In the complex landscape of real estate financing, understanding key financial metrics is paramount for both borrowers and lenders. Among these, the Loan-to-Value (LTV) ratio stands out as a fundamental indicator that profoundly influences mortgage approval, interest rates, and associated costs. It’s a simple yet powerful calculation that encapsulates the risk profile of a mortgage transaction. For anyone navigating the process of buying a home, refinancing an existing mortgage, or even considering a home equity loan, grasping the concept and implications of LTV is not just beneficial – it’s essential for making informed financial decisions.

The LTV ratio is a straightforward comparison between the amount of money being borrowed and the appraised value of the property. It acts as a yardstick for lenders, helping them assess the potential financial exposure they undertake with each mortgage. A lower LTV generally signifies a lower risk for the lender, as the borrower has a greater stake in the property, and there’s more equity to absorb potential market fluctuations or default scenarios. Conversely, a higher LTV indicates a greater proportion of the property’s value is financed by the loan, increasing the lender’s risk and potentially leading to higher costs for the borrower. This article will delve into the intricacies of LTV, exploring its calculation, significance, and impact on various aspects of the mortgage process.

Understanding the Core Calculation of LTV

At its heart, the Loan-to-Value ratio is a simple mathematical formula, yet its implications are far-reaching within the mortgage industry. Lenders use this ratio as a primary tool for assessing risk and determining the terms of a loan. Understanding how it’s calculated is the first step to deciphering its importance.

The Formula and Its Components

The calculation of the Loan-to-Value ratio is remarkably straightforward. It is derived by dividing the total amount of the mortgage loan by the appraised value of the property, expressed as a percentage.

The formula is as follows:

LTV = (Loan Amount / Appraised Property Value) * 100

Let’s break down the two key components:

- Loan Amount: This is the total sum of money the borrower is requesting from the lender for the mortgage. It typically includes the principal amount needed to purchase the property. In some cases, it might also encompass certain closing costs or fees that are rolled into the loan, though this practice can significantly increase the LTV.

- Appraised Property Value: This is the estimated market value of the property, determined by a professional appraiser. The appraisal is a crucial step in the mortgage process, as it provides an objective assessment of what the property is worth. Lenders rely on this valuation to ensure that the collateral backing the loan is sufficient. It’s important to note that the appraised value can sometimes differ from the agreed-upon purchase price. In such instances, lenders typically use the lower of the two figures (appraised value or purchase price) for LTV calculation purposes to err on the side of caution.

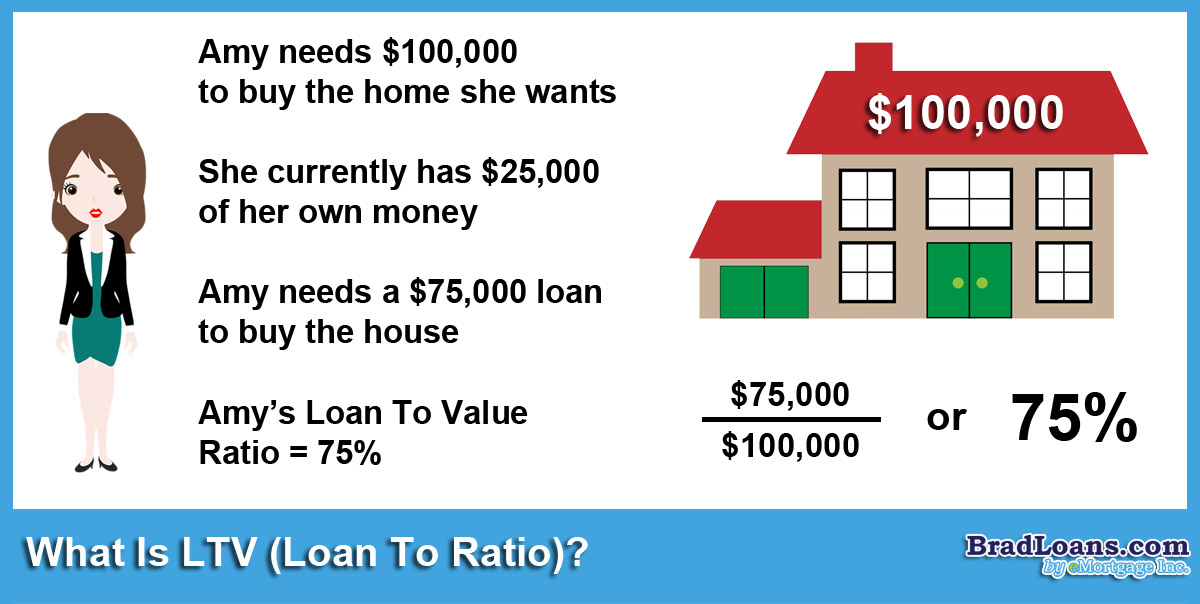

For example, if a borrower is purchasing a home appraised at $300,000 and is seeking a mortgage of $240,000, the LTV would be calculated as:

LTV = ($240,000 / $300,000) * 100 = 80%

This 80% LTV signifies that the borrower is financing 80% of the property’s value, and their down payment or existing equity represents the remaining 20%.

The Significance of the Appraised Value

The appraisal process itself is a critical determinant of the LTV. Appraisers consider a multitude of factors when determining a property’s value, including:

- Comparable Sales (Comps): The prices of recently sold similar properties in the same neighborhood.

- Property Condition: The age, maintenance, and any recent renovations or necessary repairs.

- Location: Proximity to amenities, schools, and overall desirability of the area.

- Square Footage and Features: The size of the home, number of bedrooms and bathrooms, lot size, and unique features.

- Market Trends: Current supply and demand dynamics in the local real estate market.

The appraisal aims to provide a realistic market value, which is essential for the lender to gauge the security of their investment. If the appraised value comes in lower than expected, it can have a direct impact on the LTV, potentially requiring the borrower to either increase their down payment or accept less favorable loan terms.

The Impact of LTV on Mortgage Approval and Terms

The Loan-to-Value ratio is not merely a calculation; it’s a gateway that significantly influences whether a mortgage is approved and, if so, under what conditions. Lenders use LTV as a primary risk assessment tool, and a lower ratio generally translates into more favorable outcomes for the borrower.

LTV Thresholds and Lender Risk

Lenders categorize mortgage applications based on their LTV. These thresholds are critical because they directly correlate with the perceived risk of default.

- High LTV (e.g., 80% and above): Mortgages with a high LTV are considered riskier by lenders. This is because the borrower has a smaller financial stake in the property. In the event of a foreclosure or a significant downturn in the housing market, the lender has less equity to recover their investment. Consequently, high LTV loans often come with stricter qualification requirements and may necessitate private mortgage insurance (PMI).

- Moderate LTV (e.g., 60% to 80%): This range represents a more balanced risk profile. Lenders are generally more comfortable with these LTVs, and the terms offered might be more competitive than those for high LTV loans.

- Low LTV (e.g., below 60%): Loans with a low LTV are viewed as the least risky. The borrower has a substantial equity stake in the property, providing a strong incentive to uphold their loan obligations. These loans typically offer the most favorable interest rates and loan terms.

The Role of Private Mortgage Insurance (PMI)

One of the most significant consequences of a high LTV is the requirement for Private Mortgage Insurance (PMI). PMI is an insurance policy that protects the lender if the borrower defaults on the loan. It is typically required when the borrower’s down payment is less than 20% of the home’s purchase price, resulting in an LTV of 80% or higher.

- Cost to the Borrower: PMI is an additional monthly expense for the homeowner. The cost of PMI varies based on the loan amount, the borrower’s credit score, and the LTV, but it can add a considerable amount to the monthly mortgage payment.

- Cancellation of PMI: Fortunately, PMI is not a permanent fixture. Homeowners can typically request to have PMI removed once their LTV falls to 80% of the original appraised value. Furthermore, by law, PMI must automatically be canceled when the LTV reaches 78% of the original appraised value, provided the loan is current on payments.

Interest Rates and Loan Terms

Beyond PMI, LTV directly impacts the interest rates offered by lenders.

- Higher LTV = Higher Interest Rates: Because high LTV loans carry greater risk, lenders often compensate for this by charging higher interest rates. This means borrowers with a lower down payment will pay more in interest over the life of the loan.

- Lower LTV = Lower Interest Rates: Conversely, borrowers who can achieve a lower LTV by making a larger down payment often qualify for lower interest rates. This can lead to substantial savings over the loan term, making the overall cost of homeownership significantly less.

The LTV also influences other loan terms, such as the types of loan programs available. Some government-backed loan programs (like FHA loans) allow for higher LTVs, making homeownership more accessible, but often come with their own forms of mortgage insurance that may be structured differently from conventional PMI.

Strategies to Optimize Your LTV

Understanding the impact of LTV empowers prospective and current homeowners to take proactive steps to improve their financial standing and secure more favorable mortgage terms. By strategically managing your down payment, creditworthiness, and loan options, you can work towards achieving a lower LTV.

Maximizing Your Down Payment

The most direct way to reduce your LTV is by increasing your down payment. A larger down payment means a smaller loan amount relative to the property’s value.

- Saving Strategically: This involves disciplined saving, budgeting, and potentially exploring different savings vehicles. Prioritizing saving for a down payment can lead to significant long-term financial benefits through reduced interest payments and avoidance of PMI.

- Gift Funds: Many lenders allow borrowers to use gift funds from family members for down payments. It’s crucial to ensure these gifts are properly documented according to lender guidelines to avoid complications.

- Down Payment Assistance Programs: Various state and local government agencies, as well as non-profit organizations, offer down payment assistance programs. These programs can provide grants or low-interest loans to help eligible borrowers cover a portion of their down payment, thereby reducing the LTV.

Improving Creditworthiness

While not directly part of the LTV calculation, your credit score plays a crucial role in how lenders assess risk and determine loan terms, especially when LTV is a factor.

- Credit Score Impact: A higher credit score signals to lenders that you are a responsible borrower, making them more willing to offer better interest rates and more flexible terms, even with a slightly higher LTV. Conversely, a low credit score can necessitate a higher down payment to compensate for the perceived risk.

- Steps to Improve Credit: This includes paying bills on time, reducing existing debt, avoiding opening new credit accounts unnecessarily before applying for a mortgage, and checking your credit reports for errors and disputing them.

Exploring Different Loan Programs

Not all mortgage products are created equal, and some are designed to accommodate different LTV scenarios.

- Conventional Loans: Typically require a 20% down payment to avoid PMI. However, some conventional loan programs allow for lower down payments, but will require PMI.

- FHA Loans: Insured by the Federal Housing Administration, these loans are designed for borrowers with lower credit scores and allow for down payments as low as 3.5% (resulting in a high LTV). However, they require an upfront mortgage insurance premium and annual mortgage insurance premiums for the life of the loan in most cases.

- VA Loans: Guaranteed by the Department of Veterans Affairs, these loans are available to eligible veterans and service members. A significant benefit is that VA loans often allow for 0% down payment, meaning an LTV of 100%, and do not require private mortgage insurance.

- USDA Loans: For eligible rural and suburban areas, these loans offer 0% down payment options for qualified borrowers. Similar to FHA loans, they have their own guarantee fees.

By understanding these strategies and how they interact with the LTV ratio, borrowers can approach the mortgage process with greater confidence and work towards achieving the most advantageous loan terms for their financial situation.

Beyond the Purchase: LTV in Refinancing and Home Equity

The significance of the Loan-to-Value ratio extends beyond the initial home purchase. It plays a critical role in subsequent financial transactions involving a property, such as refinancing an existing mortgage or tapping into home equity. Understanding LTV in these contexts allows homeowners to make informed decisions about optimizing their financial leverage and managing their property’s value.

Refinancing Your Mortgage

Refinancing involves replacing an existing mortgage with a new one, often to secure a lower interest rate, change the loan term, or convert from an adjustable-rate mortgage (ARM) to a fixed-rate mortgage. The LTV of your property at the time of refinancing is a primary determinant of your eligibility and the terms you will receive.

- Lower LTV for Better Rates: If your home’s value has increased since you purchased it, or if you’ve paid down a significant portion of your mortgage principal, your LTV will have decreased. A lower LTV during refinancing generally allows you to qualify for better interest rates and more favorable loan terms, as you represent less risk to the new lender.

- Higher LTV Challenges: Conversely, if your home’s value has depreciated or if you haven’t made substantial principal payments, your LTV might be higher than when you initially took out the loan. This can make it more challenging to get approved for a refinance, especially if the LTV exceeds 80%, potentially requiring PMI on the new loan or leading to higher interest rates.

- Cash-Out Refinance: Homeowners may opt for a cash-out refinance to borrow more than they currently owe on their mortgage and receive the difference in cash. This inherently increases the LTV. Lenders will assess the new, higher LTV to determine risk and set the terms for the cash-out portion of the loan. Typically, lenders will cap the combined loan-to-value (CLTV) for cash-out refinances, often around 80% to 90%, depending on the lender and borrower’s creditworthiness.

Accessing Home Equity

Home equity represents the portion of your home’s value that you actually own, free from debt. Homeowners can leverage this equity through various financial products, and the LTV is a crucial factor in determining how much equity you can borrow against.

- Home Equity Loans: These are typically second mortgages taken out against the equity in your home. They provide a lump sum of cash, repaid with fixed monthly payments over a set period. Lenders will consider the combined loan-to-value (CLTV) – the sum of your primary mortgage balance and the new home equity loan, divided by the home’s value. Most lenders will allow a CLTV of up to 80% or 85%, meaning your existing mortgage and the new home equity loan cannot exceed this percentage of your home’s appraised value.

- Home Equity Lines of Credit (HELOCs): A HELOC functions more like a credit card, allowing you to borrow funds up to a certain limit during a “draw period.” You make interest-only payments during this phase, and then a repayment period begins where you pay back the principal and interest. Similar to home equity loans, HELOCs are also subject to CLTV limits, usually capped around 80% to 85%. A higher LTV will restrict the amount of credit you can access through a HELOC.

In essence, LTV acts as a gatekeeper for accessing your home’s equity. A lower LTV signifies more available equity for borrowing, while a higher LTV limits your borrowing capacity. Understanding and managing your LTV is therefore not just about purchasing a home, but also about intelligently leveraging its value throughout your ownership journey.