If you’ve ever applied for health insurance through the Marketplace, contributed to a Roth IRA, or wondered why you didn’t qualify for certain tax credits, you likely encountered the term MAGI, or Modified Adjusted Gross Income.

While it sounds like complex tax jargon, understanding your MAGI is crucial because it acts as the “gatekeeper” for many of the most valuable financial benefits offered by the government.

1. Defining MAGI: The Basics

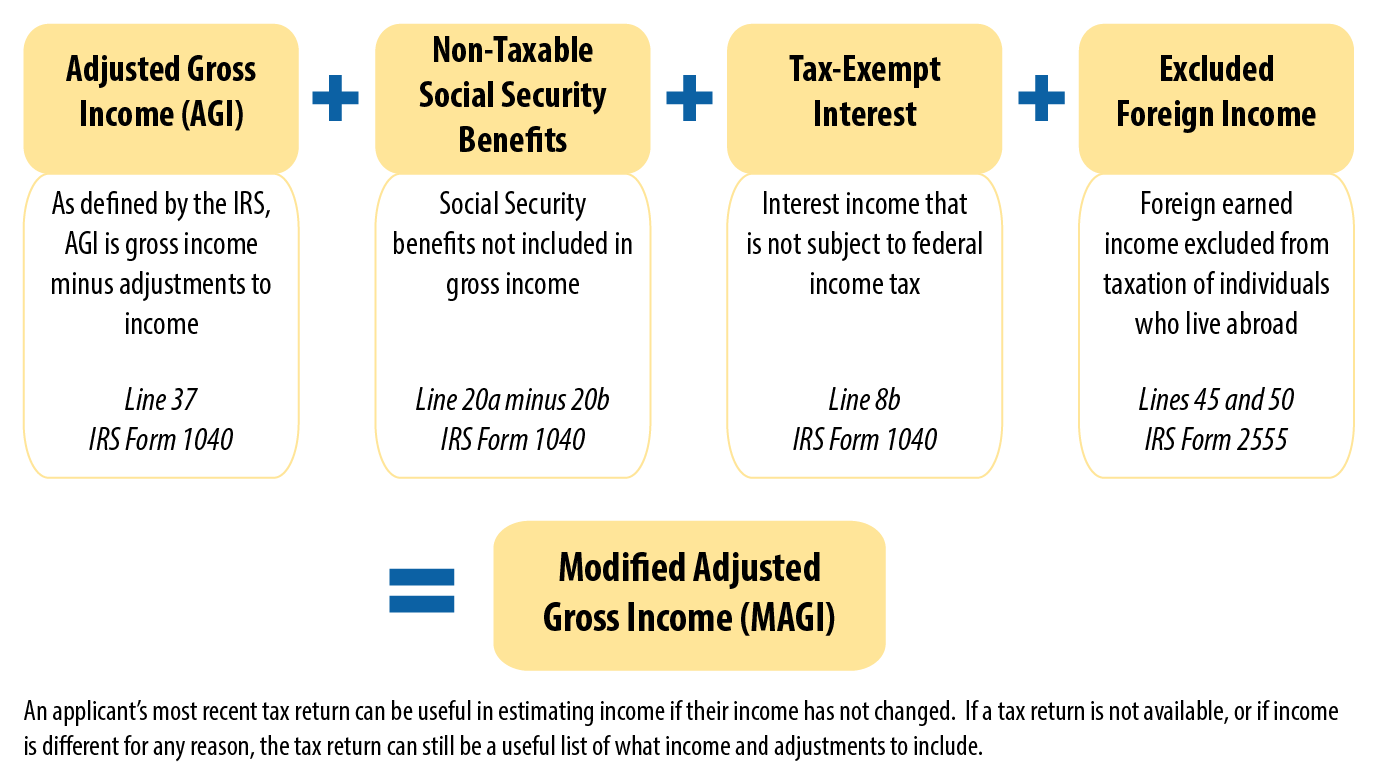

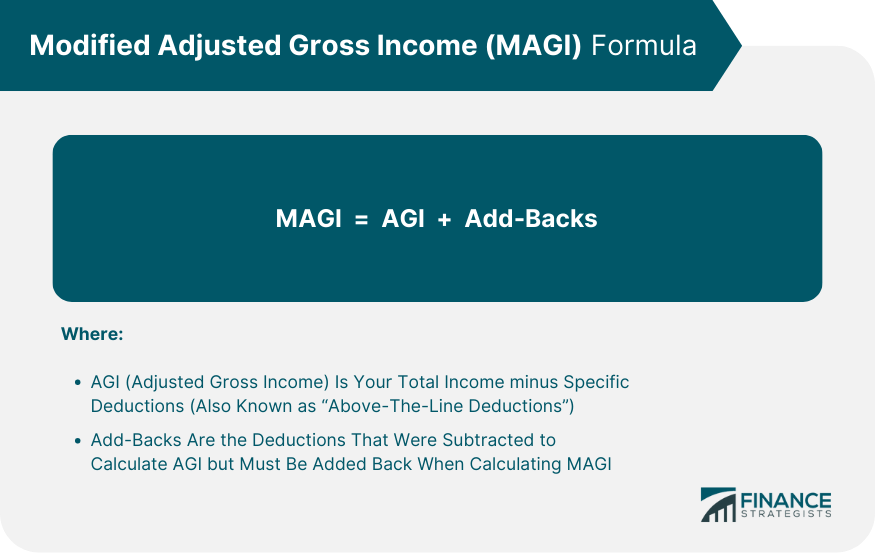

Modified Adjusted Gross Income (MAGI) is your Adjusted Gross Income (AGI) with certain deductions added back in.

The IRS uses MAGI to determine your eligibility for various tax deductions, credits, and government programs. For many taxpayers, MAGI is very close to—or even identical to—their AGI. However, if you have specific types of income or expenses (like foreign income or student loan interest), the two numbers will differ.

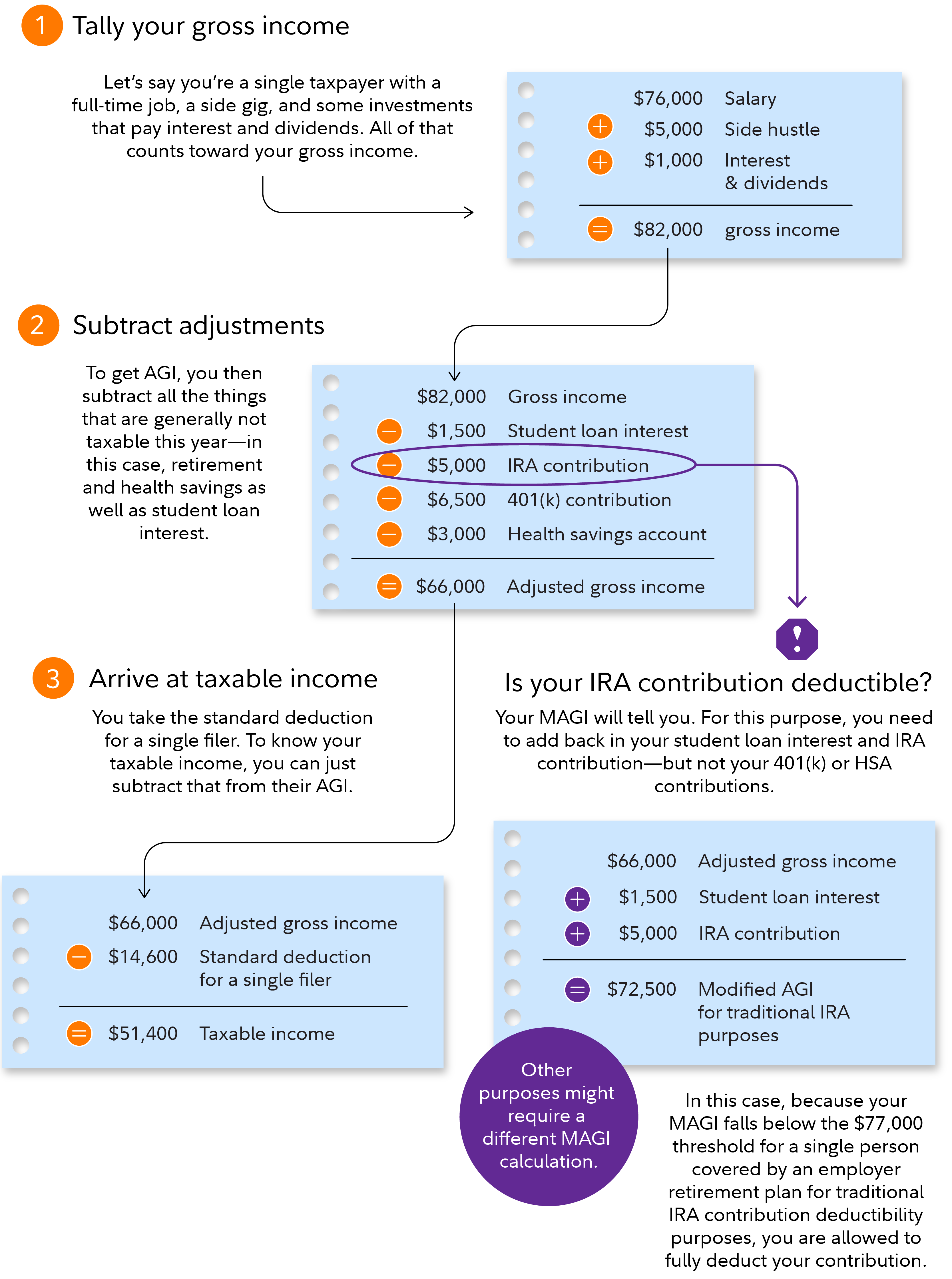

2. The Formula: From Gross Income to MAGI

To find your MAGI, you must follow a three-step process:

- Gross Income: The total of everything you earn (wages, dividends, capital gains, business income, etc.).

- Adjusted Gross Income (AGI): Gross income minus “above-the-line” deductions (such as HSA contributions, educator expenses, and student loan interest). This is found on Line 11 of Form 1040.

- Modified Adjusted Gross Income (MAGI): Take your AGI and add back specific deductions.

Common “Add-Backs” for MAGI:

Depending on what you are calculating MAGI for, you may need to add back:

- Student loan interest deductions.

- Half of the self-employment tax.

- Qualified tuition expenses.

- Passive income or losses.

- Excluded foreign income.

- Tax-exempt interest income (common for ACA eligibility).

- Rental losses.

3. Why Does MAGI Matter?

Your MAGI is the benchmark for several significant financial limits:

A. Retirement Account Contributions

- Roth IRA: If your MAGI exceeds certain thresholds, your ability to contribute to a Roth IRA is phased out or eliminated.

- Traditional IRA: Your MAGI determines if you can deduct your contributions if you (or your spouse) are covered by a retirement plan at work.

B. Health Insurance Subsidies (ACA)

If you buy health insurance through the Healthcare.gov Marketplace, your MAGI is used to determine if you qualify for Premium Tax Credits (subsidies) to lower your monthly costs.

C. Tax Credits and Deductions

MAGI determines if you qualify for:

- The Child Tax Credit.

- Education Credits (like the American Opportunity Tax Credit).

- The Adoption Credit.

4. MAGI vs. AGI: What’s the Difference?

It is easy to confuse the two, but here is the simple distinction:

- AGI is your income after certain deductions are taken.

- MAGI “undoes” some of those deductions to get a more comprehensive picture of your financial standing.

Note: For the vast majority of Americans who do not have foreign income or complex investment losses, AGI and MAGI are often the same number.

5. How to Find Your MAGI

There is no specific line on a standard tax return labeled “MAGI.” Because the “modifications” change depending on the credit or deduction you are applying for, you usually have to calculate it using a worksheet provided by the IRS (such as those found in Publication 590-A for IRAs).

Summary

Understanding your MAGI is essential for effective tax planning. If you are near the threshold for a Roth IRA contribution or a health insurance subsidy, small changes to your income—or increasing your pre-tax retirement contributions—could lower your MAGI enough to save you thousands of dollars.

Disclaimer: Tax laws change frequently. It is always recommended to consult with a tax professional or use certified tax software to calculate your specific MAGI for the current tax year.