Understanding the intricacies of mortgage financing is crucial for aspiring homeowners, and among the various elements, Private Mortgage Insurance (PMI) often emerges as a point of confusion. For loans backed by the Federal Housing Administration (FHA), this concept is known as Mortgage Insurance Premium (MIP), serving a distinct but analogous purpose. Far from being an optional add-on, MIP is an integral component of nearly all FHA loans, designed to protect lenders and enable a broader spectrum of individuals to achieve homeownership.

Understanding FHA Loans and Their Appeal

FHA loans are a popular option for first-time homebuyers and those with less-than-perfect credit or limited down payment funds. Backed by the U.S. government, these loans offer more lenient qualification requirements compared to conventional mortgages. The FHA does not directly lend money; instead, it insures loans made by FHA-approved lenders. This government backing significantly reduces the risk for lenders, encouraging them to provide mortgages to borrowers who might otherwise be deemed too risky.

![]()

The primary appeal of FHA loans lies in their accessibility. Borrowers can qualify with a minimum down payment as low as 3.5% (for credit scores of 580 or higher), making homeownership attainable for many who struggle to save the larger down payments typically required for conventional loans. Furthermore, FHA guidelines are generally more forgiving regarding credit history, debt-to-income ratios, and bankruptcies or foreclosures that occurred several years prior.

The Role of FHA Insurance

The insurance provided by the FHA is the cornerstone of its program. Without this insurance, lenders would be hesitant to offer loans with such favorable terms to a demographic segment that traditionally carries higher perceived risk. When a borrower defaults on an FHA-insured loan, the FHA compensates the lender for their loss, up to a certain amount. This protection is not free, however. It is funded directly by the borrowers themselves through the payment of Mortgage Insurance Premiums (MIP). Therefore, MIP is not a benefit to the borrower in the traditional sense; rather, it’s the cost of the government guarantee that allows the loan to exist in the first place, benefiting the borrower by making homeownership accessible.

The Mechanics of FHA Mortgage Insurance Premiums (MIP)

FHA Mortgage Insurance Premiums are structured into two distinct components: an upfront premium and an annual premium. Both are mandatory for the vast majority of FHA loans and contribute to the FHA’s Mutual Mortgage Insurance Fund (MMIF), which is used to pay claims to lenders in the event of borrower default.

Upfront Mortgage Insurance Premium (UFMIP)

The Upfront Mortgage Insurance Premium (UFMIP) is a one-time fee paid at the time of closing. This premium is calculated as a percentage of the total loan amount. While it’s paid “upfront,” borrowers typically don’t need to bring this cash to the closing table. Instead, UFMIP is almost always financed directly into the loan amount. For example, if the UFMIP is 1.75% and the loan amount is $200,000, the UFMIP would be $3,500. This amount would then be added to the principal balance, making the total loan $203,500. Financing the UFMIP means the borrower’s monthly mortgage payment will be slightly higher, as they are paying interest on the financed premium over the life of the loan. This financing mechanism allows borrowers to benefit from the FHA program without needing an even larger sum of cash at closing.

Annual Mortgage Insurance Premium (Annual MIP)

In addition to the UFMIP, FHA loan borrowers also pay an Annual Mortgage Insurance Premium (Annual MIP). Despite its name, this premium is not paid as a single lump sum each year. Instead, it is calculated annually as a percentage of the outstanding loan balance and then divided into twelve equal installments, which are added to the borrower’s monthly mortgage payment.

The annual MIP rate can vary based on several factors, including the loan-to-value (LTV) ratio at the time of origination, the loan term (e.g., 15-year vs. 30-year), and the original loan amount. For most FHA loans with a 30-year term and a down payment of less than 10%, the annual MIP is typically a consistent percentage for the entire duration it is required. This monthly charge ensures that the FHA fund remains adequately capitalized to cover potential defaults, acting as a continuous risk mitigation measure for lenders.

Why FHA Loans Require MIP

The mandatory nature of MIP for FHA loans stems from the fundamental mission of the FHA: to expand access to homeownership for a broader demographic. This mission inherently involves taking on higher risks than conventional lenders typically would without government backing.

Mitigating Lender Risk

At its core, MIP serves as a critical risk mitigation tool for lenders. By insuring a significant portion of the loan, the FHA reduces the potential financial exposure for banks and mortgage companies. This protection is especially vital for loans with low down payments or for borrowers with credit profiles that might not meet conventional lending standards. Without MIP, lenders would face greater risk of loss if a borrower defaults, making them far less likely to offer such favorable terms or even to originate these loans at all. MIP essentially transfers a significant portion of the default risk from the individual lender to the collective fund managed by the FHA.

Facilitating Homeownership

The direct consequence of this risk mitigation is the increased availability of mortgages for eligible borrowers. Because lenders are protected by the FHA insurance, they are willing to offer loans with features designed to make homeownership more accessible, such as lower down payment requirements, more flexible credit criteria, and competitive interest rates. Therefore, while MIP adds to the cost of an FHA loan, it is the mechanism that facilitates the FHA’s ability to help millions of Americans purchase homes who might otherwise be priced out of the market or unable to qualify for traditional financing. It bridges the gap between the perceived risk of a borrower and a lender’s willingness to extend credit.

Duration and Removal of FHA MIP

One of the most significant differences between FHA MIP and conventional PMI lies in its duration and the conditions under which it can be removed. FHA MIP often lasts for the entire life of the loan, depending on when the loan was originated and the initial loan-to-value (LTV) ratio. This perpetual nature is a key consideration for borrowers evaluating FHA vs. conventional financing.

Loans Originated On or After June 3, 2013

For FHA loans originated on or after June 3, 2013, the rules regarding MIP duration are quite stringent:

- If the original loan-to-value (LTV) was 90% or less (meaning a down payment of 10% or more): The Annual MIP will be collected for 11 years. After 11 years, if the loan is still active, the MIP obligation ceases.

- If the original loan-to-value (LTV) was greater than 90% (meaning a down payment of less than 10%): The Annual MIP will be collected for the entire life of the loan. This means borrowers will pay MIP for as long as they have the FHA loan, whether it’s 30 years or until they sell or refinance.

This policy adjustment aimed to strengthen the FHA’s financial reserves following the 2008 housing crisis. For many FHA borrowers who put down the minimum 3.5%, this means paying MIP indefinitely, significantly impacting the total cost of their mortgage over time.

Loans Originated Before June 3, 2013

FHA loans originated prior to June 3, 2013, operate under different rules. For these loans, borrowers typically had the ability to cancel Annual MIP once their loan-to-value (LTV) ratio reached 78% (based on the original amortization schedule) or after five years, whichever came later, provided they had made on-time payments. This older policy offered a clear path to MIP removal, making these legacy FHA loans more appealing in terms of long-term cost.

Refinancing as an Exit Strategy

Given that most FHA loans originated today require MIP for the life of the loan, many borrowers view refinancing as the primary strategy to eliminate their MIP obligation. Once a homeowner builds sufficient equity in their property (typically 20% or more) and improves their credit profile, they can often refinance their FHA loan into a conventional loan. Conventional loans, unlike FHA loans, allow for the cancellation of Private Mortgage Insurance (PMI) once 20% equity is achieved. This makes refinancing a powerful tool for reducing monthly housing costs for FHA borrowers who have improved their financial standing and increased their home’s equity.

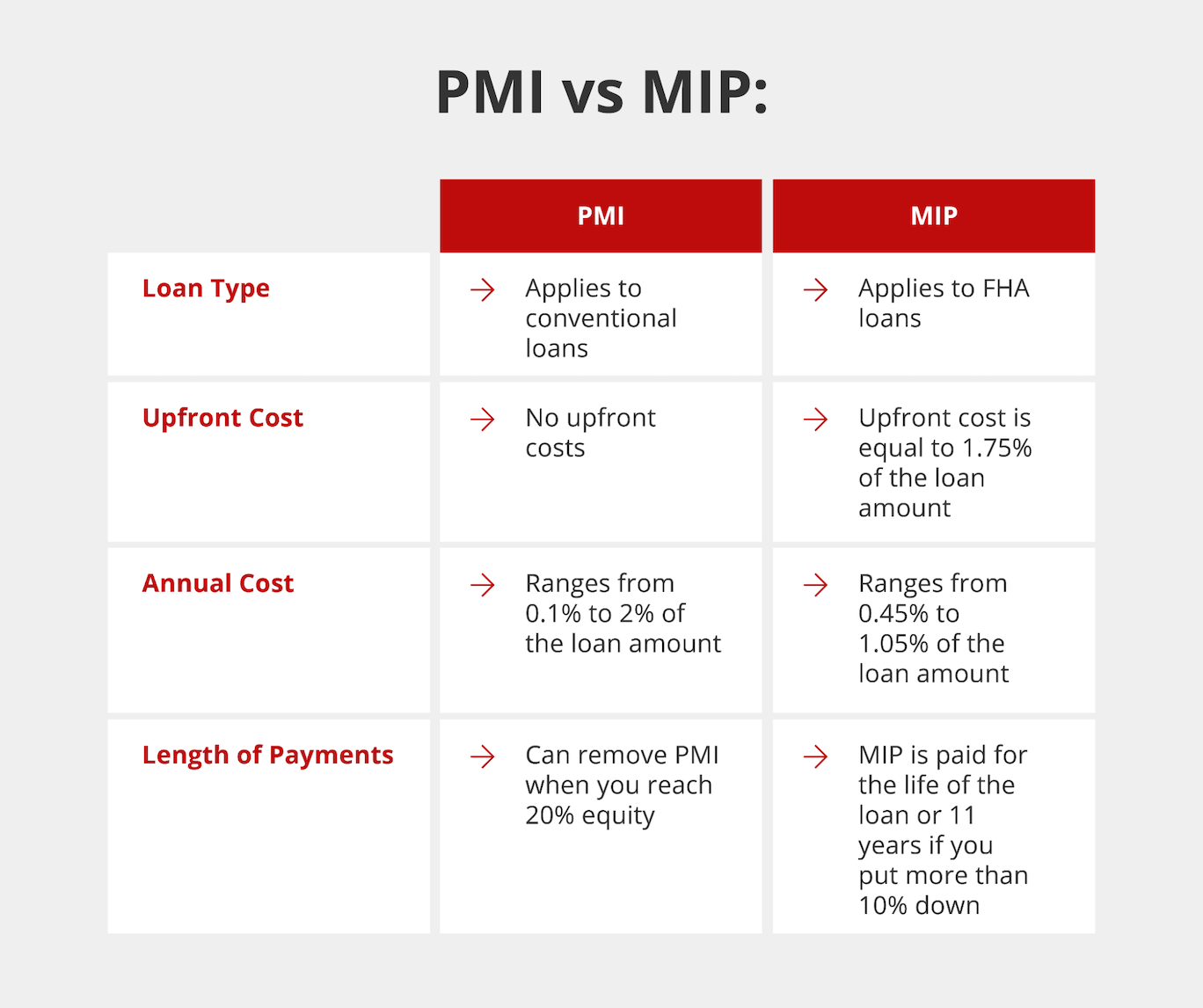

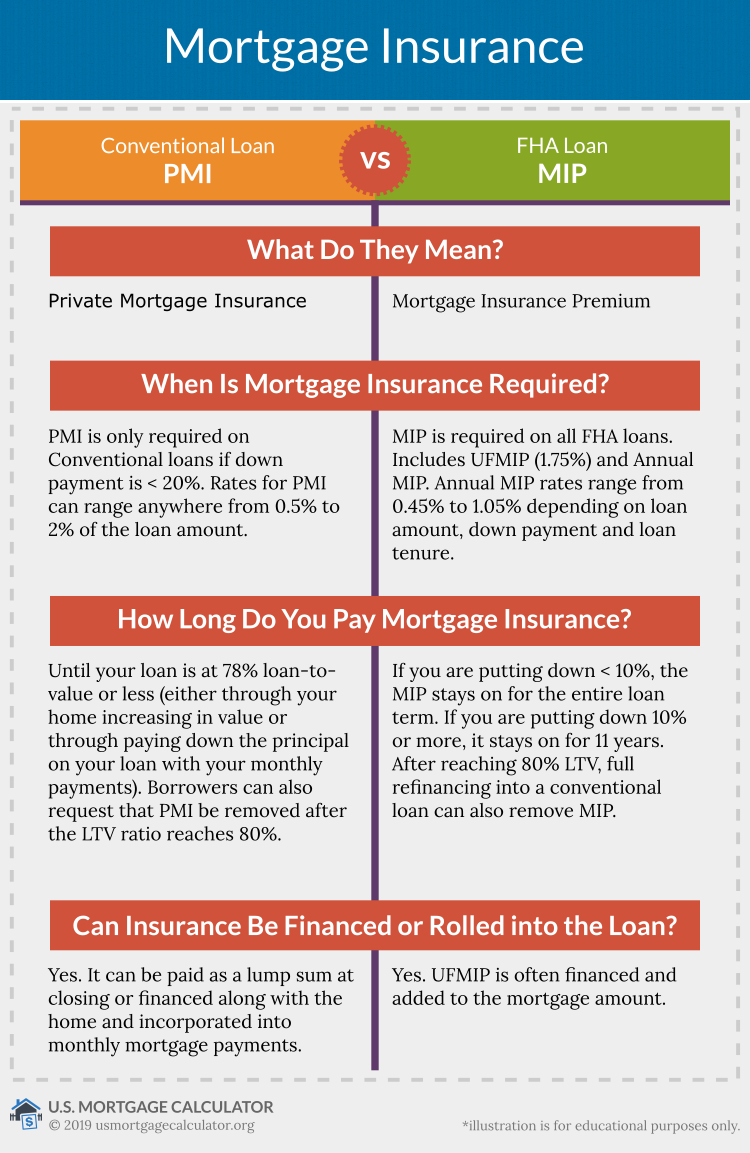

Comparing FHA MIP to Conventional PMI

While both FHA MIP and conventional PMI serve to protect lenders against borrower default, there are crucial distinctions in their structure, cost, and cancellation policies. Understanding these differences is key when choosing between FHA and conventional financing options.

Key Differences in Structure and Duration

- Mandatory Upfront Premium: FHA loans always require an Upfront Mortgage Insurance Premium (UFMIP), which is typically financed into the loan. Conventional loans do not have an upfront PMI component; any PMI is paid solely through monthly installments.

- Annual Premium Calculation: FHA annual MIP is calculated on the original loan amount for its duration (though it recalculates based on the declining balance, the rate is fixed to the initial LTV/term). Conventional PMI is calculated on the outstanding loan balance and generally becomes cheaper over time as the principal balance decreases.

- Cancellation Policy: This is arguably the most significant difference.

- FHA MIP: For most FHA loans originated today (low down payment, post-2013), annual MIP is for the life of the loan and cannot be canceled unless the borrower refinances out of the FHA loan. If the initial LTV was 90% or less, it might cancel after 11 years.

- Conventional PMI: By federal law (Homeowners Protection Act of 1998), conventional PMI must be automatically canceled by the lender once the borrower reaches 78% LTV based on the original amortization schedule. Borrowers can also request cancellation once they reach 80% LTV, often requiring an appraisal to verify current home value. This provides a clear path to eliminating the insurance payment.

- Cost: While specific rates vary, FHA MIP generally tends to be more expensive over the long term, especially if it’s paid for the life of the loan, compared to conventional PMI which can be canceled. However, FHA loans often have lower interest rates, which can partially offset the MIP cost in the initial years.

In essence, FHA loans offer greater accessibility but often come with a more enduring and potentially higher total cost for mortgage insurance. Conventional loans, while requiring higher credit scores and down payments, provide a defined path to cancel PMI, potentially leading to lower long-term housing expenses. Borrowers must weigh these trade-offs carefully based on their individual financial situation and homeownership goals.