In the intricate world of finance, particularly within the realm of real estate and asset-backed securitization, understanding complex debt structures is paramount. Among these, “qualified nonrecourse” debt stands out as a pivotal concept, often misunderstood yet critical for both borrowers and lenders. This article delves into the essence of qualified nonrecourse debt, dissecting its characteristics, implications, and common applications within the financial landscape.

Understanding Recourse vs. Nonrecourse Debt

Before dissecting “qualified nonrecourse,” it’s essential to grasp the fundamental difference between recourse and nonrecourse debt. This distinction lies in the lender’s rights and remedies in the event of a borrower’s default.

Recourse Debt

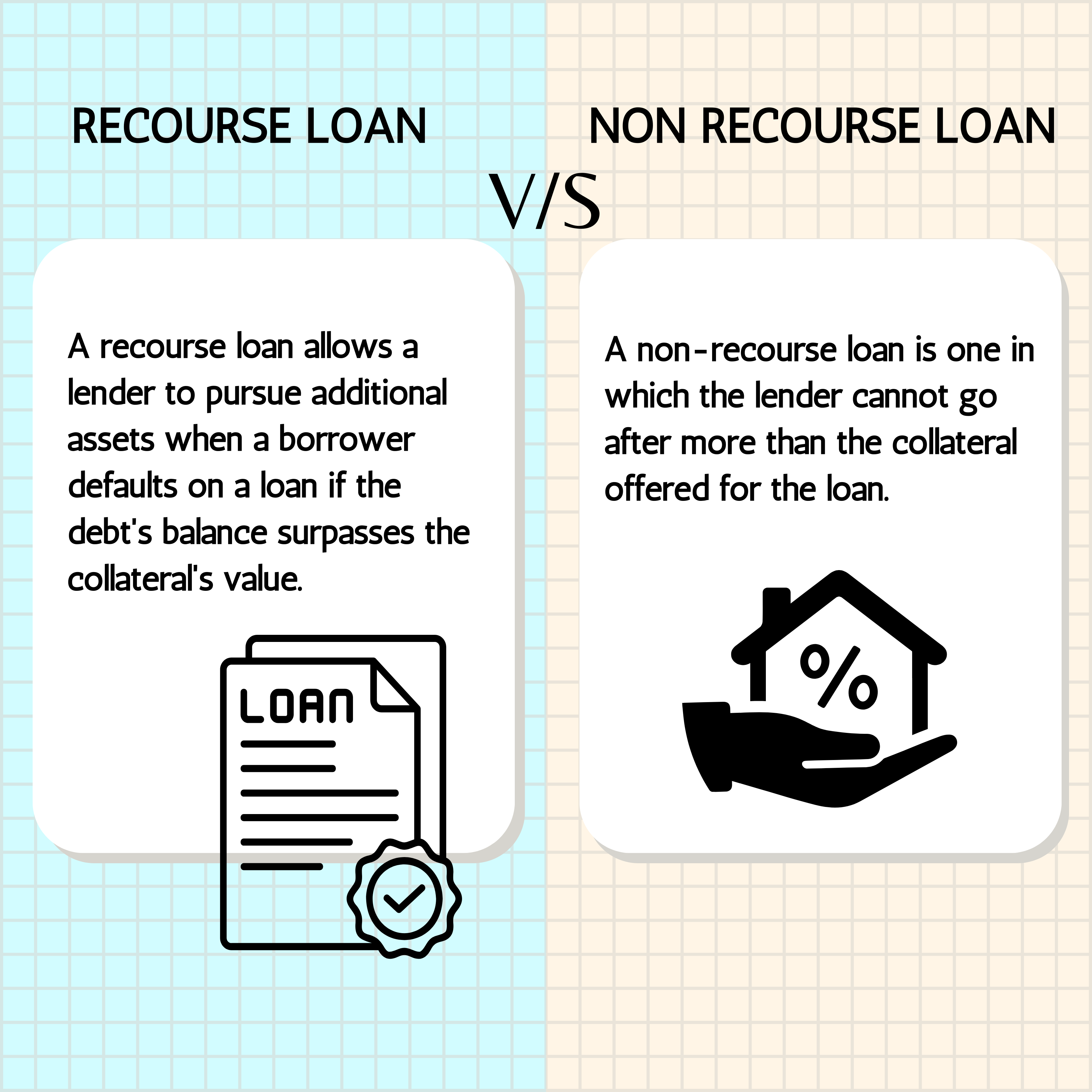

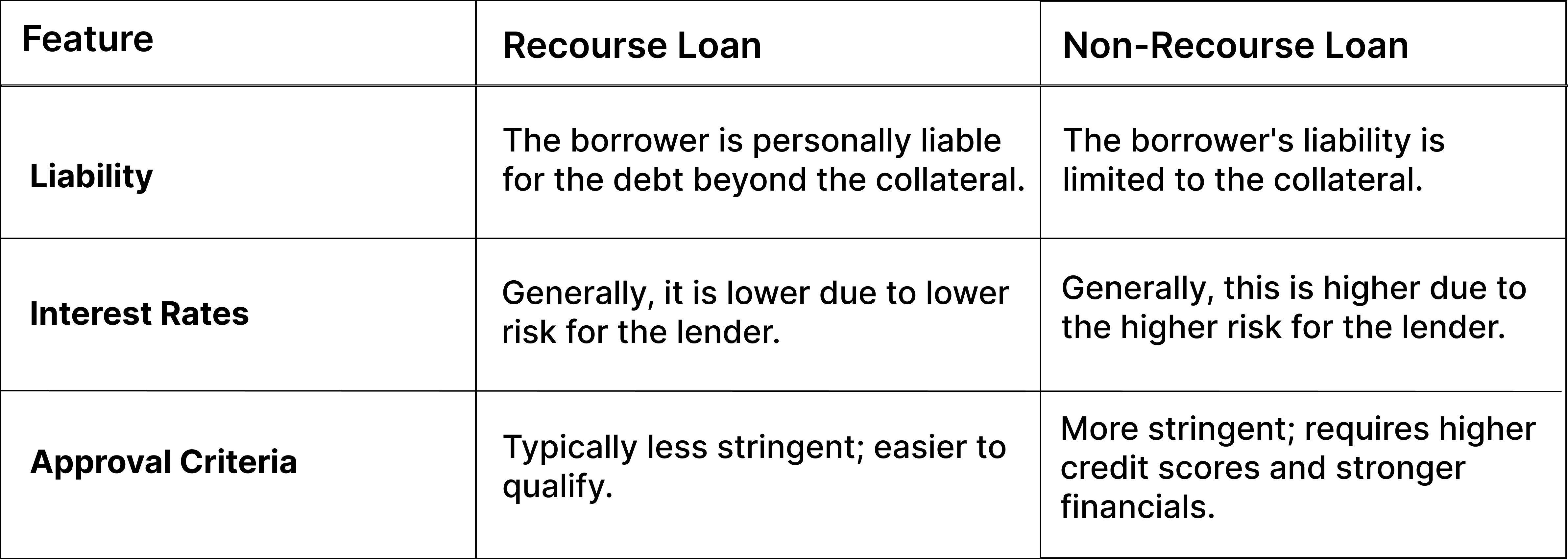

In a recourse loan, the borrower is personally liable for the entire debt, even if the collateral securing the loan is insufficient to cover the outstanding balance. If a borrower defaults on a recourse loan and the sale of the collateral (e.g., a property) at foreclosure does not yield enough to satisfy the debt, the lender can pursue the borrower’s other assets – such as savings accounts, investments, or even future income – to recover the shortfall. This personal liability offers a greater degree of security for the lender, as it expands their recovery options beyond the specific asset pledged as collateral.

Nonrecourse Debt

Conversely, nonrecourse debt limits the lender’s recourse solely to the collateral securing the loan. If the borrower defaults and the collateral’s value is less than the outstanding debt, the lender can only seize and sell the collateral. They cannot pursue the borrower’s personal assets for any deficiency. This structure provides a significant benefit to the borrower, shielding their other assets from potential claims in case of default. However, nonrecourse loans typically come with higher interest rates and stricter lending criteria due to the increased risk for the lender.

Defining Qualified Nonrecourse Debt

Qualified nonrecourse debt introduces a specific set of conditions and protections that make a typically nonrecourse loan even more advantageous for certain borrowers, particularly in the context of tax law and specific investment structures. The “qualified” aspect signifies that the loan meets particular criteria, usually defined by tax regulations, to be treated as truly nonrecourse for specific purposes, most notably for the calculation of basis in an asset for tax depreciation and gain/loss recognition.

The “Qualified” Criteria

The precise definition of “qualified nonrecourse debt” often originates from tax codes, such as the Internal Revenue Code (IRC) in the United States. For a loan to be considered qualified nonrecourse debt, it must generally satisfy several key conditions:

- Secured by Specific Property: The debt must be secured by property that is used in a trade or business or for the production of income. This typically excludes personal-use property.

- Loan Terms: The loan terms must be commercially reasonable and similar to those that would be offered by unrelated lenders for similar property. This implies an arm’s-length transaction.

- No Personal Liability: The borrower (or a related party) cannot assume personal liability for the debt. The lender’s only recourse must be to the specific property securing the loan.

- No Contingent Payments: The amount of the debt must be fixed or adjustable only based on a market interest rate. It cannot be contingent on future profits or the borrower’s income generated from the property.

- Limited Lender-Borrower Relationship: There should be no pre-existing relationship between the borrower and the lender that would suggest the terms are not arm’s length, and the lender must be actively engaged in the business of lending.

- Reasonable Loan-to-Value Ratio: The loan-to-value (LTV) ratio must be reasonable. While specific thresholds can vary, excessively high LTVs may indicate a loan that is not truly at arm’s length or is structured to circumvent nonrecourse principles.

The primary purpose of these qualifications is to ensure that the debt is a genuine financing arrangement and not a disguised equity investment or a means to artificially inflate the tax basis of an asset.

Implications of Qualified Nonrecourse Debt

The distinction between ordinary nonrecourse debt and qualified nonrecourse debt carries significant financial and tax implications.

Tax Basis and Depreciation

One of the most crucial implications of qualified nonrecourse debt is its inclusion in the tax basis of an asset. For real estate investments, for instance, a borrower can include the amount of qualified nonrecourse debt in their basis for the property. This increased basis is vital for calculating depreciation deductions, which can significantly reduce taxable income. Without the “qualified” status, a portion or all of the nonrecourse debt might not be includible in the basis, thereby limiting the depreciation benefits.

Recognition of Gains and Losses

The treatment of debt in the calculation of an asset’s basis also affects the recognition of capital gains and losses when the asset is sold. A higher basis, partly attributable to qualified nonrecourse debt, results in a lower gain (or a larger loss) upon disposition. This can be a strategic advantage for investors seeking to manage their tax liabilities.

Investment Structures

Qualified nonrecourse debt is often a feature of sophisticated investment vehicles, such as:

- Real Estate Syndications: Investors in real estate partnerships or syndications can benefit from qualified nonrecourse debt when the partnership incurs such debt to acquire income-producing properties. The debt increases the investors’ share of the partnership’s basis, enhancing their tax benefits.

- Master Limited Partnerships (MLPs): Certain MLPs, particularly those in the energy sector, may utilize qualified nonrecourse debt in their financing structures.

- Leveraged Buyouts (LBOs): While LBOs often involve a mix of debt types, qualified nonrecourse debt can play a role in acquiring specific income-producing assets within a larger transaction, providing tax advantages for the acquiring entity.

Qualified Nonrecourse Debt in Real Estate

Real estate is perhaps the most common arena where qualified nonrecourse debt plays a significant role. For investors acquiring commercial properties, rental apartments, or other income-generating real estate, a significant portion of the purchase price is often financed through debt.

Commercial Property Acquisition

When an entity acquires a commercial office building or a retail complex, the financing is frequently structured as nonrecourse debt. However, to maximize tax benefits, such as depreciation deductions on the building’s structure, the debt must meet the “qualified” criteria. Lenders specializing in commercial real estate finance are well-versed in these requirements and can structure loans accordingly.

Rental Property Investments

For individual investors or smaller entities acquiring apartment buildings or other residential rental properties, the concept of qualified nonrecourse debt is equally relevant. The debt used to finance the acquisition of these income-producing assets can be included in the investor’s tax basis, allowing for depreciation deductions that can offset rental income.

Special Purpose Entities (SPEs)

Often, particularly in larger real estate transactions, the borrowing entity is a Special Purpose Entity (SPE) or Special Purpose Vehicle (SPV). This legal structure is created specifically for the acquisition and ownership of the property. Loans made to these SPEs are typically structured as nonrecourse to the ultimate beneficial owners, and if they meet the IRS criteria, they become qualified nonrecourse debt, providing the intended tax benefits.

Navigating the Nuances

The determination of whether a loan qualifies as “qualified nonrecourse debt” can be complex and is subject to specific tax laws and interpretations. Borrowers and investors should always seek advice from qualified tax professionals and legal counsel to ensure that their financing arrangements meet all necessary criteria.

Key Considerations for Borrowers

- Documentation: Ensure all loan documentation clearly reflects the nonrecourse nature of the debt and adheres to the specific requirements outlined by tax authorities.

- Loan-to-Value Ratios: Be mindful of LTV ratios, as excessively high ratios can raise questions about the arm’s-length nature of the transaction.

- Related-Party Transactions: Avoid arrangements that could be construed as related-party transactions, which may invalidate the qualified nonrecourse status.

- Purpose of the Loan: Confirm that the loan is being used to acquire or improve property used for trade or business or the production of income.

Lender’s Perspective

Lenders offering what they deem to be nonrecourse loans will also need to ensure their structures meet the “qualified” criteria if they expect those loans to be treated as such for tax purposes by the borrower. This involves careful underwriting, clear loan documentation, and potentially structuring the loan through specific lending vehicles designed to comply with tax regulations.

In conclusion, qualified nonrecourse debt is a critical financial instrument that provides significant tax advantages by allowing borrowers to include the debt amount in the tax basis of their income-producing assets. Understanding its definition, implications, and the specific criteria it must meet is essential for anyone involved in real estate investment, asset-backed securitization, or other ventures where such debt structures are employed. It represents a sophisticated tool for optimizing financial outcomes and managing tax liabilities within the framework of financial and tax law.