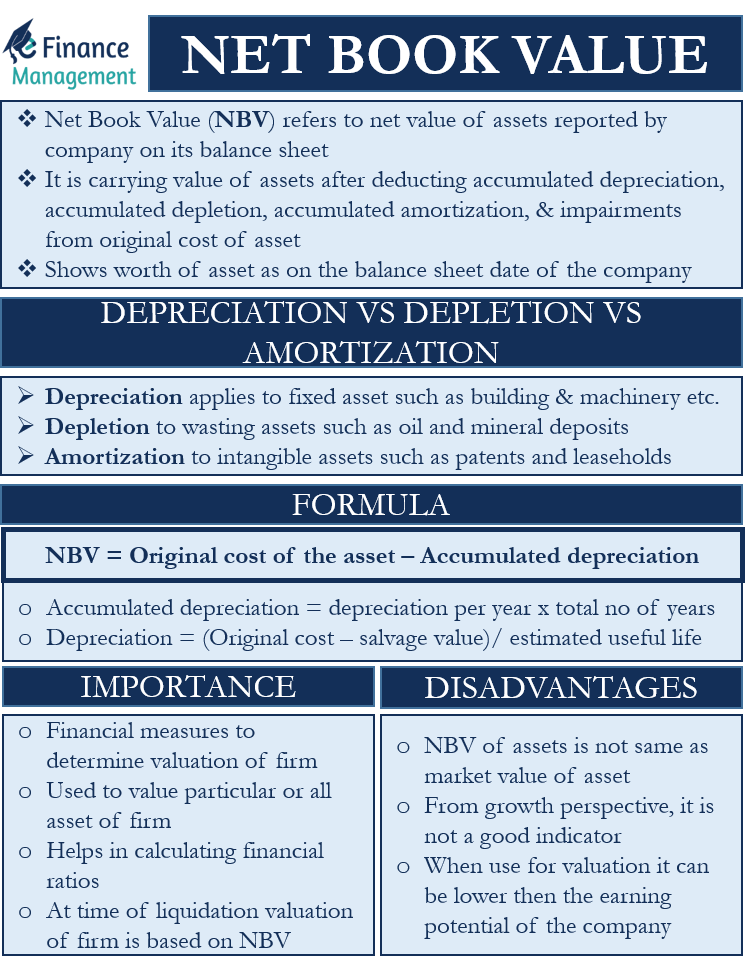

Net Book Value (NBV) is a fundamental accounting concept that represents the value of an asset on a company’s balance sheet after accounting for accumulated depreciation. It’s essentially what an asset is worth on paper at a specific point in time, according to accounting principles. While it doesn’t necessarily reflect the true market value, NBV is crucial for financial reporting, investment analysis, and understanding a company’s asset base.

Understanding the Components of Net Book Value

To grasp Net Book Value, it’s essential to first understand its constituent parts: the original cost of an asset and its accumulated depreciation.

Original Cost

The original cost of an asset, often referred to as its historical cost, is the total expenditure incurred to acquire and prepare the asset for its intended use. This includes not only the purchase price but also any additional costs that are directly attributable to bringing the asset to its working condition. For a drone, this might include:

- Purchase Price: The base cost of the drone itself.

- Shipping and Handling: Costs associated with transporting the drone to the company.

- Taxes and Duties: Any applicable sales tax or import duties.

- Initial Setup and Calibration: Expenses incurred to assemble, configure, and perform initial calibrations to ensure the drone is ready for operation.

- Essential Accessories: Costs of immediate, necessary accessories required for operation, such as initial batteries or a basic controller if not included in the base price.

For more complex drone operations, the original cost might also encompass specialized software or initial training required to operate the specific model. It’s important to note that subsequent upgrades or repairs that extend the asset’s useful life are typically capitalized and added to the original cost, while routine maintenance costs are expensed as incurred.

Depreciation

Depreciation is an accounting method used to allocate the cost of a tangible asset over its useful life. Assets, including drones, inevitably wear out or become obsolete over time. Depreciation allows a company to systematically reduce the asset’s carrying value on the balance sheet, reflecting this gradual loss of value. The key components in calculating depreciation are:

- Cost: The original cost of the asset.

- Salvage Value (Residual Value): The estimated value of the asset at the end of its useful life. For many technological assets like drones, this might be minimal or even zero, especially if they are expected to be fully obsolete or non-functional.

- Useful Life: The estimated period over which the asset is expected to be used by the company. This is often expressed in years, but can also be in operating hours or flight cycles for a drone. Factors influencing useful life include the intensity of use, technological advancements, and maintenance practices.

Accumulated Depreciation

Accumulated depreciation is the total amount of depreciation that has been charged against an asset since it was put into service. It’s a contra-asset account, meaning it reduces the gross value of the asset on the balance sheet. Each accounting period, a portion of the asset’s depreciable cost is recognized as an expense (depreciation expense), and this amount is added to the accumulated depreciation.

For a drone, if a company uses straight-line depreciation (the most common method) and estimates a useful life of 5 years and a salvage value of $0, the annual depreciation expense would be the original cost divided by 5. If the drone was purchased at the beginning of the year and $1,000 was its original cost, the annual depreciation would be $200. After the first year, accumulated depreciation would be $200. After the second year, it would be $400, and so on.

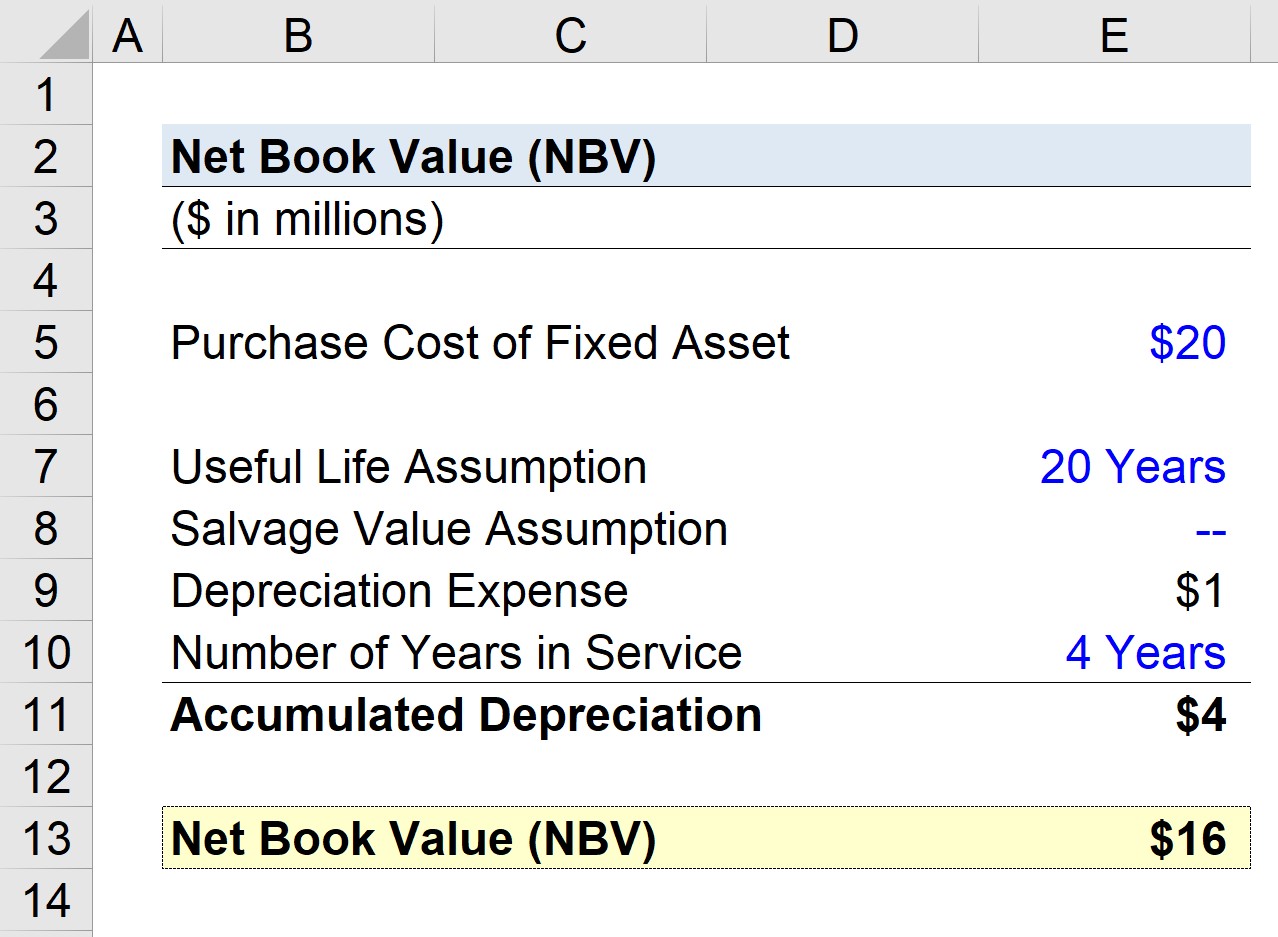

Calculating Net Book Value

The formula for Net Book Value is straightforward:

Net Book Value = Original Cost – Accumulated Depreciation

Let’s illustrate with a drone example. Suppose a company purchased a high-end professional drone for $10,000. They estimate its useful life to be 4 years and its salvage value to be $1,000. Using the straight-line depreciation method:

- Depreciable Cost: Original Cost – Salvage Value = $10,000 – $1,000 = $9,000

- Annual Depreciation Expense: Depreciable Cost / Useful Life = $9,000 / 4 years = $2,250 per year

Now, let’s track the Net Book Value over time:

-

At Purchase (Year 0):

- Original Cost: $10,000

- Accumulated Depreciation: $0

- Net Book Value: $10,000 – $0 = $10,000

-

End of Year 1:

- Original Cost: $10,000

- Accumulated Depreciation: $2,250

- Net Book Value: $10,000 – $2,250 = $7,750

-

End of Year 2:

- Original Cost: $10,000

- Accumulated Depreciation: $2,250 (Year 1) + $2,250 (Year 2) = $4,500

- Net Book Value: $10,000 – $4,500 = $5,500

-

End of Year 3:

- Original Cost: $10,000

- Accumulated Depreciation: $4,500 + $2,250 = $6,750

- Net Book Value: $10,000 – $6,750 = $3,250

-

End of Year 4 (End of Useful Life):

- Original Cost: $10,000

- Accumulated Depreciation: $6,750 + $2,250 = $9,000

- Net Book Value: $10,000 – $9,000 = $1,000 (This equals the salvage value, as expected)

After Year 4, the drone would typically be retired from service. If it were sold, any difference between the sale price and the Net Book Value would be recognized as a gain or loss on disposal.

Why Net Book Value Matters in the Drone Industry

The concept of Net Book Value is particularly relevant for businesses that rely on drones as operational assets. This includes industries such as:

- Aerial Photography and Videography: Companies that provide drone-based visual content for marketing, real estate, or media production.

- Inspection Services: Businesses using drones for inspecting infrastructure like bridges, power lines, wind turbines, or buildings.

- Surveying and Mapping: Firms employing drones for creating detailed topographical maps and 3D models.

- Agriculture: Using drones for crop monitoring, spraying, and precision farming.

- Delivery and Logistics: Companies experimenting with or implementing drone delivery systems.

For these businesses, understanding NBV is critical for several reasons:

Financial Reporting and Taxation

Publicly traded companies are required to report their financial position accurately. The NBV of their drone fleet is a key component of their fixed assets on the balance sheet. This reported value directly impacts profitability calculations and can influence tax liabilities, as depreciation expense is a tax-deductible item. Accurate NBV ensures compliance with accounting standards like GAAP (Generally Accepted Accounting Principles) or IFRS (International Financial Reporting Standards).

Asset Management and Replacement Cycles

NBV provides a quantifiable metric for tracking the remaining value of a drone. As the NBV decreases, it signals that the asset is aging. This information is vital for strategic planning, particularly for determining optimal times for asset replacement. Businesses can use NBV trends to forecast future capital expenditure needs, ensuring they can upgrade their drone technology before it becomes obsolete or unreliable, thereby maintaining operational efficiency and competitiveness. For instance, if a drone’s NBV drops significantly and its maintenance costs begin to rise, it might be a strong indicator for considering a new purchase.

Investment and Financing Decisions

Lenders and investors often scrutinize a company’s asset base when making decisions. The NBV of a company’s drone fleet can be a factor in assessing its overall financial health and the collateral available for loans. A higher NBV might suggest a more robust asset base, potentially improving a company’s creditworthiness. Furthermore, when considering selling or acquiring a drone business, understanding the NBV of the drone assets is a crucial step in valuation.

Insurance Purposes

While insurance policies typically base premiums and payouts on replacement cost or actual cash value (which can be closer to market value), the NBV can serve as a baseline reference. It helps in documenting the asset’s depreciated worth, which can be a point of discussion during insurance claim settlements, especially in cases of partial damage or total loss.

Limitations of Net Book Value

Despite its importance, Net Book Value has significant limitations that users must acknowledge:

Does Not Reflect Market Value

The most critical limitation is that NBV is an accounting construct, not a measure of market value. The actual resale value of a drone can fluctuate significantly due to market demand, technological obsolescence, condition, and brand reputation. A drone with a high NBV might have a low market value if newer, superior models are available, or if it has sustained unrecorded damage. Conversely, a drone with a low NBV might still command a good price in the used market if it’s a sought-after model or in excellent condition.

Accounting Method Dependency

NBV is directly influenced by the depreciation method chosen and the estimates for useful life and salvage value. Different depreciation methods (straight-line, declining balance, sum-of-the-years’ digits) will result in different NBVs at any given point in time. Similarly, aggressive depreciation (shorter useful life, higher salvage value) will lead to a lower NBV faster than conservative depreciation.

Ignores Inflation and Economic Changes

The original cost is a historical figure. NBV does not inherently adjust for inflation or significant economic changes that might affect the replacement cost of the asset in current terms.

Excludes Intangible Factors

NBV only accounts for the tangible asset itself. It does not consider intangible factors that might contribute to an asset’s true operational value, such as proprietary software licenses, established maintenance schedules that prolong life, or the skill of the pilots operating the drone.

Net Book Value vs. Other Valuation Methods

It’s helpful to contrast NBV with other ways of valuing assets:

- Market Value: The price an asset would fetch in an open market transaction between a willing buyer and a willing seller. This is what a drone could actually be sold for today.

- Replacement Cost: The cost to acquire a new asset of similar utility or function. For a drone, this would be the cost of buying a brand-new model with comparable capabilities to the one being valued.

- Liquidation Value: The net amount that could be realized if an asset were sold quickly, often under distressed conditions.

For businesses in the drone industry, understanding all these valuation methods can be beneficial. While NBV is essential for accounting, market value and replacement cost are more relevant for strategic decisions like selling, insuring, or upgrading equipment.

Conclusion

Net Book Value is a cornerstone of accounting, providing a standardized method for representing an asset’s value on a company’s financial statements. For businesses operating with drone fleets, understanding how to calculate and interpret NBV is vital for accurate financial reporting, effective asset management, informed investment decisions, and tax compliance. While it’s crucial to remember that NBV is an accounting measure and may not align with market realities, it remains an indispensable tool for financial stewardship and strategic planning in the dynamic drone industry. By diligently tracking the depreciation of their drone assets, companies can maintain a clear financial picture and make sound decisions for their operational future.