Understanding the intricacies of sales tax is crucial for any business operating within or selling into Indiana. While the question “what is Indiana sales tax?” seems straightforward, its application involves a nuanced understanding of taxable goods and services, exemptions, filing requirements, and the specific economic nexus rules that have evolved over recent years. This article delves into the core components of Indiana sales tax, providing clarity for businesses navigating this complex landscape.

The Fundamentals of Indiana Sales Tax

Indiana imposes a state sales tax on the retail sale of tangible personal property and certain services. This tax is levied at the point of sale and is collected by the retailer, who then remits it to the Indiana Department of Revenue. The primary purpose of sales tax is to fund state and local government services, ranging from infrastructure development to public education and safety.

Taxable Goods and Services

At its core, Indiana sales tax applies to most tangible personal property sold at retail. This includes a wide array of items, from everyday consumer goods to specialized equipment. However, the definition of “tangible personal property” is key. It refers to items that can be touched, weighed, measured, or felt. This distinction is important because intangible property, such as software licenses that are delivered electronically and do not involve physical media, may be treated differently.

Beyond tangible goods, Indiana also taxes specific enumerated services. These typically include:

- Admissions to amusement, entertainment, or recreational events or facilities: This covers tickets to sporting events, concerts, theme parks, and other similar venues.

- Towing and repair services for motor vehicles: When you get your car fixed or towed, the labor and parts involved in certain repair services are generally subject to sales tax.

- Electrical contracting, plumbing, and window cleaning: Services performed by these trades within a building are often taxed.

- Business, employment, and management services: While broad, this category can encompass consulting, temporary staffing, and other advisory services.

- Linen and wardrobe rental services: Businesses that rent out linens or uniforms are typically required to collect sales tax on these rentals.

- Commercial printing: The production of printed materials for commercial purposes is generally taxable.

- Contracting for the construction or improvement of real property: While complex, sales tax may apply to certain aspects of construction projects, particularly when materials are consumed.

It is crucial to consult the Indiana Department of Revenue’s official guidance and tax publications for a comprehensive and up-to-date list of taxable services, as these can be subject to change and interpretation.

Exemptions and Non-Taxable Items

Not everything sold in Indiana is subject to sales tax. The state provides several important exemptions to encourage certain activities or provide relief. Understanding these exemptions can significantly impact a business’s tax liability.

One of the most prominent exemptions is for food for human consumption. This generally includes groceries purchased at a grocery store. However, this exemption typically does not extend to prepared foods, such as meals purchased from restaurants, delis, or vending machines, which are often considered taxable.

Prescription drugs and certain medical supplies are also typically exempt. This ensures that essential healthcare items are more accessible.

Newspapers and periodicals are generally exempt from sales tax, promoting the dissemination of information.

Sales for resale are a critical exemption. If a business purchases tangible personal property for the purpose of reselling it to another party, they typically do not pay sales tax on that purchase. They will, however, collect sales tax from their customer when they make the subsequent sale. This is often managed through the use of resale certificates.

Manufacturing and agricultural exemptions are also significant. Indiana offers specific exemptions for machinery, equipment, and materials used directly in the manufacturing process or in agricultural production. These exemptions are designed to foster economic growth in these vital sectors.

Other common exemptions might include:

- Certain sales to governmental or non-profit organizations.

- Sales of motor vehicles, boats, and aircraft (which are subject to different registration fees and taxes).

- Utilities, in some cases, may have specific tax treatments.

A thorough review of Indiana sales tax law is necessary to identify all applicable exemptions relevant to a particular business’s operations.

Registration and Filing Requirements

To legally collect and remit Indiana sales tax, businesses must first register with the Indiana Department of Revenue. This process typically involves obtaining an Indiana Taxpayer Identification Number (TID). The registration is usually completed online through the state’s dedicated tax portal.

Obtaining a Taxpayer Identification Number (TID)

The TID is essential for all tax-related activities in Indiana, including sales tax. Businesses that sell taxable goods or services in Indiana are generally required to register. This includes both in-state businesses and out-of-state businesses that establish a physical presence or meet certain economic nexus thresholds in Indiana.

Sales Tax Filing Frequency

Once registered, businesses will be assigned a filing frequency. The most common frequencies are monthly, quarterly, or annually. The determination of filing frequency is usually based on the business’s historical sales tax liability. Businesses with a higher volume of sales tax collected will typically be required to file more frequently.

- Monthly Filers: Businesses that have collected a significant amount of sales tax are typically required to file and remit sales tax on a monthly basis.

- Quarterly Filers: Businesses with a moderate sales tax liability may be designated as quarterly filers.

- Annual Filers: Businesses with very low sales tax liabilities might be eligible for annual filing.

The Indiana Department of Revenue will notify businesses of their assigned filing frequency. It is imperative to adhere to these deadlines, as late filings and payments can incur penalties and interest.

Filing Methods

Indiana offers several methods for filing sales tax returns:

- Online Filing: The most common and encouraged method is online filing through the Indiana Department of Revenue’s INTIME portal. This system allows for electronic submission of returns and payment.

- Paper Filing: In some limited circumstances, paper returns may be permitted, but electronic filing is strongly encouraged and often mandatory for larger businesses.

Economic Nexus: Selling into Indiana from Out-of-State

The concept of “economic nexus” has fundamentally changed how businesses, particularly those operating online or selling across state lines, are required to handle sales tax. Prior to the widespread adoption of economic nexus laws, a business generally only had to collect and remit sales tax in states where it had a physical presence (e.g., an office, warehouse, or employees).

Indiana, like many other states, has adopted economic nexus legislation. This means that even if a business does not have a physical presence in Indiana, it may still be required to register and collect Indiana sales tax if its sales into the state exceed certain thresholds.

The Indiana Economic Nexus Threshold

Indiana’s economic nexus threshold is generally based on a combination of sales revenue and the number of separate transactions into the state. Specifically, a remote seller is presumed to have established economic nexus and is therefore required to collect and remit Indiana sales tax if, in the current or previous calendar year, either of the following occurs:

- The seller’s gross revenue from sales of tangible personal property and taxable services delivered into Indiana exceeds $100,000.

- The seller engages in 200 or more separate transactions involving the sale of tangible personal property and taxable services delivered into Indiana.

These thresholds are designed to capture businesses that have a significant economic impact in Indiana, even without a physical footprint. It is crucial for businesses to monitor their sales into Indiana to ensure they do not inadvertently trigger economic nexus obligations.

Compliance for Remote Sellers

For businesses that meet the economic nexus thresholds, compliance involves several key steps:

- Registration: Register with the Indiana Department of Revenue to obtain a TID.

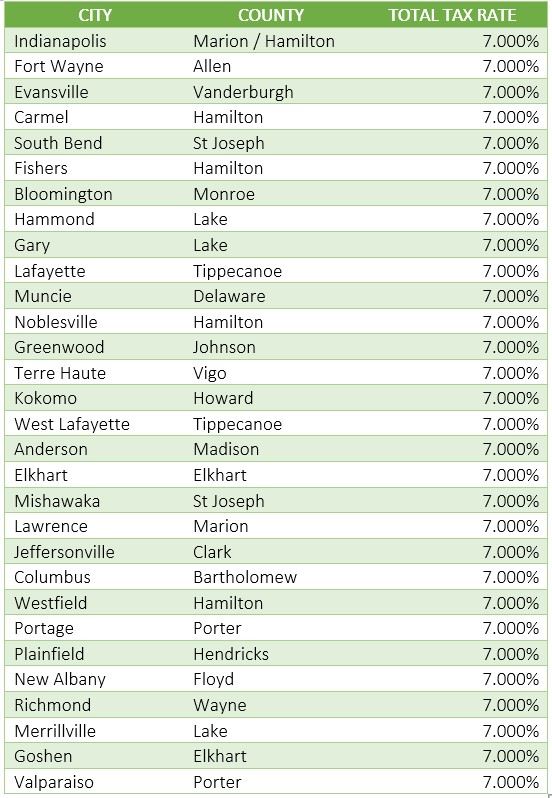

- Collection: Implement systems to accurately calculate and collect sales tax on all applicable sales to Indiana customers. This requires understanding Indiana’s tax rates, which can vary by locality.

- Remittance: File periodic sales tax returns and remit the collected tax to the state.

- Record Keeping: Maintain comprehensive records of all sales, tax collected, and filings for audit purposes.

The complexity of sales tax laws, especially with the evolution of economic nexus, underscores the importance of seeking professional advice from tax advisors or legal counsel to ensure full compliance and avoid potential penalties. Understanding “what is Indiana sales tax” is not just about knowing the rate; it’s about understanding the broad framework of obligations and responsibilities for businesses operating in the Hoosier State.