![]()

Understanding the Fundamentals of House Equity

House equity represents a homeowner’s financial stake in their property—the portion truly owned, free of outstanding loans. A home is often a primary asset, and building equity is a key financial goal, offering a safety net, potential funds, or a path to wealth. Grasping this concept is vital for informed property and financial decisions.

Defining Home Equity

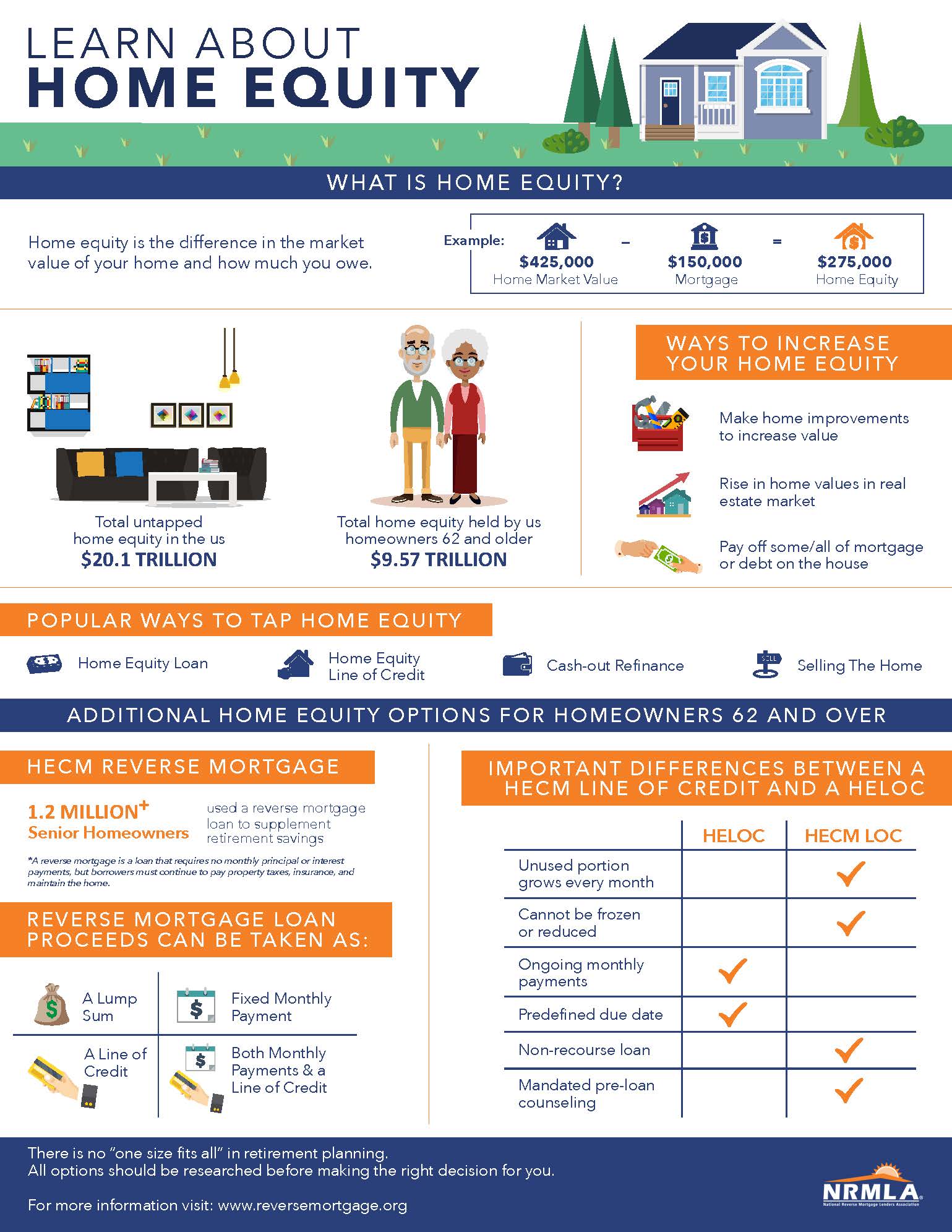

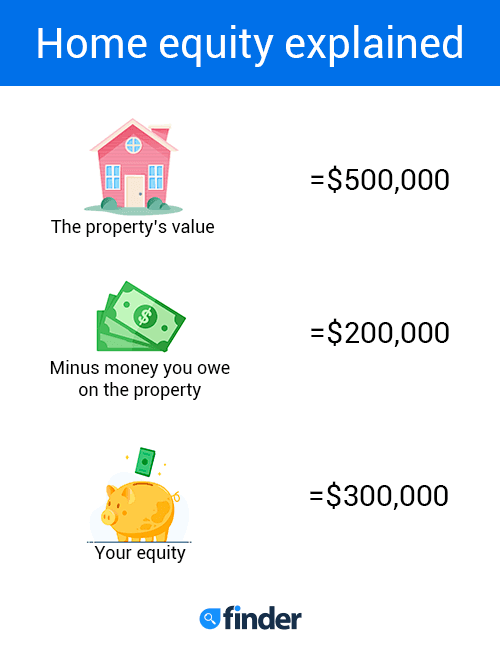

Home equity is the difference between your home’s current market value and your total mortgage(s) and other liens. It signifies the value returned if you sold and paid off all associated debts. This figure is dynamic: it grows with mortgage principal payments and property appreciation, but can decrease with depreciation or additional borrowing.

The Simple Calculation: Value Minus Debt

Calculate house equity simply:

Home Equity = Current Market Value – Total Outstanding Mortgage Balance (and any other liens)

For example, a $400,000 home with $250,000 debt yields $150,000 equity. Include all secured debts for accuracy. Regular calculation helps track your financial position.

Factors Influencing House Equity

Several key factors contribute to home equity’s growth or decline, enabling homeowners to make strategic decisions.

Market Appreciation

Rising local property values directly increase your home’s market value, boosting equity. This appreciation stems from strong economies, low housing supply, high demand, and attractive interest rates. While external, selecting property in a growing area accelerates equity. Conversely, market downturns cause depreciation and reduce equity.

Principal Payments and Mortgage Paydown

Consistently paying down your mortgage principal is a fundamental, controllable way to build equity. As the principal balance decreases, your ownership stake grows. Though early payments lean towards interest, the principal portion increases over time. Extra principal payments significantly accelerate accumulation and reduce loan terms.

Home Improvements and Renovations

Strategic home improvements can enhance property value and thus equity. High-ROI projects like kitchen/bathroom remodels, adding usable space, or improving curb appeal are most effective. Research local trends to ensure renovations add genuine market value, avoiding over-improving for the neighborhood without a financial return.

Economic Conditions and Interest Rates

Broad economic health influences housing demand and values. Robust economies, with job growth and higher wages, typically raise home values. Interest rates also matter; lower rates boost affordability, stimulating demand and prices, which in turn boosts equity. Higher rates can cool the market. Understanding these macroeconomic factors helps anticipate equity shifts.

How to Determine Your Current Home Equity

Accurately knowing your home equity is essential for financial planning and exploring leveraging options.

Obtaining a Property Valuation

A professional appraisal offers the most precise market value. An appraiser inspects your property, evaluates features, and compares it to recent local sales for an unbiased estimate. Alternatively, a real estate agent’s comparative market analysis (CMA) provides a free estimate based on similar sales. Online tools offer quick but less accurate estimates.

Reviewing Your Mortgage Statements

After estimating market value, determine your outstanding mortgage balance from monthly statements or by contacting your lender. The statement details your principal balance. Include balances from any additional secured loans (e.g., second mortgage, HELOC) to calculate your “total outstanding mortgage balance” for accurate equity assessment.

Leveraging Your House Equity

Once substantial equity accumulates, it becomes a valuable financial asset, offering various utilization options for homeowners.

Home Equity Loans

A home equity loan is a second mortgage providing a lump sum, secured by your home’s equity. It features a fixed interest rate and repayment schedule, ensuring consistent monthly payments. Ideal for major, one-time expenses like renovations, debt consolidation, or education. Being secured, rates are often lower than unsecured loans, but default risks foreclosure.

Home Equity Lines of Credit (HELOCs)

A HELOC functions like a revolving credit line, allowing flexible borrowing up to a limit during a “draw period.” You only pay interest on borrowed amounts. HELOCs typically have variable interest rates, meaning payments can fluctuate. While offering flexibility for ongoing needs, they demand discipline to prevent escalating debt.

Cash-Out Refinancing

Cash-out refinancing replaces your existing mortgage with a new, larger loan. The difference between the new loan amount and your old balance (after closing costs) is paid to you in cash. This can secure a lower interest rate on the entire mortgage if rates dropped, but it extends your term and increases total debt. Useful for large expenditures or high-interest debt consolidation.

Selling Your Home

The most direct way to access equity is by selling your property. Proceeds first cover outstanding mortgage(s), other liens, commissions, and closing costs. The remaining sum is your cash equity. This capital can fund a new home down payment, investments, or other financial goals. Selling is a significant decision, typically driven by lifestyle changes, relocation, or upgrading/downsizing.

Risks and Considerations When Using Equity

While leveraging home equity offers significant financial opportunities, understanding and mitigating associated risks is crucial for long-term financial stability.

Increased Debt Burden

Leveraging equity (loan, HELOC, refinance) increases your monthly financial obligations. Without proportional income growth or an adequate emergency fund, meeting higher payments becomes challenging, reducing financial flexibility. Rigorous assessment of your financial capacity is essential before taking on more debt.

Market Fluctuations

Your equity is tied to your home’s market value. If you borrow against equity and the housing market declines, your home’s value might fall below your total mortgage debt. This “underwater” situation severely limits selling or refinancing without significant loss and can trap you, making relocation difficult.

Foreclosure Risk

All equity-backed loans are secured by your home; defaulting risks foreclosure. Failure to make payments allows the lender to seize your property. Foreclosure means losing your home, damaging credit, and making future housing/credit difficult. A clear repayment strategy and robust emergency fund are vital.

Impact on Future Financial Flexibility

Utilizing substantial current equity can diminish future financial options. Draining reserves limits access to this cushion for emergencies, investments, or life events. Maintaining conservative equity provides a buffer against challenges and preserves future financial maneuverability, preventing over-leveraging from turning an asset into stress.