Navigating the complexities of tax filing can often feel like deciphering an ancient riddle, especially when it comes to determining if you even need to file in the first place. The question of “what is the minimum income for filing taxes?” is a fundamental one, impacting millions of individuals and households each year. Understanding these thresholds is not just about avoiding potential penalties; it’s about ensuring you claim any eligible refunds and remain compliant with tax laws. This article aims to demystify these income requirements, providing a clear and comprehensive overview of who needs to file a federal income tax return in the United States.

The minimum income requirements for filing taxes are not static. They are influenced by a variety of factors, including your age, filing status, and the amount of gross income you received during the tax year. These guidelines are established by the Internal Revenue Service (IRS) and are typically updated annually to account for inflation. Therefore, it is crucial to consult the most recent tax year’s guidelines to ensure accuracy.

Understanding Gross Income Thresholds

At its core, the decision to file a tax return hinges on your gross income. Gross income encompasses all income you receive from any source that isn’t specifically excluded by law. This includes wages, salaries, tips, interest, dividends, capital gains, business income, and even certain benefits. However, the IRS sets specific thresholds below which you are generally not required to file. These thresholds vary significantly based on your filing status.

Filing Status and its Impact

Your filing status is a critical determinant in calculating your minimum income requirement. The most common filing statuses are:

- Single: This status applies if you are unmarried and do not qualify for any other filing status.

- Married Filing Separately: This status is for married individuals who choose to file their taxes individually, even if living together.

- Married Filing Jointly: This status is for married couples who choose to combine their income and deductions on a single tax return.

- Head of Household: This status is available to unmarried individuals who pay more than half the costs of keeping up a home for a qualifying child.

- Qualifying Widow(er): This status is for individuals who have a dependent child and meet certain other criteria, allowing them to file as married for two years after their spouse’s death.

Each of these statuses has a different standard deduction amount, which directly influences the gross income threshold for filing. For example, the threshold for a single filer will typically be lower than for a married couple filing jointly, as the latter benefits from a larger combined standard deduction.

Standard Deduction vs. Itemized Deductions

The concept of the standard deduction is central to understanding filing requirements. Most taxpayers are eligible to take either the standard deduction or to itemize their deductions. The standard deduction is a fixed dollar amount that reduces your taxable income. It is set by the IRS and varies based on your filing status and age. Itemized deductions, on the other hand, are specific expenses that you can deduct from your income, such as medical expenses, state and local taxes, home mortgage interest, and charitable contributions.

If your total gross income is less than your applicable standard deduction, you are generally not required to file a federal tax return. However, if you plan to itemize deductions, you must file a return even if your gross income is below the standard deduction threshold, provided your itemized deductions exceed the standard deduction amount. This is because itemizing can potentially reduce your taxable income below zero, leading to a refund.

Special Cases and Considerations

Beyond the general gross income thresholds, several special circumstances can trigger a filing requirement regardless of your income level. It’s important to be aware of these exceptions to ensure full compliance.

Self-Employment Income

If you are self-employed, the rules for filing can differ. Generally, if your net earnings from self-employment were $400 or more, you are required to file a tax return, even if your total gross income from all sources is below the standard filing threshold. This is because self-employment income is subject to self-employment taxes (Social Security and Medicare taxes), which must be reported and paid.

Receiving Advance Premium Tax Credits

If you received advance payments of the Premium Tax Credit (which helps pay for health insurance purchased through the Health Insurance Marketplace), you are required to file a federal tax return to reconcile these payments. Even if your income is below the usual filing threshold, you must file to claim the credit or repay any excess advance payments.

Other Filing Requirements

There are several other situations that necessitate filing a tax return, regardless of your income:

- Owing Special Taxes: If you owe any special taxes, such as household employment taxes or taxes related to retirement plans, you must file.

- Having a Health Savings Account (HSA): If you received a distribution from an HSA, you must file Form 8889, Health Savings Accounts (HSAs), with your tax return.

- Receiving Distributions from a Dependent’s Social Security: If you are claimed as a dependent on someone else’s tax return and received more than a certain amount of unearned income or a combination of earned and unearned income, you may need to file.

Current Tax Year Filing Thresholds (Example for Tax Year 2023)

To provide concrete examples, let’s look at the general income thresholds for the 2023 tax year (returns filed in 2024). These figures are for gross income and do not include any potential deductions. Remember, these are general guidelines, and your specific situation might vary.

Single Filers

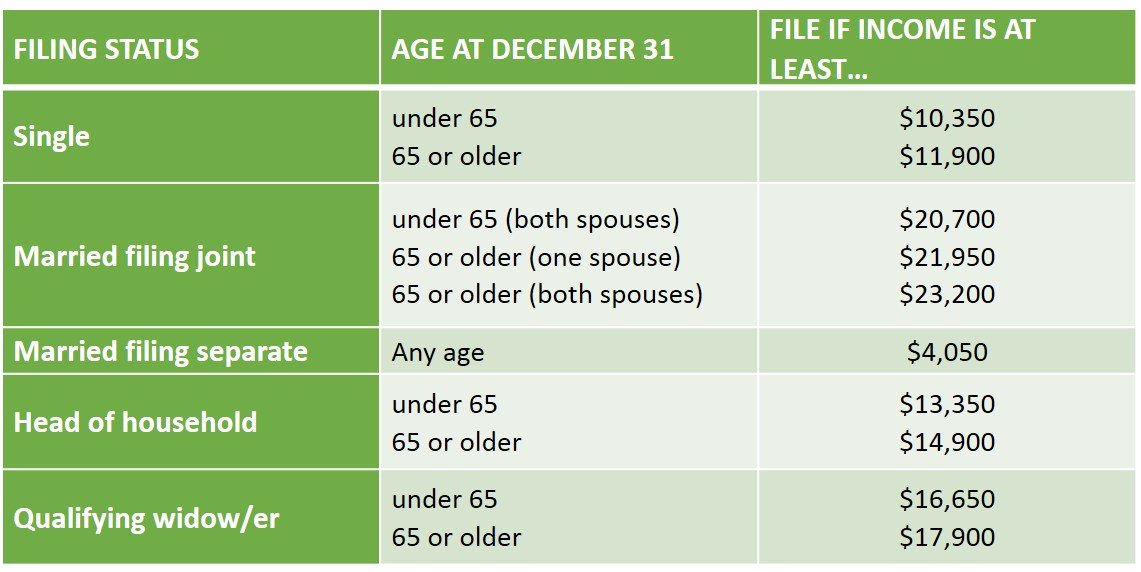

For the 2023 tax year, an individual filing as Single is generally required to file if their gross income was at least $13,850. This threshold increases for those who are 65 or older.

Married Filing Separately

Married individuals filing Separately have a very low filing threshold: $5. This means that if you are married and choose to file separately, you will likely need to file a return even with minimal income, unless you have no tax liability and no reason to claim a refund.

Married Filing Jointly

For married couples filing Jointly, the gross income threshold is significantly higher. For the 2023 tax year, married couples filing jointly are generally required to file if their gross income was at least $27,700. This threshold increases for couples where one or both spouses are age 65 or older.

Head of Household

For those filing as Head of Household, the gross income threshold for the 2023 tax year is $20,800. This threshold also increases if the taxpayer is 65 or older.

Qualifying Widow(er)

Similar to married couples filing jointly, qualifying widows and widowers have a higher filing threshold. For the 2023 tax year, the gross income threshold is $27,700, with an additional amount if the taxpayer is 65 or older.

Why Filing is Beneficial, Even When Not Required

While the IRS sets minimum income thresholds for filing, choosing to file a tax return can often be beneficial, even if your income falls below these requirements. Understanding these advantages can help you make an informed decision.

Claiming Tax Refunds

Perhaps the most common reason to file when not required is to claim a tax refund. If you had federal income tax withheld from your paychecks throughout the year, and your total tax liability for the year is less than the amount withheld, you are entitled to a refund of the difference. This can happen if you had a lower-than-expected income, experienced a change in employment, or qualify for certain tax credits.

For instance, if you worked only part of the year and your total income was below the filing threshold, but taxes were still withheld, filing a return is the only way to get that money back. Similarly, if you are eligible for refundable tax credits, such as the Earned Income Tax Credit (EITC) or the Additional Child Tax Credit, these credits can result in a refund even if you owe no tax. The EITC, in particular, is designed to help low-to-moderate-income individuals and families, and its benefits can be substantial.

Accessing Tax Credits

Several valuable tax credits can significantly reduce your tax liability or provide a refund. Some of these credits are “refundable,” meaning you can receive them as a refund even if you don’t owe any taxes. Common refundable credits include:

- Earned Income Tax Credit (EITC): As mentioned, this credit is for low-to-moderate-income individuals and families. The amount of the credit depends on your income, filing status, and the number of qualifying children you have.

- Additional Child Tax Credit (ACTC): This is a portion of the Child Tax Credit that can be refunded if it exceeds your tax liability.

- American Opportunity Tax Credit (AOTC): This credit is for eligible educational expenses for the first four years of higher education. A portion of this credit is refundable.

Even if you don’t owe taxes, filing allows you to claim these credits and potentially receive a payment from the government.

Establishing Eligibility for Future Benefits

Filing tax returns, even with low income, can serve as a valuable record of your earnings and tax payments. This documentation can be crucial for establishing eligibility for various government programs and benefits in the future. For example:

- Social Security Benefits: Your earnings history, as reported on your tax returns, is used to calculate your eligibility for Social Security retirement, disability, and survivor benefits.

- Student Loans: Lenders and financial institutions may require proof of income from tax returns when you apply for student loans or other forms of credit.

- Housing Assistance: Some housing assistance programs require proof of income through filed tax returns.

By consistently filing, you build a solid financial history that can open doors to future opportunities and support systems.

Conclusion: Stay Informed and File Accordingly

The question of “what is the minimum income for filing taxes?” is multifaceted, with answers that depend on your individual circumstances. While the IRS provides clear gross income thresholds, it’s essential to remember that these are general guidelines. Self-employment income, special taxes owed, advance premium tax credit payments, and the potential to claim valuable refunds and credits can all influence your decision to file.

Staying informed about the latest IRS guidelines for the relevant tax year is paramount. The thresholds are subject to change, and it’s your responsibility to ensure compliance. Consult the official IRS website or a qualified tax professional if you have any doubts or complex situations. Ultimately, understanding these requirements empowers you to navigate the tax system effectively, claim the benefits you’re entitled to, and maintain peace of mind. Even if you are not legally required to file, carefully considering the potential benefits of filing can lead to financial advantages and a more secure future.