The Savings Incentive Match Plan for Employees Individual Retirement Account, commonly known as a SIMPLE IRA, stands as a critical retirement savings vehicle, particularly designed for small businesses and their employees. Far from complex, its very name, “SIMPLE,” reflects its core philosophy: to provide an accessible, low-cost, and straightforward retirement savings solution that benefits both employers and their workforce. Understanding the intricacies of a SIMPLE IRA is essential for small business owners considering their options and for employees evaluating their long-term financial planning.

Understanding the Foundation: What Defines a SIMPLE IRA?

At its heart, a SIMPLE IRA is a tax-advantaged retirement plan that allows both employers and employees to contribute to individual retirement accounts. It’s an attractive alternative to more complex plans like a 401(k) for businesses that may not have the resources or desire to manage the extensive administrative burdens associated with larger plans. The IRS established SIMPLE IRAs to encourage retirement savings among smaller entities, fostering financial security for a broader segment of the working population.

Eligibility and Employer Requirements

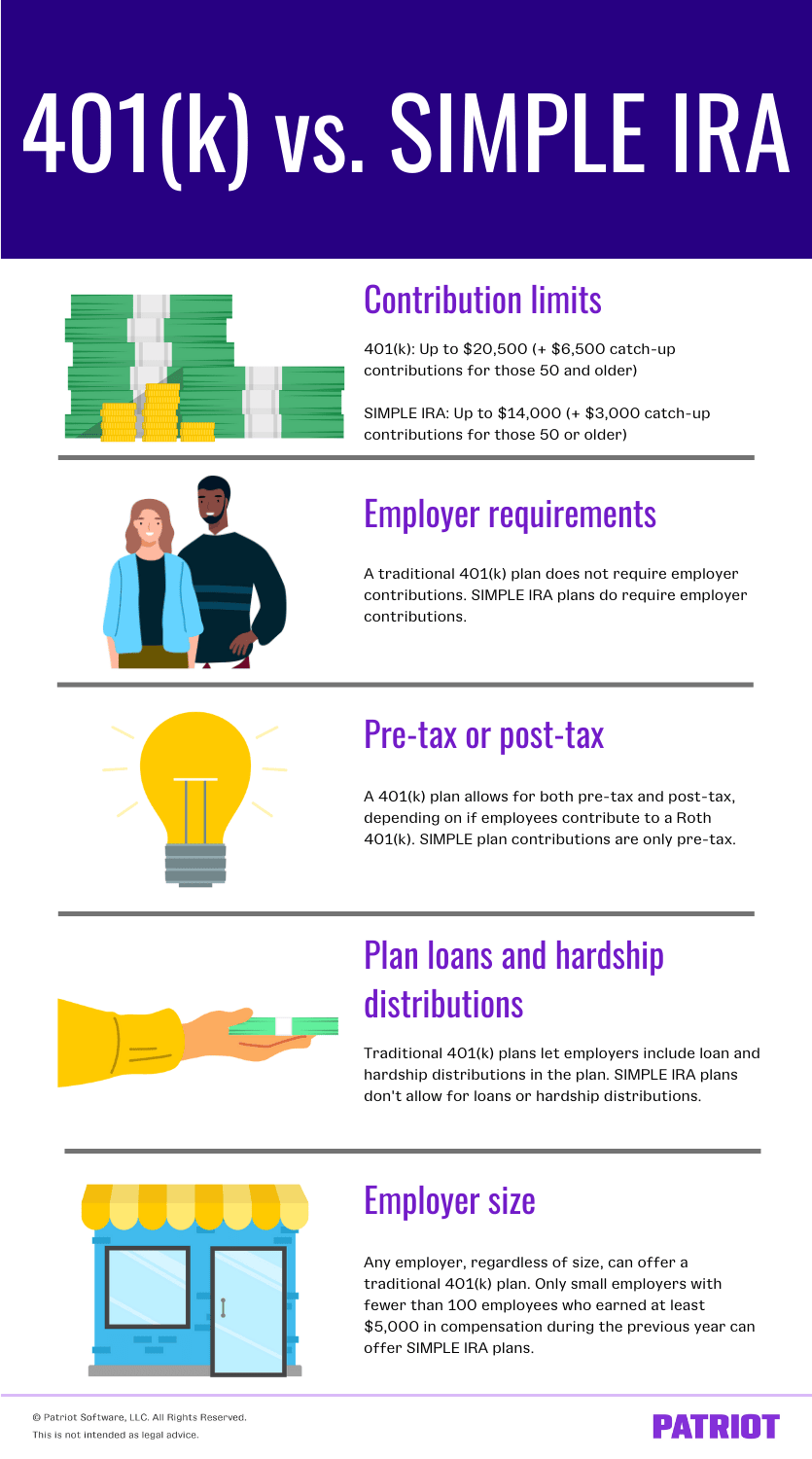

For a business to establish a SIMPLE IRA plan, it must meet specific eligibility criteria. Foremost, the employer must have 100 or fewer employees who received at least $5,000 in compensation during the preceding calendar year. This threshold ensures the plan remains focused on small to medium-sized enterprises. Crucially, a business cannot maintain any other qualified retirement plan (like a 401(k), SEP IRA, or profit-sharing plan) during the same calendar year that it maintains a SIMPLE IRA. This exclusivity is a key feature, preventing overlapping retirement benefits and simplifying compliance.

All eligible employees, defined as those who earned at least $5,000 in any two preceding calendar years and are reasonably expected to earn at least $5,000 in the current year, must be offered the opportunity to participate. Employers cannot exclude any eligible employee, ensuring broad participation and equitable access to retirement savings within the company. This inclusive nature is a cornerstone of the SIMPLE IRA’s design, emphasizing widespread benefit rather than selective access.

Contribution Limits and Structure

The contribution structure of a SIMPLE IRA is unique and mandates employer contributions, making it particularly beneficial for employees. There are two primary types of contributions:

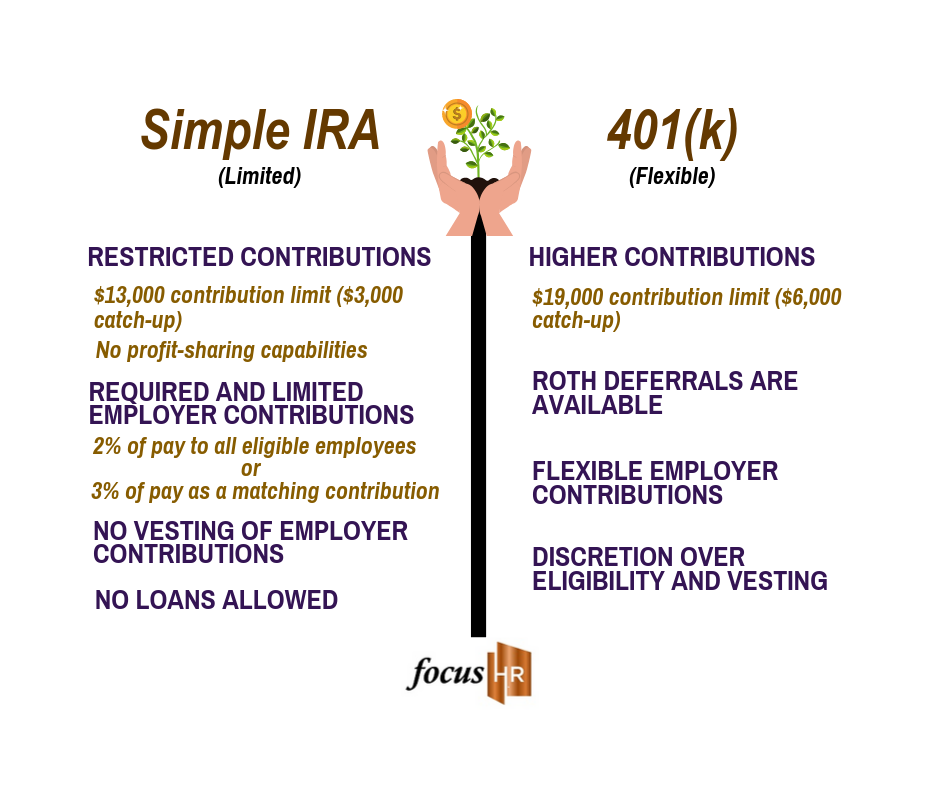

- Employee Salary Deferrals: Employees can elect to contribute a percentage of their compensation, up to a specific annual limit. For 2024, this limit is $16,000, with an additional catch-up contribution of $3,500 allowed for those aged 50 and over. These contributions are made on a pre-tax basis, meaning they reduce the employee’s taxable income in the year they are made, similar to traditional 401(k) contributions.

- Employer Contributions: Employers are required to make contributions, choosing between two options:

- Matching Contributions: The employer must match employee salary deferrals dollar-for-dollar, up to 3% of the employee’s compensation. This 3% match can be reduced to as low as 1% in two out of five years, but it provides a strong incentive for employees to save.

- Non-Elective Contributions: Alternatively, the employer can contribute a fixed 2% of each eligible employee’s compensation, regardless of whether the employee chooses to make their own salary deferrals. This 2% contribution is based on up to $345,000 (for 2024) of the employee’s compensation.

These mandatory employer contributions are a significant advantage for employees, guaranteeing a boost to their retirement savings even if their personal contributions are modest. The specific contribution limits are adjusted periodically by the IRS to account for inflation, so staying informed of the current year’s limits is crucial. All contributions, both employee and employer, grow tax-deferred until withdrawal in retirement.

Advantages and Disadvantages for Small Businesses

For a small business, choosing the right retirement plan involves balancing cost, administrative burden, and employee benefits. The SIMPLE IRA offers a compelling proposition but also comes with certain limitations that warrant careful consideration.

Benefits for Employers

The primary draw for small businesses considering a SIMPLE IRA is its simplicity and low administrative cost. Unlike 401(k) plans, SIMPLE IRAs are not subject to the complex discrimination testing rules that often plague larger plans, which can be time-consuming and expensive to manage. This lack of complex testing significantly reduces compliance burdens and professional fees for plan administration. Employers also face fewer fiduciary responsibilities compared to 401(k) plans, as employees typically choose their own investments from a range offered by the financial institution.

Furthermore, employer contributions to a SIMPLE IRA are tax-deductible, which can reduce the business’s taxable income. This provides a direct financial incentive for offering the plan. By providing a retirement plan, even a small business can enhance its employee recruitment and retention efforts. In a competitive job market, offering retirement benefits can significantly boost a company’s attractiveness to prospective employees and improve morale among current staff, fostering loyalty and reducing turnover. The ability to offer a robust benefit without the corresponding administrative overhead is a clear win for many small businesses.

Drawbacks to Consider

Despite its advantages, the SIMPLE IRA is not without its limitations. The most notable drawback for employers is the mandatory employer contribution. Unlike some other plans where employer contributions might be discretionary, a business establishing a SIMPLE IRA is legally obligated to either match employee contributions (up to 3%) or make a non-elective 2% contribution for every eligible employee. This commitment represents a fixed cost that must be factored into the business’s financial planning, regardless of profitability in a given year. For businesses with tight margins or fluctuating revenues, this mandatory contribution can be a significant burden.

Another potential limitation is the lower contribution limits compared to 401(k) plans. While suitable for many small businesses, highly compensated employees or owners who wish to defer a larger portion of their income might find the limits restrictive. This can make the SIMPLE IRA less appealing to businesses where key personnel aim for aggressive, high-limit retirement savings. Finally, the exclusive plan rule means that a business cannot have any other qualified retirement plan concurrently. This lack of flexibility might be a disadvantage if the business grows and wishes to offer a more sophisticated or varied suite of retirement benefits in the future, requiring a full transition away from the SIMPLE IRA.

Employee Perspective: How a SIMPLE IRA Impacts You

For employees, a SIMPLE IRA offers a straightforward and often beneficial pathway to retirement savings. It provides tax advantages, employer contributions, and relative ease of management, making it an accessible tool for building long-term wealth.

Vesting and Portability

One of the most attractive features of a SIMPLE IRA for employees is the immediate 100% vesting of all contributions, both employee and employer. “Vesting” refers to the employee’s ownership of the funds contributed to the plan. Immediate vesting means that as soon as a contribution is made to an employee’s SIMPLE IRA, those funds immediately belong to the employee, with no waiting period. This is a significant advantage over many 401(k) plans, which often have graded vesting schedules that require employees to work for a company for several years before fully owning employer-contributed funds. Immediate vesting ensures that employees always walk away with all the retirement savings accumulated in their SIMPLE IRA, regardless of how long they remain with the employer.

Furthermore, SIMPLE IRAs boast excellent portability. Since contributions are made to individual IRAs established in the employee’s name, these accounts are generally easy to roll over into other IRA accounts (like a Traditional or Roth IRA) or even into a new employer’s qualified retirement plan (like a 401(k)) once the employee leaves the company and has met the two-year rule (avoiding early withdrawal penalties). This ease of transferability means that an employee’s retirement savings are not tied to a specific employer, providing flexibility and continuity in their financial planning journey.

Investment Options

While the employer chooses the financial institution that will hold the SIMPLE IRA accounts, employees typically have control over their investment choices within their individual account. The chosen financial institution (e.g., a bank, mutual fund company, or brokerage firm) will offer a range of investment options, such as mutual funds, exchange-traded funds (ETFs), stocks, bonds, and money market accounts. This self-directed investment power allows employees to tailor their portfolio to their personal risk tolerance, financial goals, and time horizon. This contrasts with some employer-sponsored plans where investment choices might be more restricted or managed by the plan administrator. However, it also means employees bear the responsibility for making informed investment decisions and monitoring their portfolio’s performance. Financial literacy and periodic review are therefore important for maximizing the potential growth of a SIMPLE IRA.

Comparing SIMPLE IRAs with Other Retirement Plans

Understanding where a SIMPLE IRA fits within the broader landscape of retirement savings options is crucial for both employers and employees to make informed decisions. Each plan type caters to different needs and circumstances.

SIMPLE IRA vs. Traditional/Roth IRA

The key distinction between a SIMPLE IRA and a personal Traditional or Roth IRA lies primarily in the employer contribution component and contribution limits. Traditional and Roth IRAs are individual plans, meaning only the individual can contribute to them. There are no employer contributions. While Traditional and Roth IRAs offer tax advantages (pre-tax contributions for Traditional, tax-free withdrawals in retirement for Roth), their annual contribution limits are significantly lower than those for a SIMPLE IRA. For 2024, the Traditional/Roth IRA limit is $7,000 ($8,000 for those 50 and over), whereas a SIMPLE IRA allows for employee deferrals of $16,000 ($19,500 for those 50 and over), plus mandatory employer contributions. Thus, for an employee whose employer offers a SIMPLE IRA, it provides a much more robust savings capacity than relying solely on a personal IRA. However, if no employer plan is available, or if an individual wants to save beyond their employer plan, a Traditional or Roth IRA serves as an excellent supplementary option.

SIMPLE IRA vs. 401(k) and SEP IRA

When comparing a SIMPLE IRA to other employer-sponsored plans like a 401(k) or a SEP IRA, different trade-offs emerge.

SIMPLE IRA vs. 401(k):

- Administrative Complexity: SIMPLE IRAs are significantly less complex and have lower administrative costs than 401(k) plans. 401(k)s often involve extensive compliance testing, higher setup fees, and ongoing administration.

- Contribution Limits: 401(k) plans generally allow for much higher employee salary deferrals (e2024: $23,000, plus $7,500 catch-up) and total contributions (including employer and employee, up to $69,000 for 2024, plus $7,500 catch-up) compared to SIMPLE IRAs. This makes 401(k)s more attractive for high-income earners seeking to maximize tax-deferred savings.

- Employer Contributions: While both require employer contributions, 401(k) employer contributions can often be more flexible or discretionary, whereas SIMPLE IRA employer contributions are mandatory and follow strict rules.

- Plan Eligibility: 401(k)s do not have the 100-employee limit, making them suitable for businesses of all sizes.

SIMPLE IRA vs. SEP IRA:

- Employee Contributions: SEP IRAs are funded exclusively by employer contributions; employees cannot make salary deferrals. This is a critical difference from SIMPLE IRAs, where employees can contribute.

- Contribution Limits: SEP IRAs allow for much higher employer contributions, up to 25% of an employee’s compensation (with a compensation limit), or $69,000 for 2024, whichever is less. This makes SEP IRAs very attractive for business owners who want to contribute a significant amount for themselves and their employees without the employee contribution component.

- Eligibility: SEP IRAs are suitable for businesses of any size, including self-employed individuals, and do not have the 100-employee limit.

- Mandatory Contributions: Unlike SIMPLE IRAs, employer contributions to a SEP IRA are generally discretionary each year, meaning the employer can choose whether or not to contribute and how much.

In essence, a SIMPLE IRA strikes a balance, offering more savings capacity and employer contributions than a personal IRA, more simplicity and lower cost than a 401(k), and employee contribution opportunities that a SEP IRA lacks, all while maintaining a focus on small business needs.

Setting Up and Managing a SIMPLE IRA Plan

Establishing and maintaining a SIMPLE IRA is designed to be user-friendly, aligning with its “simple” moniker. However, certain steps and ongoing responsibilities are necessary to ensure compliance and proper administration.

Key Steps for Implementation

The process of setting up a SIMPLE IRA plan generally involves a few straightforward steps:

- Choose a Financial Institution: The employer must select a financial institution (such as a bank, mutual fund company, or brokerage firm) to hold the SIMPLE IRA accounts. The institution will provide the necessary plan documents.

- Complete Plan Documents: The employer will sign a plan agreement, typically IRS Form 5305-SIMPLE or a similar prototype plan provided by the financial institution. This document outlines the terms and conditions of the plan.

- Notify Employees: The employer is responsible for notifying all eligible employees about the establishment of the SIMPLE IRA plan and their right to participate. This notification must occur before the employee’s election period, usually 60 days prior to January 1st of the year the plan becomes effective, or as soon as administratively feasible for new hires. The notice must include information about contribution limits, the employer contribution formula, and the employee’s right to make contributions and select investments.

- Establish Individual Accounts: Each participating employee must establish an individual SIMPLE IRA account with the chosen financial institution.

- Begin Contributions: Once accounts are set up and elections are made, the employer begins deducting employee salary deferrals from payroll and remitting them, along with their mandatory employer contributions, to the employees’ respective SIMPLE IRA accounts.

Ongoing Compliance and Administration

While simpler than a 401(k), a SIMPLE IRA still requires ongoing administration to maintain its qualified status. The primary responsibilities include:

- Timely Deposit of Contributions: Employers must deposit employee salary deferrals into their SIMPLE IRA accounts as soon as administratively feasible, but no later than 30 days following the end of the month in which the amounts were withheld from pay. Employer contributions must be made by the due date of the employer’s income tax return, including extensions.

- Annual Employee Notification: Each year, the employer must provide eligible employees with a notice (often provided by the financial institution) regarding their right to make salary deferrals, the contribution limits, and the employer contribution method for the upcoming year. This typically needs to be done before the annual 60-day election period, which usually runs from November 2nd to December 31st for the following year.

- Adherence to Eligibility Rules: Employers must continuously monitor employee eligibility to ensure all qualifying employees are offered participation and that the business continues to meet the 100-employee limit. If the employee count exceeds 100, the business typically has a two-year grace period to transition to another retirement plan.

- No Annual IRS Filings: A significant administrative advantage of SIMPLE IRAs is that employers generally do not need to file annual reports (like Form 5500 series) with the IRS, as is required for most other qualified plans, further reducing administrative burdens.

By diligently following these steps and responsibilities, small businesses can effectively leverage the SIMPLE IRA to provide a valuable retirement benefit, fostering financial well-being for their employees and reinforcing the company’s commitment to its workforce.