to gain a deeper understanding of a company’s underlying value and its ability to meet its obligations and generate profits.

At its core, ratio analysis involves calculating and interpreting various ratios derived from a company’s balance sheet, income statement, and cash flow statement. These ratios act as diagnostic tools, highlighting trends, identifying potential problems, and offering insights into areas that might require further investigation. The true value of ratio analysis lies not just in the calculation of these numbers, but in their subsequent interpretation within a relevant context. Without this understanding, the ratios themselves are merely abstract figures.

Understanding the Building Blocks: Financial Statements

Before delving into the intricacies of ratio calculation and interpretation, it’s crucial to have a firm grasp of the financial statements from which these ratios are derived. These documents are the bedrock of any financial analysis, providing the raw data that ratio analysis transforms into actionable insights.

The Balance Sheet: A Snapshot in Time

The balance sheet, also known as the statement of financial position, presents a company’s assets, liabilities, and equity at a specific point in time, typically at the end of a fiscal quarter or year. It adheres to the fundamental accounting equation: Assets = Liabilities + Equity.

- Assets: These are resources owned or controlled by the company with the expectation of providing future economic benefits. Assets are typically categorized as current (expected to be converted to cash or used within one year) or non-current (long-term assets). Examples include cash, accounts receivable, inventory, property, plant, and equipment, and intangible assets.

- Liabilities: These represent obligations of the company to external parties, representing amounts owed. Like assets, liabilities are categorized as current (due within one year) or non-current (due beyond one year). Examples include accounts payable, salaries payable, short-term loans, and long-term debt.

- Equity: This represents the owners’ stake in the company. It’s the residual interest in the assets of the entity after deducting all its liabilities. Equity includes common stock, preferred stock, and retained earnings.

The balance sheet provides a static view, showing what a company owns and owes at a particular moment. Ratios derived from the balance sheet often focus on liquidity, solvency, and capital structure.

The Income Statement: Performance Over a Period

The income statement, also known as the profit and loss (P&L) statement, reports a company’s financial performance over a specific period, such as a quarter or a year. It details the revenues earned and expenses incurred to arrive at the net income or loss. The basic structure is: Revenue – Expenses = Net Income (or Loss).

- Revenue (or Sales): This is the total income generated from the company’s primary business activities, such as selling goods or services.

- Cost of Goods Sold (COGS): The direct costs attributable to the production or purchase of the goods sold by a company.

- Gross Profit: Revenue minus COGS. This indicates the profitability of a company’s core operations before considering operating expenses.

- Operating Expenses: Costs incurred in the normal course of business, excluding COGS. This includes selling, general, and administrative (SG&A) expenses, research and development (R&D), and marketing costs.

- Operating Income (or EBIT – Earnings Before Interest and Taxes): Gross profit minus operating expenses. This shows the profit generated from the company’s core business operations.

- Interest Expense: The cost of borrowing money.

- Taxes: Income taxes paid to the government.

- Net Income (or Net Profit): The “bottom line,” representing the profit remaining after all expenses, interest, and taxes have been deducted.

The income statement provides a dynamic view of a company’s profitability and operational efficiency over time. Ratios derived from the income statement often focus on profitability and operational performance.

The Cash Flow Statement: Tracking Cash Movements

The cash flow statement tracks the movement of cash and cash equivalents into and out of a company over a specific period. It’s crucial because profit, as reported on the income statement, doesn’t always equate to readily available cash. The statement categorizes cash flows into three primary activities:

- Cash Flow from Operating Activities (CFO): Cash generated from the company’s normal business operations. This is often considered the most important section, as it indicates the company’s ability to generate cash from its core activities.

- Cash Flow from Investing Activities (CFI): Cash used or generated from the purchase or sale of long-term assets, such as property, plant, and equipment, or investments in other companies.

- Cash Flow from Financing Activities (CFF): Cash generated or used in transactions related to debt, equity, and dividends. This includes issuing or repurchasing stock, taking out or repaying loans, and paying dividends.

The cash flow statement provides insights into a company’s liquidity and its ability to fund its operations, invest in growth, and repay its debts. Ratios derived from the cash flow statement can offer a more accurate picture of a company’s true cash-generating ability.

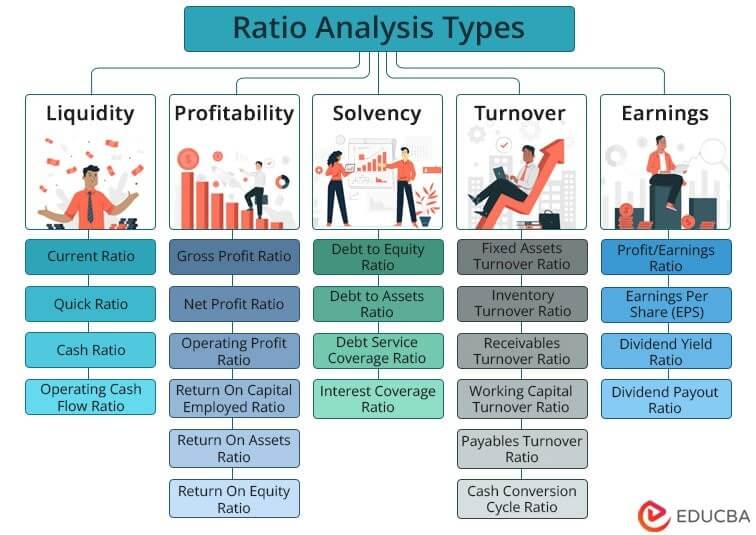

The Power of Comparison: Categories of Financial Ratios

Ratio analysis categorizes ratios into several key groups, each designed to illuminate a specific aspect of a company’s financial health and performance. By examining ratios across these categories, analysts can build a comprehensive picture of a company’s operational effectiveness and financial stability.

Liquidity Ratios: Measuring Short-Term Solvency

Liquidity ratios assess a company’s ability to meet its short-term obligations (those due within one year) using its most liquid assets. A company with strong liquidity can comfortably pay its bills as they come due, indicating financial stability in the short term.

- Current Ratio: This is one of the most fundamental liquidity ratios. It compares a company’s current assets to its current liabilities.

- Formula: Current Ratio = Current Assets / Current Liabilities

- Interpretation: A current ratio of 2:1 (or higher) is generally considered healthy, meaning the company has $2 of current assets for every $1 of current liabilities. A ratio below 1:1 suggests potential difficulty in meeting short-term obligations. However, an excessively high ratio might indicate inefficient use of assets.

- Quick Ratio (Acid-Test Ratio): This ratio is a more stringent measure of liquidity than the current ratio because it excludes inventory from current assets. Inventory is often the least liquid current asset and can be difficult to convert to cash quickly without a significant price reduction.

- Formula: Quick Ratio = (Current Assets – Inventory) / Current Liabilities

- Interpretation: A quick ratio of 1:1 (or higher) is generally considered good, indicating the company can meet its short-term obligations without relying on selling inventory.

- Cash Ratio: This is the most conservative liquidity ratio, measuring a company’s ability to pay off its current liabilities using only its cash and cash equivalents.

- Formula: Cash Ratio = (Cash + Cash Equivalents) / Current Liabilities

- Interpretation: A higher cash ratio indicates a stronger ability to cover immediate obligations. This ratio is particularly useful for businesses with volatile cash flows or those in industries with long production cycles.

Profitability Ratios: Gauging Earning Power

Profitability ratios measure a company’s ability to generate earnings from its sales, assets, and equity. These ratios are crucial for investors and management to assess the company’s performance and its potential for growth.

- Gross Profit Margin: This ratio reveals how much profit a company makes after deducting the cost of goods sold from its revenue.

- Formula: Gross Profit Margin = (Gross Profit / Revenue) * 100%

- Interpretation: A higher gross profit margin indicates that the company is efficiently managing its production costs and has pricing power. It shows how effectively the company turns raw materials into products or services.

- Operating Profit Margin (EBIT Margin): This ratio measures a company’s profitability from its core operations before considering interest and taxes.

- Formula: Operating Profit Margin = (Operating Income / Revenue) * 100%

- Interpretation: A higher operating profit margin suggests efficient management of operating expenses and strong operational control. It provides a clearer picture of the company’s ability to generate profits from its business activities.

- Net Profit Margin: This is the “bottom line” profitability ratio, indicating how much net income is generated per dollar of sales.

- Formula: Net Profit Margin = (Net Income / Revenue) * 100%

- Interpretation: A higher net profit margin indicates greater overall profitability after all expenses, interest, and taxes have been accounted for. It reflects the company’s ability to control all costs and maximize shareholder returns.

- Return on Assets (ROA): This ratio measures how efficiently a company uses its assets to generate profits.

- Formula: ROA = Net Income / Total Assets

- Interpretation: A higher ROA signifies that the company is effectively utilizing its assets to produce earnings. It’s a key indicator of asset management efficiency.

- Return on Equity (ROE): This vital ratio measures the profitability of a company in relation to its shareholders’ equity. It shows how effectively the company is using its shareholders’ investments to generate profits.

- Formula: ROE = Net Income / Shareholder’s Equity

- Interpretation: A higher ROE indicates that the company is generating strong returns for its shareholders. However, it’s important to consider the company’s debt levels, as high leverage can artificially inflate ROE.

Efficiency Ratios (Activity Ratios): Assessing Operational Performance

Efficiency ratios, also known as activity ratios or turnover ratios, measure how effectively a company is using its assets to generate sales and manage its operations. These ratios provide insights into the speed at which a company converts its assets into revenue.

- Inventory Turnover Ratio: This ratio indicates how many times a company has sold and replaced its inventory during a given period.

- Formula: Inventory Turnover Ratio = Cost of Goods Sold / Average Inventory

- Interpretation: A higher inventory turnover ratio generally suggests that inventory is being sold quickly and efficiently, minimizing holding costs and obsolescence. A low turnover might indicate slow-moving inventory or overstocking.

- Accounts Receivable Turnover Ratio: This ratio measures how efficiently a company collects its outstanding credit sales.

- Formula: Accounts Receivable Turnover Ratio = Net Credit Sales / Average Accounts Receivable

- Interpretation: A higher turnover indicates that the company is collecting its receivables quickly, reducing the risk of bad debts and improving cash flow. A low turnover might signal problems with credit policies or collection efforts.

- Accounts Payable Turnover Ratio: This ratio measures how quickly a company pays its suppliers.

- Formula: Accounts Payable Turnover Ratio = Cost of Goods Sold / Average Accounts Payable

- Interpretation: A higher turnover suggests the company is paying its suppliers promptly, which can be beneficial for maintaining good supplier relationships. However, a very high turnover might indicate that the company isn’t taking full advantage of available credit terms.

- Asset Turnover Ratio: This broad efficiency ratio measures how efficiently a company uses all of its assets to generate sales.

- Formula: Asset Turnover Ratio = Revenue / Average Total Assets

- Interpretation: A higher asset turnover ratio implies that the company is generating more sales for each dollar of assets it owns, indicating efficient asset utilization.

Solvency Ratios (Leverage Ratios): Evaluating Long-Term Financial Stability

Solvency ratios, also known as leverage ratios, measure a company’s ability to meet its long-term debt obligations. They provide insight into the company’s financial risk and its reliance on borrowed funds.

- Debt-to-Equity Ratio: This is a key leverage ratio that compares a company’s total debt to its shareholder equity.

- Formula: Debt-to-Equity Ratio = Total Debt / Shareholder’s Equity

- Interpretation: A higher debt-to-equity ratio indicates that the company is using more debt financing relative to equity financing, which can increase financial risk. A lower ratio suggests a more conservative financial structure.

- Debt-to-Assets Ratio: This ratio measures the proportion of a company’s assets that are financed by debt.

- Formula: Debt-to-Assets Ratio = Total Debt / Total Assets

- Interpretation: A higher ratio indicates a greater reliance on debt, which can make the company more vulnerable to economic downturns.

- Interest Coverage Ratio (Times Interest Earned): This ratio measures a company’s ability to cover its interest expenses with its operating income.

- Formula: Interest Coverage Ratio = Earnings Before Interest and Taxes (EBIT) / Interest Expense

- Interpretation: A higher interest coverage ratio indicates that the company has a greater capacity to meet its interest payments, suggesting lower financial risk. A ratio below 1.5:1 might be a cause for concern.

The Art of Interpretation: Beyond the Numbers

Calculating financial ratios is only the first step in the process. The true value of ratio analysis emerges from the careful and insightful interpretation of these figures. Without proper context, the numbers themselves are meaningless.

Benchmarking and Trend Analysis

To make ratios truly useful, they must be compared against relevant benchmarks.

- Historical Analysis (Trend Analysis): Examining a company’s ratios over multiple periods (quarters or years) reveals trends in its performance. Is profitability improving or declining? Is liquidity strengthening or weakening? This analysis helps identify patterns and predict future performance. For example, a declining net profit margin over several years, even if still positive, warrants investigation into the underlying causes.

- Industry Analysis (Cross-Sectional Analysis): Comparing a company’s ratios to those of its peers in the same industry provides crucial context. What is considered a “good” ratio can vary significantly by industry. A high inventory turnover might be excellent in a fast-fashion retail industry but poor in a heavy manufacturing sector. This comparison highlights competitive strengths and weaknesses.

- Competitor Analysis: Specifically comparing a company’s ratios to its closest competitors can offer even more granular insights into its market position and operational efficiency relative to its direct rivals.

Limitations of Ratio Analysis

Despite its power, ratio analysis is not without its limitations. It’s essential to be aware of these to avoid drawing inaccurate conclusions.

- Historical Data Dependence: Ratios are based on historical financial statements. They reflect past performance and may not accurately predict future outcomes, especially in rapidly changing economic environments.

- Accounting Method Differences: Different accounting methods (e.g., inventory valuation methods like FIFO vs. LIFO, depreciation methods) can distort comparisons between companies, even within the same industry.

- Inflation Effects: Inflation can distort historical figures, making comparisons over long periods challenging without adjustments.

- Qualitative Factors Ignored: Ratio analysis is purely quantitative. It doesn’t account for qualitative factors such as management quality, brand reputation, employee morale, regulatory changes, or technological disruptions, all of which can significantly impact a company’s performance.

- Manipulation Potential: Companies may engage in accounting practices that can manipulate financial ratios to present a more favorable picture.

- One-Time Events: Unusual or one-time events (e.g., a large asset sale, a major lawsuit settlement) can distort ratios for a specific period and require careful consideration.

Conclusion: A Vital Tool for Informed Decision-Making

Ratio analysis is an indispensable tool for anyone seeking to understand the financial health and operational performance of a business. By systematically analyzing key financial metrics derived from a company’s financial statements, investors, creditors, and management can gain invaluable insights. Whether assessing short-term liquidity, long-term solvency, profitability, or operational efficiency, ratios provide a standardized and comparable framework.

However, the true power of ratio analysis lies not solely in the calculation of numbers but in their thoughtful interpretation. Benchmarking against historical trends, industry averages, and competitors, while acknowledging the inherent limitations of the technique, allows for a comprehensive and nuanced understanding. When used judiciously and in conjunction with qualitative analysis, ratio analysis serves as a cornerstone of sound financial decision-making, empowering stakeholders to make informed judgments about investment, lending, and strategic management.