When the term “rider” is mentioned in the context of insurance, it’s crucial to understand that it doesn’t refer to the pilot of a drone, nor to the person being transported on a motorcycle. Instead, in the realm of insurance, a “rider” is an addendum or endorsement that modifies the terms of an existing insurance policy. It’s essentially a supplementary clause that provides additional coverage or alters specific aspects of the original contract. Think of it as a customizable feature for your insurance, allowing you to tailor your protection to your specific needs and circumstances.

The concept of rider insurance is prevalent across various insurance types, including life insurance, health insurance, and property insurance. However, in the context of understanding the term broadly, and to delve into its functional aspects, we can categorize its application and significance. This exploration will focus on how riders function, their common types, and the strategic advantages they offer to policyholders.

The Fundamental Mechanics of Insurance Riders

At its core, an insurance rider is an amendment that can be attached to a primary insurance policy. It is not a standalone policy but rather an integral part of an existing contract. The purpose of a rider is to enhance, limit, or clarify the coverage provided by the original policy. This means that the terms and conditions outlined in the rider become legally binding as part of the overall insurance agreement. Understanding these mechanics is paramount for policyholders to fully leverage their insurance protection.

How Riders are Introduced and Incorporated

The process of adding a rider to an insurance policy typically begins with the policyholder expressing a need for specific additional coverage or modification. This request is then submitted to the insurance provider. The insurer will assess the request, considering the risk associated with the proposed changes and the existing policy terms. If approved, the rider will be drafted with specific clauses detailing the new coverage, its cost, and any exclusions. This rider is then officially attached to the policy, often requiring an adjustment in the premium. The rider becomes an official part of the policy document, and all its provisions are legally enforceable.

The Impact of Riders on Policy Premiums and Terms

The addition of a rider almost invariably affects the policy’s premium. Since riders provide additional benefits or coverage, they represent an increased risk for the insurer. Consequently, the premium will likely increase to compensate for this expanded liability. The amount of the premium increase depends on the type of rider, the extent of coverage it provides, and the assessed risk. For instance, a rider that offers comprehensive accidental death benefit coverage will likely have a more significant impact on the premium than a rider that simply waives certain fees under specific conditions. Beyond premiums, riders can also alter the policy’s terms. This might include introducing new definitions, specifying conditions under which certain benefits are payable, or defining specific circumstances that are excluded from coverage.

Common Applications and Types of Insurance Riders

The versatility of insurance riders allows them to address a wide spectrum of potential needs and risks. While the specific names and availability of riders can vary significantly between different insurance companies and policy types, certain categories are widely recognized for their utility. Examining these common types provides a practical understanding of how riders enhance insurance protection.

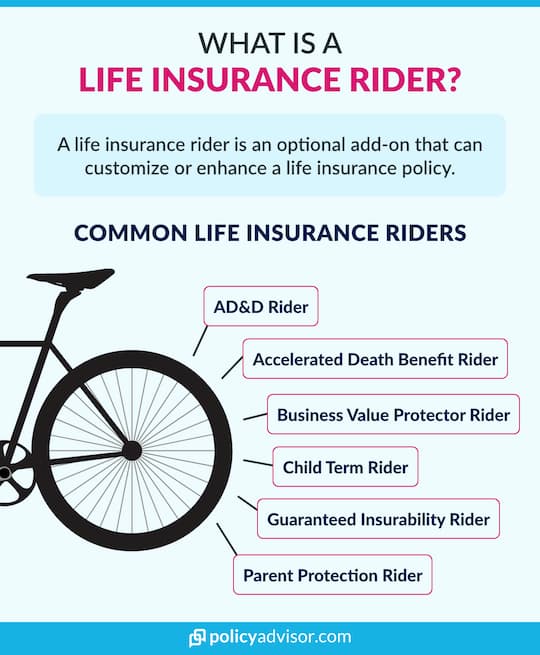

Riders in Life Insurance Policies

Life insurance riders are among the most popular, offering policyholders the ability to customize their death benefit coverage and financial security.

Accelerated Death Benefit Rider

This rider allows the policyholder to receive a portion of the death benefit in advance if they are diagnosed with a terminal illness. This can provide crucial financial support for medical expenses or end-of-life care, without needing to surrender the policy.

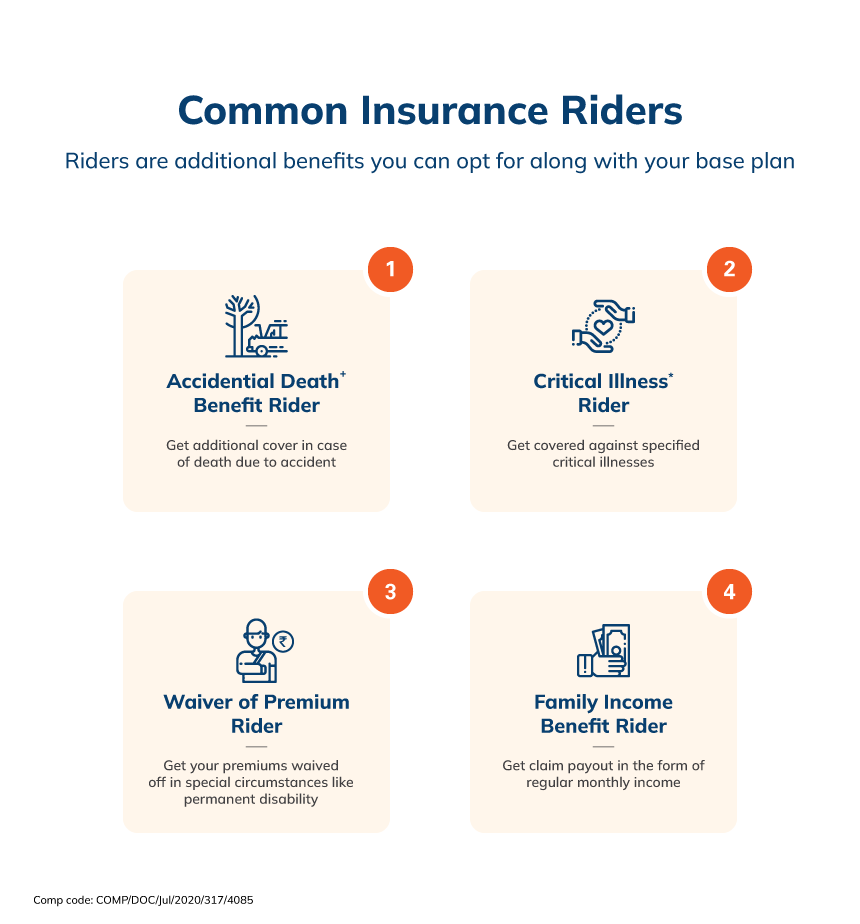

Waiver of Premium Rider

If the policyholder becomes totally disabled and is unable to work, this rider waives future premium payments. The policy remains in force as if premiums were still being paid, ensuring that the death benefit is not compromised during a period of financial hardship.

Accidental Death Benefit (ADB) Rider

This rider provides an additional death benefit if the insured dies as a direct result of an accident. This is often a multiple of the base death benefit, offering enhanced protection against accidental fatalities.

Child Term Rider

This rider allows the policyholder to add term life insurance coverage for their children to their own life insurance policy. This provides a death benefit for the child, which can be converted into a permanent policy later, often without a medical exam.

Riders in Health Insurance Policies

Health insurance riders serve to broaden the scope of coverage beyond standard medical benefits, addressing specific health needs or enhancing existing benefits.

Critical Illness Rider

This rider pays out a lump sum benefit if the insured is diagnosed with a specific critical illness, such as cancer, heart attack, or stroke, as defined by the policy. This benefit can be used to cover medical expenses, loss of income, or other needs.

Hospital Cash Benefit Rider

This rider provides a daily cash allowance for each day the insured is hospitalized, regardless of other insurance coverage. This can help offset costs not covered by the primary health insurance, such as travel expenses for family members or increased living expenses during hospitalization.

Maternity Benefit Rider

This rider covers expenses related to pregnancy, childbirth, and newborn care. It can include coverage for prenatal check-ups, delivery costs, and postnatal care, often with a waiting period before benefits become available.

Riders in Property and Casualty Insurance

While less common under the explicit term “rider” in property insurance compared to life and health, endorsements and extensions serve a similar function, adding specific coverage to a homeowner’s or auto policy.

Valuable Items Endorsement (Floater)

This endorsement, often referred to as a “rider” in common parlance, provides specific coverage for high-value items like jewelry, art, or electronics that may exceed the limits of the standard homeowner’s policy. It typically offers broader coverage with fewer exclusions.

Water Backup and Sump Pump Overflow Coverage

This endorsement adds coverage for damages caused by water backing up through sewers or drains, or from the overflow of a sump pump. Standard policies often exclude such damages.

Identity Theft Protection Rider

This rider offers assistance and reimbursement for expenses incurred in restoring one’s identity if it is stolen. This can include costs for legal fees, credit monitoring, and lost wages.

Strategic Considerations for Utilizing Insurance Riders

The decision to add riders to an insurance policy is a strategic one that requires careful evaluation of individual circumstances, financial goals, and risk tolerance. Understanding the benefits and potential drawbacks of riders is essential for making informed choices that optimize insurance protection.

Assessing Individual Needs and Risk Exposure

The primary driver for considering insurance riders should be a thorough assessment of personal needs and potential risks. For example, an individual with a family and a high-deductible life insurance policy might consider an accidental death benefit rider to provide an extra layer of financial security for their dependents in the event of a tragic accident. Similarly, someone with a family history of certain critical illnesses might find a critical illness rider invaluable for peace of mind and financial preparedness. It’s about identifying potential gaps in existing coverage and finding riders that effectively fill those voids.

Evaluating the Cost-Benefit Analysis of Riders

While riders offer enhanced protection, they come at an additional cost, increasing the overall premium. It is crucial to conduct a cost-benefit analysis before adding any rider. This involves weighing the increased premium against the potential benefits and the likelihood of the event the rider covers occurring. For instance, a waiver of premium rider might be a wise investment for someone whose income is their primary financial asset and who has limited savings to cover expenses during a period of disability. However, for someone with substantial savings and robust employer-provided disability insurance, the additional cost of such a rider might not be justified. Comparing quotes from different insurers for the same rider can also help ensure you’re getting a competitive price.

Understanding Exclusions and Limitations

It is imperative to read and understand the specific terms, conditions, exclusions, and limitations of any rider before purchasing it. Riders, like primary policies, are not all-encompassing. There might be specific circumstances under which a rider’s coverage will not apply. For example, an accidental death benefit rider may have exclusions for deaths resulting from certain activities like skydiving or engaging in acts of war. Similarly, a critical illness rider will have a defined list of illnesses it covers, and if a diagnosis falls outside this list, the benefit will not be paid. Thoroughly reviewing the policy documents and clarifying any doubts with the insurance provider is essential to avoid unexpected disappointments.

In conclusion, rider insurance represents a powerful tool for policyholders to personalize and fortify their insurance coverage. By understanding how riders function, exploring the diverse types available, and approaching their selection with strategic consideration, individuals can ensure their insurance policies provide the most comprehensive and tailored protection for their unique life circumstances.