The world of investing, particularly in derivatives like options, can seem complex and laden with jargon. Understanding these terms is crucial for any investor looking to leverage these sophisticated financial instruments. Among the most fundamental concepts in options trading is the “strike price.” This seemingly simple number holds immense power, dictating the terms of an option contract and significantly influencing its potential profitability.

In essence, the strike price is the predetermined price at which the underlying asset (such as a stock, ETF, or commodity) can be bought or sold by the option holder. It’s a cornerstone of the option contract, established at the time of its creation. For every option contract, there will be a specific strike price associated with it. This price acts as a reference point for whether the option will be “in the money,” “at the money,” or “out of the money” upon expiration. Mastering the concept of the strike price is the first step towards comprehending how options function and how traders can strategically utilize them.

Understanding the Mechanics of Strike Price

The strike price is not a random figure; it is carefully chosen by market makers and is typically set at or around the current market price of the underlying asset. For instance, if a company’s stock is trading at $100 per share, a common strike price for an option on that stock might be $100. However, options are also available with strike prices above and below the current market price, offering different risk-reward profiles.

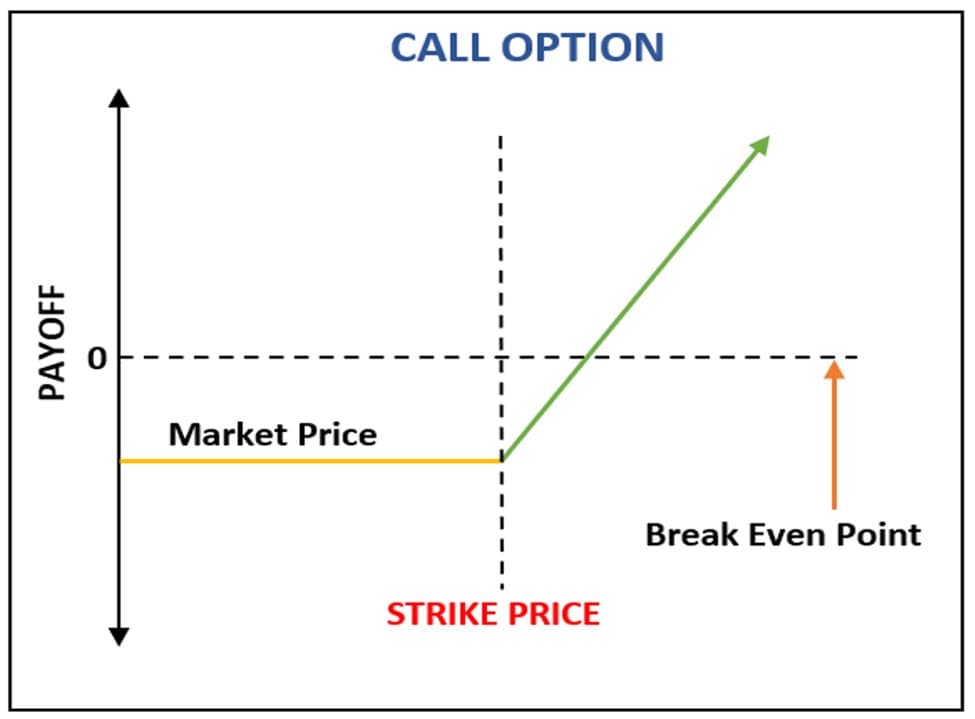

Call Options and Strike Price

For a call option, the strike price represents the maximum price at which the holder has the right to buy the underlying asset. If an investor believes the price of a stock will rise, they might buy a call option. The profitability of this call option is directly tied to how far the stock price moves above the strike price by the expiration date.

Let’s consider an example. Suppose Stock XYZ is trading at $50, and you purchase a call option with a strike price of $55. This means you have the right, but not the obligation, to buy 100 shares of Stock XYZ at $55 per share before the option expires.

- If Stock XYZ rises to $60 by expiration: Your option is “in the money.” You can exercise your right to buy the shares at $55 and immediately sell them in the market for $60, making a profit (minus the premium paid for the option). The profit per share would be $60 (market price) – $55 (strike price) = $5.

- If Stock XYZ remains at $50 or falls below $55 by expiration: Your option is “out of the money” or “at the money.” It would be financially disadvantageous to exercise your right to buy at $55 when you can buy it cheaper on the open market. In this scenario, the option would likely expire worthless, and you would lose the premium you paid for it.

The difference between the market price of the underlying asset and the strike price is often referred to as the “intrinsic value” of the option. For a call option, intrinsic value is calculated as: Max(0, Market Price - Strike Price).

Put Options and Strike Price

For a put option, the strike price represents the maximum price at which the holder has the right to sell the underlying asset. If an investor believes the price of a stock will fall, they might buy a put option. The profitability of this put option is tied to how far the stock price falls below the strike price by the expiration date.

Using Stock XYZ again, which is trading at $50, let’s say you purchase a put option with a strike price of $45. This grants you the right to sell 100 shares of Stock XYZ at $45 per share before the option expires.

- If Stock XYZ falls to $40 by expiration: Your option is “in the money.” You can exercise your right to sell shares at $45, even though the market price is $40. This allows you to sell at a higher price than the current market, generating a profit (minus the premium paid). The profit per share would be $45 (strike price) – $40 (market price) = $5.

- If Stock XYZ remains at $50 or rises above $45 by expiration: Your option is “out of the money” or “at the money.” It would be financially illogical to sell at $45 when you can sell it for more on the open market. The put option would likely expire worthless, and you would lose the premium.

For a put option, intrinsic value is calculated as: Max(0, Strike Price - Market Price).

Strike Price and Option Pricing

The strike price is a pivotal factor in determining the premium—the price an investor pays to buy an option contract. Options with strike prices that are more “favorable” to the buyer (i.e., “in the money” at the time of purchase or having a higher probability of becoming “in the money”) generally command higher premiums.

In the Money (ITM)

An option is considered “in the money” when it has intrinsic value.

- For a call option: It is ITM if the underlying asset’s market price is above the strike price.

- For a put option: It is ITM if the underlying asset’s market price is below the strike price.

ITM options typically have higher premiums because they already possess a certain level of value.

At the Money (ATM)

An option is “at the money” when the underlying asset’s market price is equal to or very close to the strike price. ATM options have little to no intrinsic value, and their premiums are primarily composed of “extrinsic value” (time value and implied volatility).

Out of the Money (OTM)

An option is “out of the money” when it has no intrinsic value.

- For a call option: It is OTM if the underlying asset’s market price is below the strike price.

- For a put option: It is OTM if the underlying asset’s market price is above the strike price.

OTM options are the cheapest because they require a significant price movement in the underlying asset to become profitable. Their premiums are almost entirely made up of extrinsic value.

The Role of Strike Price in Strategy

The choice of strike price is fundamental to an options trading strategy. Different strike prices offer varying levels of risk and potential reward, catering to diverse investor objectives.

Speculative Trading

For speculative traders looking for leveraged gains, out-of-the-money (OTM) options are often favored. These options are cheaper, meaning a smaller initial investment can control a larger amount of the underlying asset. However, they carry a higher risk of expiring worthless, as the underlying asset must move significantly in the desired direction to overcome the strike price and the premium paid.

For example, an investor might buy a deeply OTM call option if they anticipate a substantial, rapid price increase in a stock due to an upcoming event like an earnings report or product launch. The potential for a large percentage return on investment is high if the prediction is correct.

Hedging and Income Generation

Conversely, investors looking to hedge existing positions or generate income might opt for at-the-money (ATM) or even in-the-money (ITM) options.

- Hedging: An investor holding a stock might buy put options with strike prices close to the current market price to protect against a potential downturn. If the stock price falls, the profit from the put option can offset some of the losses in the stock.

- Income Generation (Covered Calls/Cash-Secured Puts): Traders who own stock might sell (write) call options against their holdings. If the stock price stays below the strike price, the option expires worthless, and the trader keeps the premium received, thus generating income. Similarly, selling put options can generate income, but it comes with the obligation to buy the stock if the price falls below the strike price.

The strike price chosen for these strategies dictates the level of protection offered or the income generated. A higher strike price for a covered call means the stock can rise further before being called away, while a lower strike price for a cash-secured put offers more downside protection.

Strike Price Selection and Implied Volatility

Implied volatility (IV) plays a significant role in option premiums, and its interplay with strike price selection is crucial. IV represents the market’s expectation of future price fluctuations of the underlying asset. Higher IV generally leads to higher option premiums across all strike prices.

However, the effect of IV can differ across strike prices. For instance, OTM options are often more sensitive to changes in implied volatility than ITM options. A surge in IV can disproportionately inflate the premiums of OTM options, making them more expensive for speculative bets. Conversely, a drop in IV can significantly reduce the premiums of OTM options, sometimes making them less attractive even if the underlying asset’s price movement is favorable.

Traders must consider implied volatility when selecting strike prices. A strategy that relies on a large price move might become prohibitively expensive if IV is already high. Conversely, if IV is low, it might present an opportunity to buy options at a lower premium, anticipating a rise in volatility or price movement.

Conclusion

The strike price is far more than just a number; it is the very essence of an option contract’s potential. It defines the threshold for profitability, dictates the intrinsic value, and significantly influences the option’s premium. Whether an investor is aiming for aggressive speculation, strategic hedging, or consistent income generation, the careful selection of the strike price is paramount. Understanding how strike prices interact with market movements, expiration dates, and implied volatility empowers investors to navigate the complex landscape of options trading with greater confidence and precision, ultimately enhancing their ability to achieve their financial objectives.