The Home Mortgage Disclosure Act (HMDA) is a pivotal piece of U.S. federal legislation enacted in 1975. Its primary objective is to combat discriminatory lending practices, particularly in the mortgage market. By requiring financial institutions to report data on their mortgage lending activities, HMDA provides valuable insights into the availability and accessibility of home loans across various demographic groups and geographic areas. This transparency allows regulators, policymakers, and the public to identify potential patterns of redlining, reverse redlining, and other forms of discrimination, ultimately promoting fair and equitable access to housing finance.

Understanding the Core Principles of HMDA

At its heart, HMDA is a transparency and anti-discrimination law. It aims to shed light on how mortgage lenders are making decisions and to whom they are extending credit. This is achieved through a robust data collection and reporting mechanism that has evolved significantly since the act’s inception. The underlying philosophy is that an informed public and vigilant regulators are essential to maintaining a fair and competitive housing market.

The Mandate for Data Collection

The cornerstone of HMDA is the requirement for financial institutions to collect and report specific data points about each mortgage loan application they receive, whether approved or denied, and about originated loans. This data includes information about the applicant, the property, and the loan itself. The types of institutions covered by HMDA are broadly defined and include banks, credit unions, mortgage companies, and other entities that originate or purchase mortgages. The scope of institutions and loan types subject to HMDA reporting has expanded over time to ensure comprehensive coverage of the mortgage market.

The data collected is extensive and designed to capture a wide array of factors that could influence lending decisions. This includes:

- Applicant Demographics: Information such as race, ethnicity, sex, and age of the applicant. This is crucial for identifying potential disparities in lending based on protected characteristics.

- Loan Characteristics: Details about the loan amount, loan type (e.g., conventional, FHA, VA), interest rate, term, and whether it’s a fixed-rate or adjustable-rate mortgage.

- Property Information: The location of the property (census tract), its type (e.g., single-family, multi-family), and whether it is owner-occupied.

- Lender Information: Details about the financial institution making the lending decision, including its asset size and location.

- Action Taken: Whether the application was approved, denied, withdrawn, or originated.

- Denial Reasons: If an application was denied, specific reasons for denial are reported.

The Purpose: Combating Discriminatory Lending

The primary driver behind HMDA is the desire to prevent and address discriminatory lending practices. Historically, marginalized communities, particularly minority groups, faced significant barriers to obtaining mortgages, often due to practices like redlining. Redlining involved lenders refusing to lend in certain geographic areas, typically those with a high concentration of minority residents, thereby denying these communities access to capital and hindering their economic development.

HMDA provides the data necessary to detect and investigate such discriminatory patterns. By analyzing HMDA data, regulators can identify:

- Disparities in Approval Rates: Whether certain demographic groups are disproportionately denied mortgage applications compared to others, even when controlling for other relevant factors like creditworthiness.

- Geographic Disparities: Whether lending activity is concentrated in certain neighborhoods and absent in others, potentially indicating redlining.

- Differences in Loan Terms: Whether certain groups are offered less favorable loan terms, such as higher interest rates or fees.

The act doesn’t inherently prohibit lending decisions; rather, it mandates transparency to ensure those decisions are made on legitimate, non-discriminatory grounds.

The HMDA Reporting and Data Analysis Process

The effectiveness of HMDA hinges on a rigorous process of data collection, submission, and analysis. This process ensures that the information gathered is accurate, comprehensive, and ultimately useful for its intended purposes.

Who is Required to Report?

The entities obligated to report HMDA data are diverse and encompass a significant portion of the mortgage lending industry. Generally, financial institutions that meet certain asset size thresholds and originate or purchase a specific number of mortgage loans are subject to HMDA reporting requirements. These can include:

- Banks: Federally insured depository institutions, including commercial banks and savings associations.

- Credit Unions: Federally insured credit unions.

- Mortgage Lenders: Non-bank mortgage originators and purchasers, often referred to as mortgage companies or independent mortgage bankers.

- Other Financial Institutions: Certain other entities that engage in mortgage lending.

The specific thresholds and criteria are periodically reviewed and updated by regulatory agencies to ensure that the reporting requirements keep pace with the evolving financial landscape. For instance, the Consumer Financial Protection Bureau (CFPB) plays a key role in setting and enforcing these regulations.

The Data Submission Mechanism

Once the data is collected, it must be submitted to the appropriate federal regulatory agencies. The CFPB is the primary administrator of HMDA data collection and enforcement. Financial institutions are required to submit their HMDA data annually, typically by March 1st of the year following the calendar year in which the loan applications were received or loans were originated.

The submission process involves using specific software or online portals provided by the CFPB. This standardized approach ensures consistency in data formatting and facilitates efficient processing. Accuracy and completeness are paramount; errors or omissions can lead to penalties. Institutions are responsible for the quality of the data they submit, and the CFPB conducts reviews and audits to verify its accuracy.

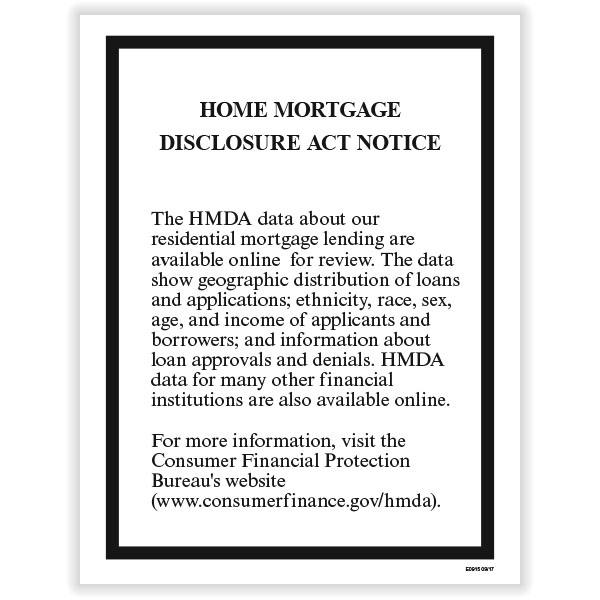

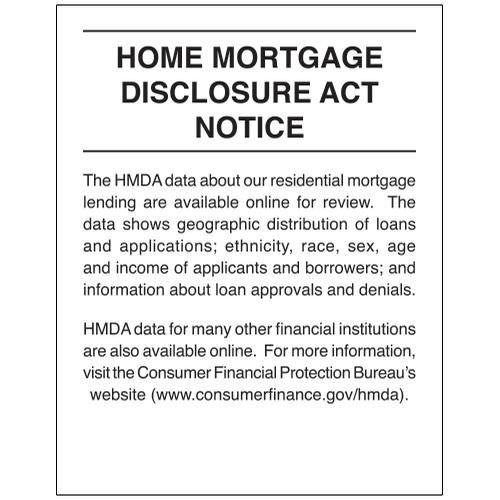

Public Access and Data Utilization

A critical aspect of HMDA is the public accessibility of the collected data. After a period of aggregation and processing, the CFPB releases the HMDA data to the public. This transparency allows researchers, community advocates, journalists, and the general public to analyze lending patterns and identify areas of concern.

The utilization of HMDA data is multifaceted:

- Regulatory Oversight: Regulators use the data to identify potential compliance issues and conduct targeted investigations into lenders exhibiting concerning lending patterns.

- Policy Development: Policymakers use the data to inform the development of new legislation, regulations, and programs aimed at promoting fair housing and increasing access to credit.

- Community Advocacy: Advocacy groups use the data to highlight disparities and push for greater accountability from lenders and policymakers.

- Academic Research: Researchers conduct in-depth studies on mortgage markets, discrimination, and the impact of lending practices on communities.

- Industry Self-Assessment: Lenders themselves can use the data to benchmark their performance against industry averages and identify areas where they might be inadvertently engaging in discriminatory practices.

The availability of this rich dataset has been instrumental in driving conversations and actions towards a more inclusive mortgage market.

Evolution and Impact of HMDA

HMDA has not remained static since its enactment. It has undergone significant reforms and expansions to adapt to changes in the financial industry and to strengthen its effectiveness in combating discrimination. The impact of HMDA has been profound, influencing lending practices, regulatory oversight, and public awareness of housing finance issues.

Key Reforms and Enhancements

Over the years, HMDA has been amended and updated to enhance its data collection capabilities and to broaden its scope. One of the most significant reforms occurred with the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010, which transferred primary responsibility for HMDA administration to the CFPB.

Subsequent rulemakings by the CFPB have further refined HMDA:

- Expansion of Data Points: The number and types of data points collected have been significantly increased to provide a more granular understanding of lending activities. This includes new fields related to loan pricing, underwriting, borrower characteristics, and property details.

- Inclusion of More Lenders: The thresholds for reporting have been adjusted, bringing more smaller institutions under the HMDA reporting umbrella.

- Consideration of Potential Discrimination: The act’s focus has sharpened to better enable the identification of pricing discrimination and other subtle forms of bias. New data elements aim to capture more information about the terms and conditions of loans.

- Clarification of Definitions: Regulatory guidance has been issued to clarify definitions of terms such as “application,” “originated,” and “denied,” ensuring more consistent reporting across institutions.

These reforms have been driven by a recognition that the mortgage market is dynamic and that effective anti-discrimination efforts require up-to-date and comprehensive data.

Measuring the Impact of HMDA

The impact of HMDA is evident in several key areas:

- Increased Transparency: HMDA has brought an unprecedented level of transparency to the mortgage market. The public availability of detailed lending data has made it more difficult for lenders to engage in covert discriminatory practices without detection.

- Deterrence of Discrimination: The knowledge that their lending activities are being monitored and publicly reported acts as a significant deterrent against discriminatory behavior. Lenders are more likely to adhere to fair lending laws when they know their practices are subject to scrutiny.

- Informed Policy and Regulation: The data generated by HMDA has been instrumental in shaping housing finance policy and regulation. It provides empirical evidence to support or refute claims of discrimination and guides the development of targeted interventions.

- Empowerment of Communities: Community organizations and advocates have leveraged HMDA data to identify lending gaps and disparities in their neighborhoods. This data has been a powerful tool for engaging with lenders and policymakers to advocate for more equitable access to credit.

- Improved Lending Practices: The insights gleaned from HMDA data have encouraged many lenders to review and improve their internal underwriting and lending processes to ensure fairness and compliance with fair lending laws.

While HMDA is a powerful tool, it is not a panacea. Identifying discrimination is often complex, and the data requires careful analysis to account for legitimate factors that influence lending decisions. However, its contribution to promoting a fairer and more accessible housing market is undeniable.

Conclusion: HMDA’s Enduring Role in Fair Housing

The Home Mortgage Disclosure Act stands as a testament to the power of data-driven policy in combating discrimination and promoting equitable access to essential financial services. By mandating the collection and public disclosure of mortgage lending data, HMDA has created a crucial mechanism for oversight, accountability, and informed action. Its evolution reflects a commitment to adapting to the complexities of the modern financial landscape and to strengthening its effectiveness in fostering a housing market where all individuals have a fair opportunity to secure homeownership. As the financial industry continues to evolve, HMDA will undoubtedly remain a cornerstone of fair housing policy, ensuring that transparency and fairness are central to the American dream of homeownership.