An Inherited IRA, often referred to as a Beneficiary IRA or a Stretch IRA (though the latter term’s implications have evolved), is a special type of Individual Retirement Account that is passed to a beneficiary after the original owner’s death. This financial instrument plays a crucial role in wealth transfer and can significantly impact a beneficiary’s financial planning, tax liabilities, and long-term savings strategies. Understanding the intricacies of an Inherited IRA is paramount, as the rules governing its distributions, taxation, and management have undergone significant changes, particularly with the passage of the SECURE Act (Setting Every Community Up for Retirement Enhancement Act) in late 2019 and its subsequent updates.

The Core Concept of an Inherited IRA

At its heart, an Inherited IRA allows a beneficiary to receive the remaining assets from the deceased owner’s IRA. However, unlike a standard IRA where an individual contributes and manages their own retirement savings, an Inherited IRA operates under a distinct set of regulations designed to dictate how and when these assets must be withdrawn. The primary objective is to manage the tax deferral benefits that retirement accounts offer, ensuring they are used for their intended purpose—retirement—or that taxes are collected within a reasonable timeframe when transferred to a non-spouse beneficiary.

The nature of an Inherited IRA depends heavily on the relationship between the deceased original owner and the beneficiary. This relationship dictates the distribution options available, which in turn profoundly impacts tax planning and wealth management decisions. Beneficiaries must act promptly to establish the Inherited IRA correctly, as errors can lead to immediate and substantial tax consequences. The account must be titled specifically as an “Inherited IRA” or “Beneficiary IRA,” distinguishing it from a personal IRA to avoid commingling funds and triggering incorrect tax treatments.

Different Types of Beneficiaries

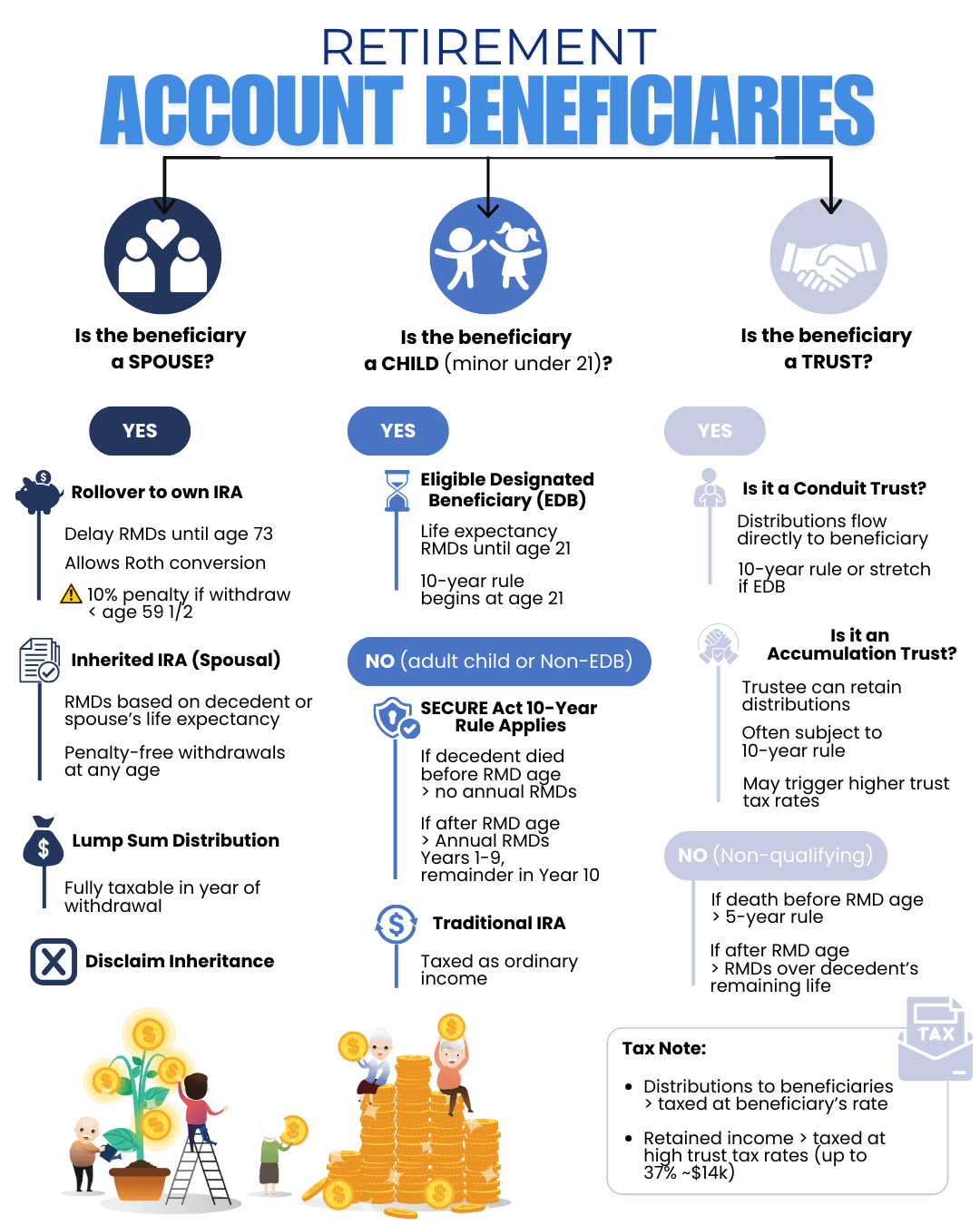

The rules surrounding an Inherited IRA are not uniform; they vary significantly based on the beneficiary’s status. Broadly, beneficiaries are categorized as follows:

-

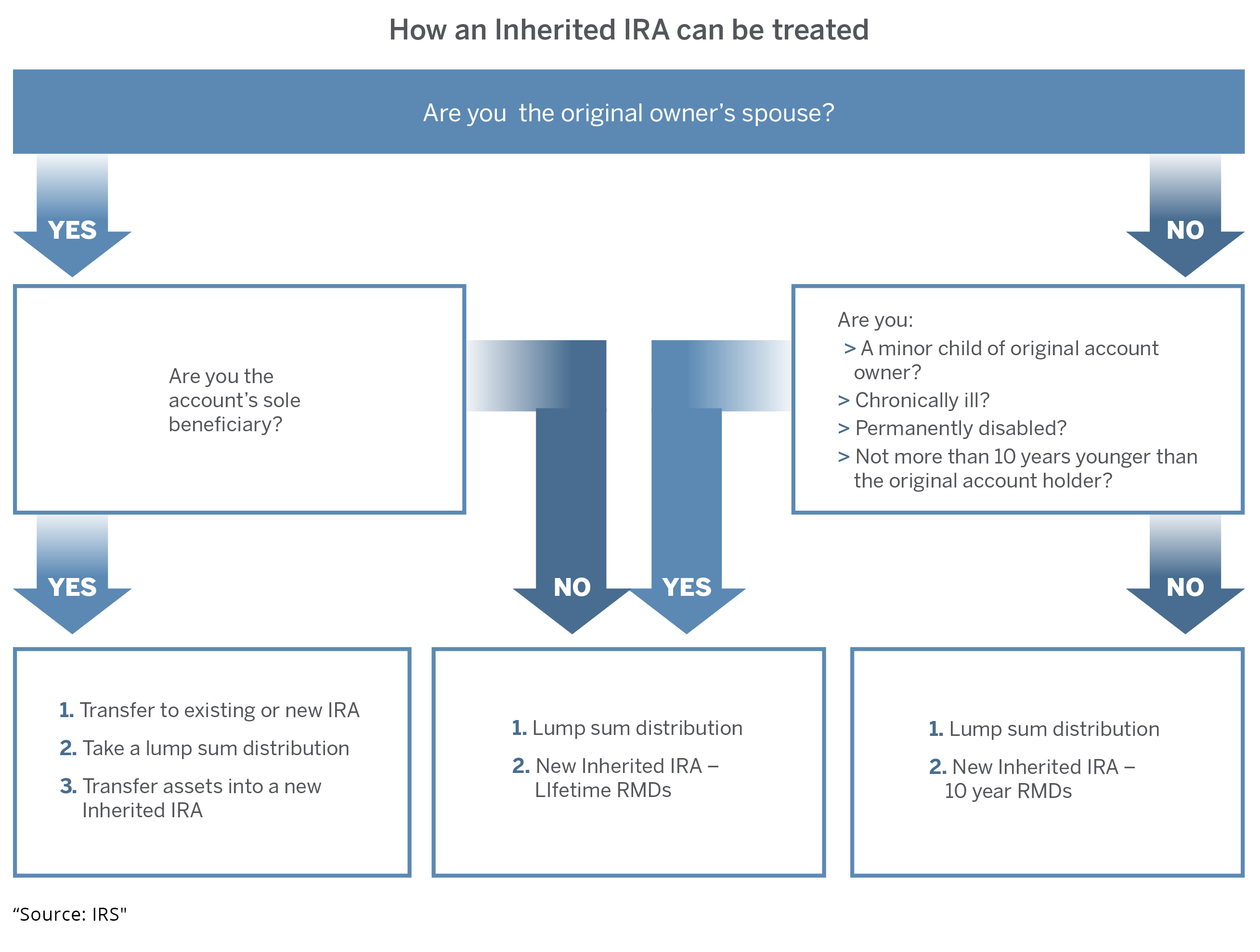

Spousal Beneficiaries: A surviving spouse typically has the most flexibility. They can choose to treat the Inherited IRA as their own, rolling it into an existing IRA or transferring it to a new one established in their name. This allows the spouse to delay distributions until they reach age 73 (Required Beginning Date for RMDs), or, if the deceased had already started RMDs, they can continue with the original RMD schedule. Spouses can also elect to be treated as a non-spouse beneficiary under the 10-year rule, which might be beneficial in specific scenarios, though less common. This spousal flexibility is a significant planning advantage, allowing for continued tax deferral and control over the funds.

-

Eligible Designated Beneficiaries (EDBs): This category was introduced with the SECURE Act to distinguish certain non-spouse beneficiaries who retain some of the “stretch” provisions that were largely eliminated for most others. EDBs include:

- The deceased’s minor children (until they reach the age of majority, after which the 10-year rule applies).

- Disabled individuals (as defined by the IRS).

- Chronically ill individuals (as defined by the IRS).

- Individuals who are not more than 10 years younger than the deceased IRA owner.

- These beneficiaries generally still have the option to “stretch” distributions over their own life expectancy, albeit with specific conditions. This provides a valuable, extended period of tax deferral.

-

Non-Eligible Designated Beneficiaries: This is the most common category for non-spouse beneficiaries, including adult children, grandchildren, siblings, or other non-EDBs. For these beneficiaries, the traditional “stretch” option has largely been replaced by the “10-year rule.” This significantly accelerates the distribution timeline and requires careful planning.

-

Non-Designated Beneficiaries (e.g., Estates or Trusts): If an estate or a trust is named as the beneficiary, or if there is no named beneficiary, the rules become even more complex and often less favorable. Depending on whether the original owner died before or after their Required Beginning Date (RBD), the assets may need to be fully distributed within five years or over the original owner’s remaining life expectancy. Trusts named as beneficiaries can sometimes qualify for “look-through” provisions, allowing the trust beneficiaries to be treated as designated beneficiaries, but this requires specific trust language and careful legal structuring.

Navigating Distribution Rules and Options

The most critical aspect of managing an Inherited IRA revolves around its distribution rules. Incorrectly handling distributions can lead to significant tax penalties, often as high as 50% of the amount that should have been withdrawn.

The 10-Year Rule

For most non-spouse, non-eligible designated beneficiaries, the SECURE Act introduced the 10-year rule. This rule mandates that the entire Inherited IRA balance must be fully distributed by the end of the 10th calendar year following the year of the original owner’s death. Crucially, for IRA owners who died after December 31, 2019, and who were already taking Required Minimum Distributions (RMDs), the IRS clarified in 2022 that beneficiaries subject to the 10-year rule must also take annual RMDs during years 1-9 before fully liquidating the account by year 10. If the original owner died before their RMDs began, the 10-year rule generally allows the beneficiary to withdraw funds at any time during the 10-year period, with the entire balance liquidated by the end of year 10. This flexibility allows some strategic tax planning, but the accelerated timeline means beneficiaries must be mindful of the immediate and future tax implications.

Exceptions to the 10-Year Rule (Eligible Designated Beneficiaries)

As mentioned, Eligible Designated Beneficiaries retain more flexibility. They can typically stretch distributions over their own life expectancy, similar to the pre-SECURE Act “stretch IRA” rules. This means they can take smaller annual distributions, allowing the remaining assets to continue growing tax-deferred for a longer period. However, for minor children who are EDBs, this “stretch” period generally ends once they reach the age of majority (typically 18 or 21, depending on state law), after which the remaining balance must be distributed within the subsequent 10 years. This hybrid approach adds another layer of complexity that requires meticulous tracking and planning.

Spousal Rollovers

The spouse’s ability to roll over the Inherited IRA into their own IRA is often the most advantageous option. This allows the spouse to become the new owner of the IRA, deferring distributions until their own Required Beginning Date (age 73). This not only maintains the tax-deferred growth but also grants the spouse full control over the investment decisions and beneficiary designations, effectively treating the inherited funds as if they were always their own. This flexibility is a cornerstone of estate planning for married couples, allowing for seamless transition and continued wealth accumulation.

Tax Implications and Planning

The tax implications of an Inherited IRA are significant and can vary based on the type of IRA (Traditional, Roth), the beneficiary’s distribution strategy, and their individual tax situation.

Income Tax Considerations

Distributions from a Traditional Inherited IRA are generally subject to ordinary income tax. Since the original contributions were often pre-tax, or tax-deductible, the growth and withdrawals are taxed at the beneficiary’s marginal income tax rate in the year they are received. This makes strategic timing of withdrawals crucial, especially under the 10-year rule, to avoid pushing the beneficiary into higher tax brackets. Conversely, qualified distributions from an Inherited Roth IRA are typically tax-free, as the original contributions were made with after-tax dollars. This tax-free status makes Inherited Roth IRAs highly desirable, especially for younger beneficiaries who can allow the funds to grow for a decade without future tax burdens.

Estate Tax Considerations

While the value of an IRA is included in the deceased owner’s taxable estate for federal estate tax purposes (if the estate’s value exceeds the federal exemption threshold), the Inherited IRA itself generally does not incur additional estate taxes when distributed to the beneficiary. The estate tax is levied on the deceased’s total estate before assets are distributed. However, beneficiaries should be aware of state-level inheritance or estate taxes, which can vary widely and may apply even if federal estate tax does not.

Leveraging Technology for Inherited IRA Management

In an era of increasing financial complexity and evolving regulations, technology plays a crucial role in simplifying the management and understanding of Inherited IRAs. The category of “Tech & Innovation” in finance extends beyond traditional banking to encompass tools that empower individuals to navigate intricate financial landscapes like inherited wealth.

Digital Platforms and Automation

Modern financial technology platforms offer significant advantages for beneficiaries of Inherited IRAs. Online brokerage accounts, for instance, provide intuitive dashboards to track account balances, monitor investment performance, and execute trades efficiently. These platforms often automate aspects of compliance, such as alerting beneficiaries to impending distribution deadlines under the 10-year rule or prompting them to consider their RMDs. Digital record-keeping ensures that all documentation related to the Inherited IRA, from beneficiary designation forms to distribution history, is securely stored and easily accessible. Furthermore, automated alerts and calendar integrations can prevent costly oversight, ensuring beneficiaries remain compliant with IRS regulations. The ability to manage these complex accounts from a smartphone or computer significantly enhances accessibility and control.

AI-Powered Financial Guidance

The innovation in artificial intelligence (AI) is beginning to transform how beneficiaries receive guidance on Inherited IRAs. AI-driven financial planning tools can analyze a beneficiary’s overall financial situation, including income, other assets, debts, and future goals, to recommend optimal distribution strategies. For example, an AI could model various withdrawal schedules under the 10-year rule, projecting the tax implications of each scenario and suggesting the most tax-efficient approach given current tax laws and the beneficiary’s income trajectory. While not replacing human financial advisors entirely, these AI tools act as powerful adjuncts, providing personalized insights, risk assessments, and proactive advice on navigating the nuances of Inherited IRAs. This innovative application of technology makes sophisticated financial planning more accessible, helping beneficiaries maximize the value of their inheritance while minimizing tax burdens.