In the dynamic and rapidly evolving world of uncrewed aerial vehicles (UAVs), commonly known as drones, operators — particularly those engaged in commercial activities — navigate a complex landscape of regulations, operational risks, and financial considerations. Among these critical elements, insurance stands as a fundamental safeguard. Within the realm of drone insurance, a specific document often arises during the initial phases of securing coverage: the insurance binder. Far from a mere formality, an insurance binder serves as a temporary, yet legally binding, proof of coverage that bridges the gap between applying for a drone insurance policy and its official issuance. For drone professionals and businesses, understanding the nuances of an insurance binder is not just beneficial but often essential for seamless operations, compliance, and risk management.

The Essential Role of Insurance for Drone Operators

The deployment of drones, whether for aerial cinematography, mapping, inspection, surveying, or delivery services, inherently carries a spectrum of risks. These can range from property damage caused by an unexpected crash, bodily injury to third parties, data privacy breaches during data collection, or even liability stemming from failed missions or faulty data. Consequently, comprehensive insurance coverage has become a cornerstone of responsible and professional drone operation. Without adequate protection, a single incident could lead to significant financial ruin for an individual operator or an entire enterprise.

Drone insurance policies are specialized, often encompassing several critical components: hull coverage (for damage to the drone itself), liability coverage (for damage or injury to third parties), payload coverage (for sensitive cameras, sensors, or other equipment carried by the drone), and sometimes even privacy and cyber liability. The process of underwriting and issuing such a specialized policy can take time, involving detailed risk assessments, equipment valuations, and operational profiling. During this interim period, an operator might need to demonstrate proof of insurance to meet contractual obligations, satisfy regulatory bodies, or finalize financing for new equipment. This is precisely where the insurance binder proves its indispensable value.

Why a Binder is Crucial for Drone Acquisition and Operation

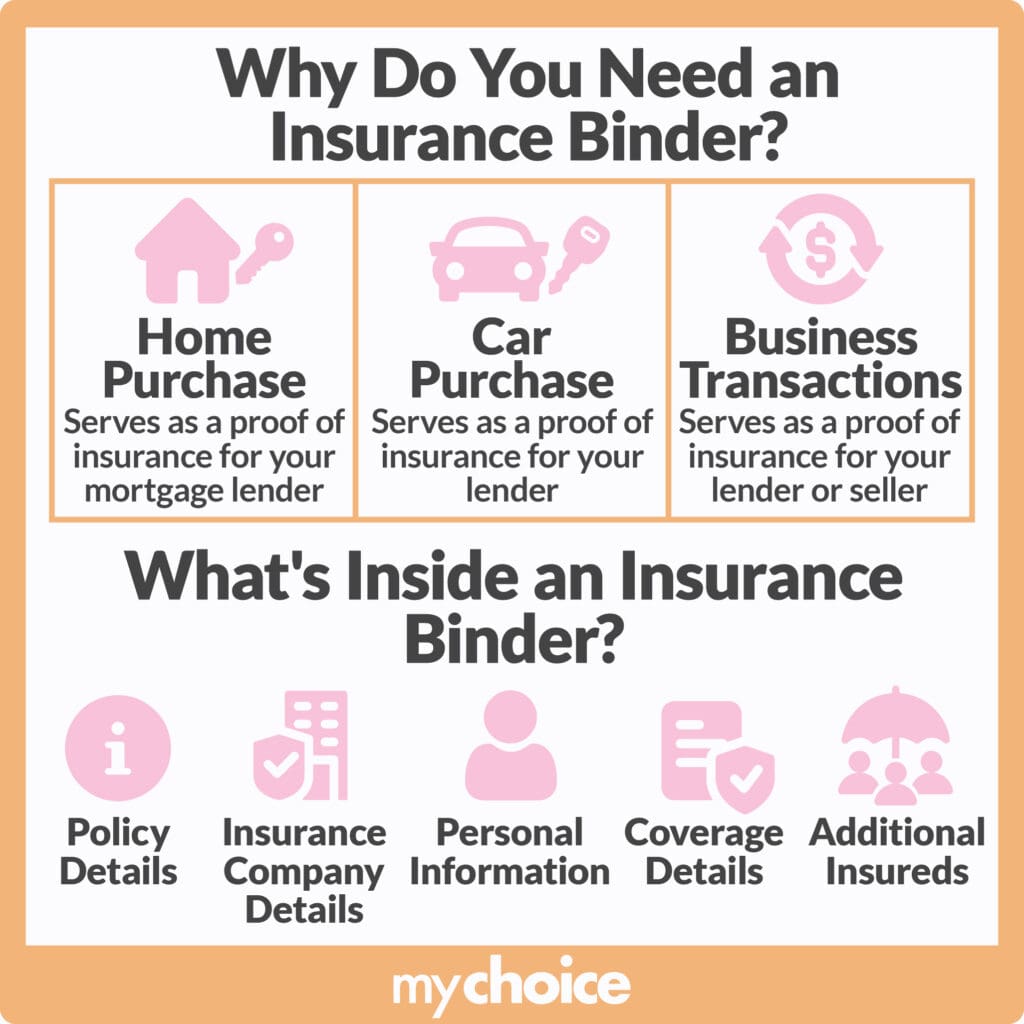

Imagine a scenario where a drone service provider lands a lucrative contract to perform infrastructure inspections using a newly acquired, high-value industrial drone. The client, understanding the inherent risks, mandates proof of liability insurance before any flight operations commence. Simultaneously, the provider is still in the process of finalizing a comprehensive annual policy for their entire fleet. Without an immediate solution, the contract could be jeopardized, or the new drone might sit idle, incurring costs without generating revenue.

This is a prime example of where an insurance binder becomes a critical enabler. It provides instant, verifiable confirmation that an insurance policy is indeed in effect, albeit temporarily, while the formal policy documents are being prepared. This temporary coverage ensures that the drone operator can commence operations, take delivery of new equipment, or satisfy lender requirements without delay, bridging the gap between application and policy issuance. For drone businesses, it represents continuity and agility, allowing them to seize opportunities without being hampered by administrative timelines.

Deconstructing the Drone Insurance Binder

An insurance binder, in essence, is a temporary contract of insurance. It is a concise document issued by an insurer or their authorized agent that confirms that insurance coverage has been put into effect. While temporary, it carries the same legal weight as a full policy during its active period, offering the specified protections under the agreed-upon terms and conditions. For drone operators, this means the drone(s) and associated liabilities are covered as if the full policy were already in hand.

Key Components and Coverage Types

A typical drone insurance binder will include several vital pieces of information, all tailored to the specific context of drone operations:

- Insured’s Name: The individual drone operator or the legal entity/company being covered.

- Policy Number (Temporary/Pending): While a final policy number may not be assigned, the binder will often reference a pending application or a temporary identifier.

- Effective Date and Expiration Date: Crucially, the binder will state when the temporary coverage begins and, just as importantly, when it ends. This period is typically short, ranging from 30 to 90 days, designed to allow sufficient time for the full policy to be issued.

- Type of Coverage: This specifies the nature of the insurance. For drone binders, this will detail whether it’s hull coverage (for physical damage to the drone itself), general liability (for third-party injury/damage), payload coverage, or a combination. The limits of coverage (e.g., $1 million liability, $50,000 hull coverage) will also be clearly stated.

- Description of Insured Property/Operations: For drones, this will include details about the specific UAV(s) being covered (make, model, serial number) and/or the nature of the operations (e.g., commercial aerial photography, industrial inspection, agricultural spraying).

- Premium Information: While the binder itself doesn’t typically serve as a bill, it confirms that arrangements for premium payment have been made, or that the first installment has been received.

- Binder Number: A unique identifier for the binder itself.

- Insurer and Agent Information: Details of the insurance company providing the coverage and the agent/broker who issued the binder.

- Special Conditions/Endorsements: Any specific terms, exclusions, or additional coverages pertinent to drone operations, such as coverage for night flights, specific altitudes, or operations in restricted airspace (if applicable and agreed upon).

The specific coverages bound will mirror those requested in the full policy application. For instance, if a drone company is applying for a policy that includes $2 million in commercial general liability and $100,000 in hull coverage for their fleet of DJI Matrice drones, the binder will reflect these exact coverage types and limits.

Understanding the Binder’s Validity and Limitations

While a powerful tool, it’s crucial for drone operators to understand that a binder is temporary. Its specified expiration date is firm, and coverage will cease unless a formal policy is issued and accepted beforehand. It’s not a long-term solution but a bridge. The purpose of this limited validity is to give the insurance company time to complete its underwriting process, issue the final policy documents, and collect any outstanding premium payments.

If a full policy is not issued by the binder’s expiration date, drone operations must cease or alternative temporary coverage must be secured to avoid operating uninsured. This highlights the importance of proactive communication with the insurance broker or carrier to ensure the full policy is finalized in a timely manner. Delays can occur due to incomplete application information, outstanding payments, or complex underwriting requirements specific to highly specialized drone operations.

Practical Scenarios for Drone Insurance Binders

The utility of an insurance binder for drone professionals extends across several common operational and commercial situations, providing immediate peace of mind and operational agility.

Commercial Operations and Client Requirements

One of the most frequent uses of an insurance binder is to satisfy client demands. Many organizations hiring drone services—whether for surveying construction sites, capturing real estate footage, or performing critical infrastructure inspections—will require their contractors to provide proof of adequate insurance coverage before any work can begin. This is to protect themselves from liability in case of an incident involving the drone operator. An insurance binder, presented as official proof of coverage, allows the drone company to sign contracts, mobilize equipment, and commence operations immediately, preventing delays and demonstrating professionalism. This is particularly vital in competitive markets where timely execution can be a differentiator.

Financing and Leasing Drone Equipment

High-end commercial drones and their associated payloads (e.g., LiDAR scanners, advanced thermal cameras) represent significant capital investments. When a drone company purchases new equipment through financing or leases it, the lender or lessor will almost invariably require proof of hull coverage to protect their asset. This ensures that in the event of damage or total loss, their investment is secured. An insurance binder quickly fulfills this requirement, enabling the financing or leasing agreement to close without waiting for the full policy documents to be processed. This is essential for drone businesses looking to expand their capabilities or upgrade their fleet without interruptions.

Expediting Regulatory Compliance

In some jurisdictions or for specific types of drone operations (e.g., flights over populated areas, operations under waivers from aviation authorities), regulatory bodies may require operators to demonstrate valid insurance coverage as part of the permitting or authorization process. While full policy documents are eventually needed, an insurance binder can serve as initial proof, allowing the application process to move forward. This ensures that drone businesses can maintain compliance and avoid penalties or delays in obtaining necessary operational clearances.

Beyond the Binder: Transitioning to a Full Drone Policy

While indispensable for its temporary coverage, the ultimate goal for any drone operator using a binder is to transition to a permanent, comprehensive drone insurance policy. This transition involves reviewing the final policy documents, ensuring all terms and conditions align with the binder’s promised coverage and the operator’s needs, and making any outstanding premium payments.

The full policy will provide detailed declarations, definitions, exclusions, and conditions that govern the insurance agreement for its entire term, typically one year. It’s imperative for drone operators to thoroughly read and understand their full policy. This includes knowing their responsibilities, such as maintaining flight logs, adhering to safety protocols, and promptly reporting incidents, as these often have implications for claims.

In conclusion, an insurance binder for drone operations is far more than a piece of paper; it’s a critical enabler of business continuity, client trust, and financial security in a fast-paced industry. It provides the immediate assurance of protection, allowing drone professionals to acquire equipment, secure contracts, and operate legally while the comprehensive details of their long-term coverage are finalized. Understanding its purpose, components, and limitations is paramount for any responsible and forward-thinking drone operator.