The Foundations of Economic Growth: Understanding the Loanable Funds Market

The intricate dance of modern economies relies heavily on the efficient allocation of capital. At its core, this allocation is facilitated by a crucial, yet often unseen, mechanism: the loanable funds market. This market represents the aggregate supply of and demand for loanable funds, which are essentially the financial resources available for lending and borrowing. Understanding the dynamics of this market is paramount to grasping how businesses expand, governments finance their operations, and individuals invest in their futures.

Defining Loanable Funds

Loanable funds can be conceptualized as the pool of money that is available for individuals, businesses, and governments to borrow or save. This pool isn’t a physical entity but rather a conceptual representation of the flow of savings and credit within an economy. The primary sources of loanable funds include:

- Household Savings: When individuals choose to save a portion of their income rather than consume it, these savings become available in the loanable funds market. This can take various forms, such as deposits in banks, investments in mutual funds, or direct purchases of bonds.

- Business Savings (Retained Earnings): Companies that generate profits and choose to reinvest them back into their operations, rather than distributing them as dividends, contribute to the supply of loanable funds. These retained earnings can be used for internal investment or made available through financial markets.

- Government Surpluses: When a government’s tax revenues exceed its expenditures, the resulting budget surplus adds to the supply of loanable funds. However, budget deficits, which are more common, actually increase the demand for loanable funds.

- Net Capital Inflows: In an open economy, foreign investment flowing into the country can also increase the supply of loanable funds. Conversely, domestic investors lending to foreign entities would decrease the domestic supply.

- Monetary Policy Actions by Central Banks: While not a direct source of “savings” in the traditional sense, central bank actions like open market operations (buying government securities) can inject liquidity into the banking system, effectively increasing the supply of funds available for lending.

The demand for loanable funds arises from entities seeking to acquire capital for various purposes, including:

- Business Investment: Companies borrow funds to finance capital expenditures, such as building new factories, purchasing machinery, or investing in research and development. These investments are crucial for economic expansion and productivity growth.

- Government Borrowing: Governments often issue bonds to finance budget deficits, fund infrastructure projects, or manage national debt. This borrowing directly increases the demand for loanable funds.

- Household Borrowing: Individuals borrow for major purchases like homes (mortgages), cars (auto loans), or education (student loans). While some household borrowing is for consumption, a significant portion is for investments that can enhance future earning potential.

- Net Capital Outflows: Domestic entities lending to foreign entities or investing abroad represents a demand for loanable funds from a global perspective, reducing the domestic supply.

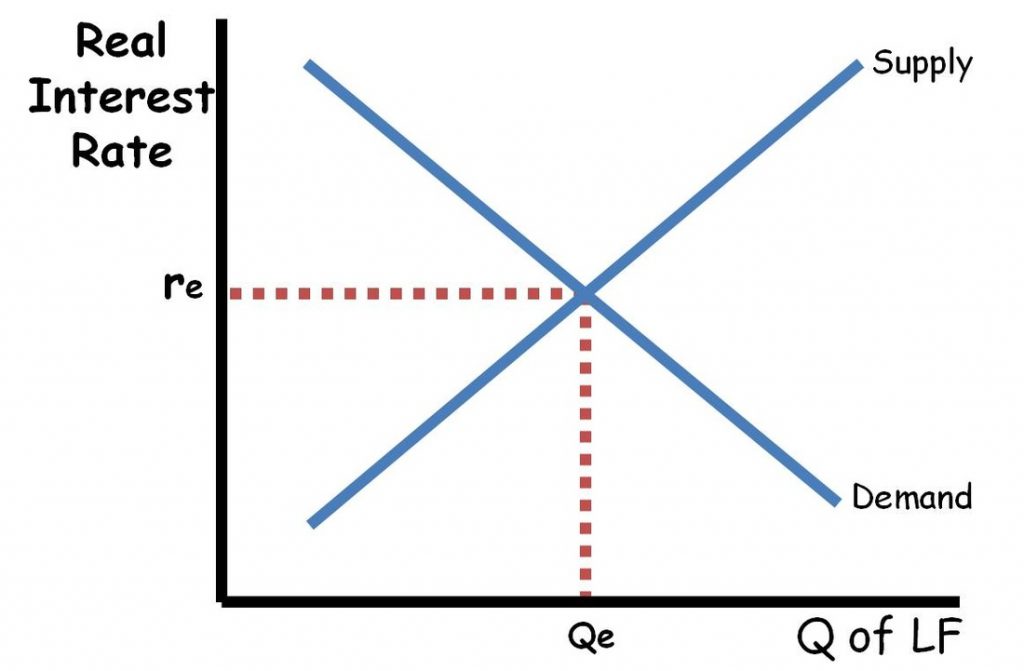

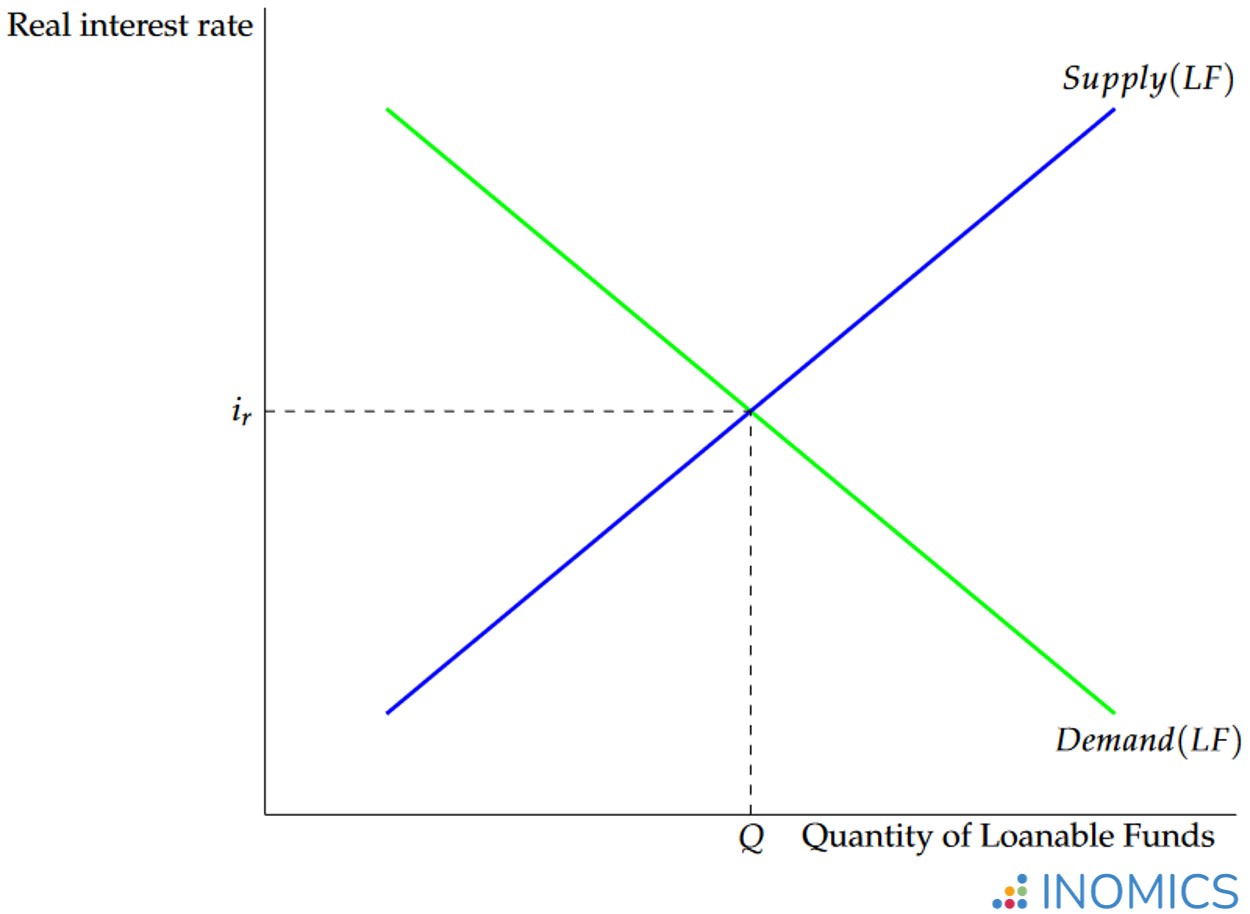

The interaction of this supply and demand determines the “price” of loanable funds, which is the real interest rate.

The Interest Rate: The Price of Loanable Funds

The real interest rate is the cornerstone of the loanable funds market. It represents the return a lender receives for parting with their funds for a period, and the cost a borrower incurs for obtaining those funds. In essence, it’s the price that equilibrates the supply and demand for loanable funds.

The nominal interest rate, which is the rate quoted by financial institutions, is comprised of the real interest rate and expected inflation. The real interest rate reflects the actual purchasing power gained or lost by the lender.

-

Factors Shifting the Supply of Loanable Funds:

- Changes in Savings Behavior: An increase in the propensity to save by households or businesses will shift the supply curve for loanable funds to the right, leading to a lower equilibrium real interest rate. Conversely, a decrease in savings will shift the supply curve to the left, raising the interest rate.

- Government Budget Surpluses: A shift from a budget deficit to a surplus (or a reduction in the deficit) reduces government borrowing, thus decreasing the demand for loanable funds. However, if the government uses a surplus to pay down debt, it effectively increases the supply of funds available to the private sector.

- Technological Advancements or Increased Confidence: These can boost business and household confidence, potentially leading to higher saving rates or a reduced demand for immediate consumption, thus increasing the supply of loanable funds.

- Monetary Policy Easing: When a central bank lowers reserve requirements or buys government bonds, it injects liquidity into the banking system, increasing the supply of loanable funds and potentially lowering interest rates.

-

Factors Shifting the Demand for Loanable Funds:

- Changes in Investment Opportunities: An increase in profitable investment opportunities for businesses will shift the demand curve for loanable funds to the right, leading to a higher equilibrium real interest rate. A decrease in such opportunities will shift the demand curve to the left, lowering the interest rate.

- Government Budget Deficits: An increase in government borrowing to finance deficits shifts the demand curve for loanable funds to the right, pushing up the real interest rate.

- Increased Household Borrowing: Higher demand for mortgages, auto loans, or other forms of credit by households will also shift the demand curve to the right.

- Economic Uncertainty or Pessimism: If businesses and households become pessimistic about the future, they may reduce investment and borrowing, shifting the demand curve for loanable funds to the left.

- Monetary Policy Tightening: When a central bank increases reserve requirements or sells government bonds, it withdraws liquidity from the banking system, decreasing the supply of loanable funds. This is often done to curb inflation, which tends to increase interest rates.

The Role of Financial Intermediaries

While the loanable funds market is a conceptual representation, its actual operation relies heavily on financial intermediaries. These institutions act as bridges between savers and borrowers, facilitating the flow of funds.

- Banks: Commercial banks are perhaps the most prominent financial intermediaries. They accept deposits from savers and use these funds to make loans to businesses and individuals. Their ability to create money through fractional reserve banking plays a significant role in the supply of loanable funds.

- Credit Unions: Similar to banks, credit unions accept deposits and provide loans, but they are typically member-owned non-profit organizations.

- Investment Banks: These institutions underwrite the issuance of new securities (stocks and bonds) by corporations and governments, thereby channeling savings from investors directly to those seeking to raise capital.

- Mutual Funds and Pension Funds: These institutions pool the savings of many individuals and invest them in a diversified portfolio of assets, including bonds and stocks, making them significant players in the demand and supply for various types of loanable funds.

- Insurance Companies: They collect premiums from policyholders and invest these funds, contributing to the supply of loanable funds.

These intermediaries play a vital role in reducing transaction costs, diversifying risk, and providing information, all of which contribute to the efficiency of the loanable funds market.

The Loanable Funds Market and Macroeconomic Policy

The loanable funds market is not only a descriptive tool but also a prescriptive one for policymakers. Understanding its mechanisms allows governments and central banks to implement policies aimed at influencing economic outcomes.

- Fiscal Policy: Government decisions on taxation and spending directly impact the demand for loanable funds. For example, tax cuts can stimulate consumption and investment, potentially increasing the demand for loanable funds. Increased government spending, especially if financed by borrowing, will directly increase this demand. Conversely, fiscal austerity and deficit reduction can decrease the demand for loanable funds, potentially leading to lower interest rates.

- Monetary Policy: Central banks, such as the Federal Reserve in the United States, exert significant influence over the supply of loanable funds. By adjusting interest rates (like the federal funds rate), conducting open market operations, and setting reserve requirements, they can either expand or contract the availability of credit. When the central bank aims to stimulate the economy, it typically lowers interest rates by increasing the supply of loanable funds. To combat inflation, it may raise interest rates by reducing the supply of loanable funds.

The effectiveness of these policies is often analyzed through the lens of the loanable funds market. For instance, a government trying to stimulate investment through tax incentives might find its efforts offset if the central bank simultaneously tightens monetary policy, leading to higher borrowing costs that discourage businesses from taking out loans.

Conclusion: The Engine of Capital Allocation

In conclusion, the loanable funds market, though a theoretical construct, represents the fundamental forces that govern the availability and cost of capital in an economy. It is where the desires of savers to earn a return on their assets meet the needs of borrowers seeking funds for investment and consumption. The real interest rate, determined by the interplay of supply and demand within this market, acts as the critical price signal that guides resource allocation, influencing everything from individual purchasing decisions to the strategic growth plans of multinational corporations. A well-functioning loanable funds market is therefore indispensable for fostering innovation, driving productivity, and ultimately achieving sustainable economic prosperity. The policies enacted by governments and central banks, whether fiscal or monetary, are designed to navigate and influence this market, aiming to steer the economy towards desired outcomes of growth, stability, and low inflation.