Accounting is often described as the language of business, providing a structured framework for recording, classifying, summarizing, and interpreting financial transactions. Understanding its core principles is fundamental for any individual or organization seeking to grasp financial health, make informed decisions, and ensure transparency and accountability. These principles, also known as Generally Accepted Accounting Principles (GAAP) in the United States and International Financial Reporting Standards (IFRS) globally, are the bedrock upon which financial statements are built. They ensure consistency, comparability, and reliability of financial information across different entities and over time.

The Foundational Concepts of Accounting

At its heart, accounting operates on a set of foundational concepts that guide its application. These are not rigid rules but rather guiding philosophies that ensure the information presented is relevant, reliable, and understandable.

The Accounting Equation: The Core of Financial Health

The most fundamental principle in accounting is the accounting equation: Assets = Liabilities + Equity. This equation forms the basis for the double-entry bookkeeping system, ensuring that every financial transaction has an equal and opposite effect on at least two accounts.

- Assets: These are resources owned by a company that have economic value and are expected to provide future benefits. Examples include cash, accounts receivable (money owed to the company), inventory, property, plant, and equipment.

- Liabilities: These represent obligations of the company to external parties. They are what the company owes to others. Examples include accounts payable (money owed by the company to suppliers), salaries payable, and loans.

- Equity: This represents the owners’ stake in the company. It is the residual interest in the assets of the entity after deducting all its liabilities. For a sole proprietorship, it’s owner’s equity; for a corporation, it’s shareholders’ equity.

This equation is continuously balanced. If a company acquires a new asset, either a liability must increase (e.g., by taking out a loan) or equity must increase (e.g., through owner investment or retained earnings).

The Double-Entry System

The double-entry system is the mechanism that upholds the accounting equation. For every financial transaction, there are at least two entries made in the accounting records: one debit and one credit.

- Debits: Generally, debits increase asset and expense accounts, while decreasing liability, equity, and revenue accounts.

- Credits: Generally, credits increase liability, equity, and revenue accounts, while decreasing asset and expense accounts.

The sum of all debits must always equal the sum of all credits. This system provides a built-in error-checking mechanism, as any imbalance signals an error in recording.

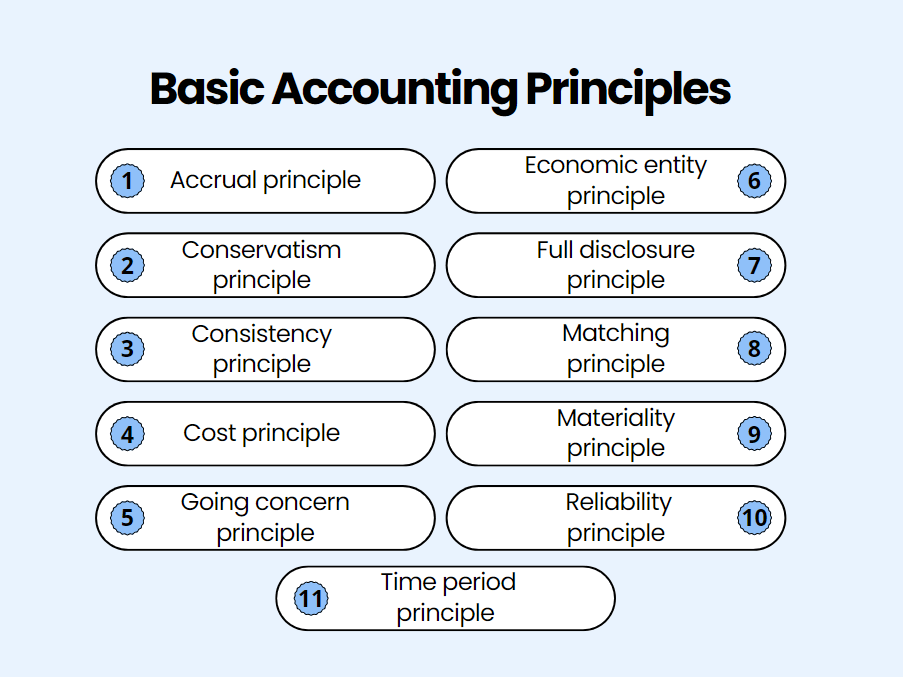

Accrual Basis vs. Cash Basis Accounting

A critical distinction in accounting lies in the method used to recognize revenue and expenses.

- Accrual Basis Accounting: This method recognizes revenue when it is earned (regardless of when cash is received) and expenses when they are incurred (regardless of when cash is paid). This provides a more accurate picture of a company’s financial performance over a period, aligning revenues with the expenses incurred to generate them. For example, if a company provides a service in December but doesn’t receive payment until January, under accrual accounting, the revenue is recognized in December.

- Cash Basis Accounting: This method recognizes revenue only when cash is received and expenses only when cash is paid. While simpler, it can distort the true financial performance of a business, especially if there are significant delays between earning revenue and receiving payment, or incurring expenses and paying them.

GAAP and IFRS predominantly mandate the accrual basis for most entities due to its superior ability to reflect true economic performance.

Core Accounting Principles and Assumptions

Beyond the fundamental equation and system, several core principles and assumptions guide the practice of accounting, ensuring that financial information is presented in a consistent and meaningful way.

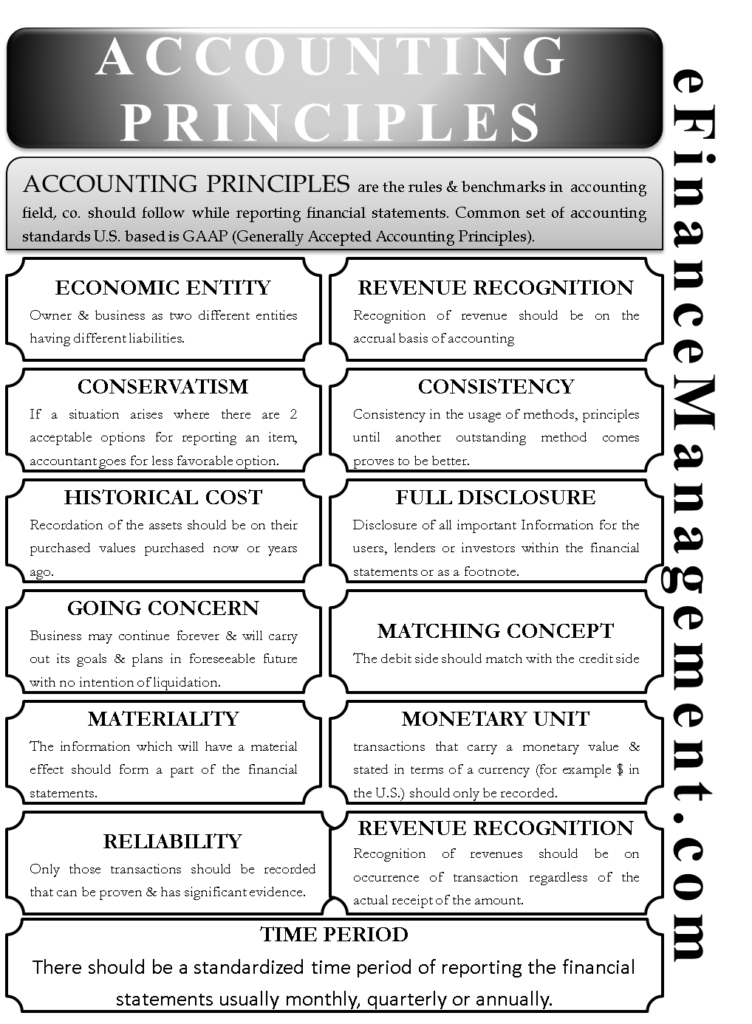

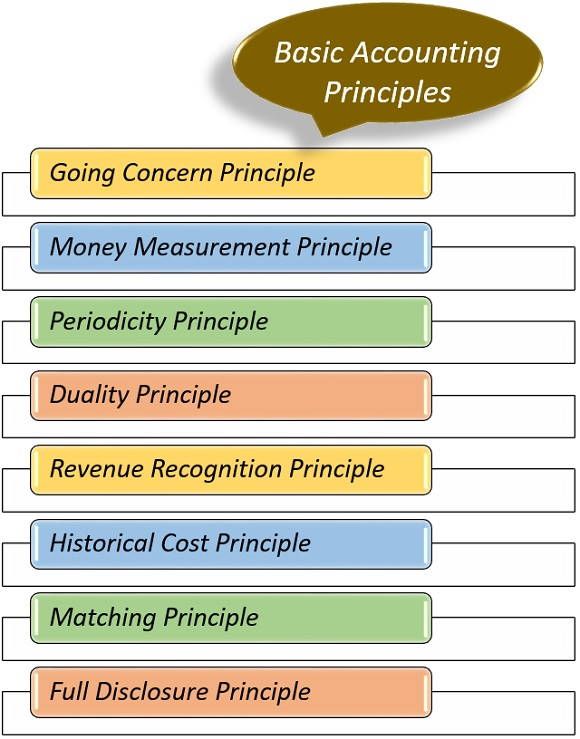

The Going Concern Assumption

This assumption posits that a business will continue to operate for the foreseeable future, without the intention or necessity of liquidation or significant curtailment of operations. This assumption is crucial because it justifies methods like depreciation, where the cost of an asset is spread over its useful life. If a company were not expected to continue, its assets would be valued at their liquidation value, not their historical cost less accumulated depreciation.

The Cost Principle (Historical Cost)

Assets are generally recorded at their original cost at the time of acquisition. This principle provides an objective and verifiable basis for asset valuation. While market values can fluctuate, historical cost remains a stable benchmark. However, there are exceptions, particularly for certain investments or when assets are impaired below their carrying value.

The Revenue Recognition Principle

Revenue should be recognized when it is earned and realized or realizable. “Earned” means the company has substantially completed its earning process. “Realized” means the asset has been converted into cash. “Realizable” means the asset is readily convertible into a known amount of cash. This principle prevents companies from artificially inflating their revenues.

The Matching Principle (Expense Recognition)

Expenses should be recognized in the same period as the revenues they helped to generate. This principle, closely linked to the accrual basis, ensures that a company’s profitability for a given period is accurately reflected by matching the costs of producing goods or services with the revenue generated from them. For example, the cost of goods sold is matched against the sales revenue in the same accounting period.

The Full Disclosure Principle

This principle dictates that all information that could significantly affect the decisions of financial statement users should be disclosed. This includes providing detailed footnotes to financial statements that explain accounting policies, contingencies, and other relevant information. Transparency is key to ensuring users have a complete understanding of the company’s financial position and performance.

The Objectivity Principle

Financial information should be based on objective evidence rather than subjective opinions or estimations. While some estimations are unavoidable (e.g., in calculating bad debt expense), they should be based on reasonable and verifiable data. This principle enhances the reliability and trustworthiness of financial statements.

The Materiality Principle

This principle states that an accounting principle or practice need not be followed if the effect is insignificant enough that it would not influence the judgment of a reasonable person relying on the financial statements. In essence, trivial matters can be treated in the most expedient manner, allowing focus on items that truly impact financial decisions. Determining materiality is often a matter of professional judgment.

The Conservatism Principle

When faced with uncertainty or a choice between two acceptable accounting methods, the method that results in the lower net income or asset value should be preferred. This principle aims to ensure that financial statements do not overstate a company’s financial position or performance. It provides a margin of safety for users of financial information. For example, potential losses are recognized immediately, while potential gains are recognized only when they are realized.

The Role of Accounting Standards

The principles outlined above are codified and elaborated upon by authoritative bodies to create comprehensive accounting standards.

Generally Accepted Accounting Principles (GAAP)

In the United States, the Financial Accounting Standards Board (FASB) sets the accounting standards known as GAAP. These principles are established to ensure that financial reporting is consistent, comparable, and transparent for U.S. companies.

International Financial Reporting Standards (IFRS)

Globally, the International Accounting Standards Board (IASB) issues IFRS, which are used in over 140 countries. IFRS aims to create a common global language for business affairs so that company accounts are understandable and comparable across international boundaries.

While both GAAP and IFRS are principles-based, they have differences in their specific rules and interpretations. The ultimate goal of both is to provide users of financial statements with useful information for making economic decisions.

Applications and Importance

The principles of accounting are not merely academic concepts; they have profound practical implications for a wide range of stakeholders.

For Business Owners and Management

Understanding accounting principles is crucial for internal decision-making, budgeting, performance evaluation, and strategic planning. It allows management to track profitability, manage cash flow, and assess the financial impact of various business activities.

For Investors and Creditors

These principles enable investors to assess the profitability and financial stability of a company, guiding their investment decisions. Creditors use financial statements to evaluate a company’s ability to repay loans and manage risk.

For Regulators and Government Agencies

Regulatory bodies use accounting principles to ensure compliance with tax laws, securities regulations, and other legal requirements. Accurate financial reporting is essential for the functioning of capital markets and for protecting the public interest.

For the Public

The principles of accounting contribute to overall economic transparency and accountability. They allow the public to understand the financial health of companies and the broader economic landscape.

In conclusion, the principles of accounting provide a robust and logical framework for understanding and communicating financial information. By adhering to these foundational concepts and standards, businesses can foster trust, facilitate informed decision-making, and contribute to a more transparent and efficient global economy. Mastering these principles is not just about recording numbers; it’s about understanding the financial narrative of an organization and its place within the broader economic ecosystem.