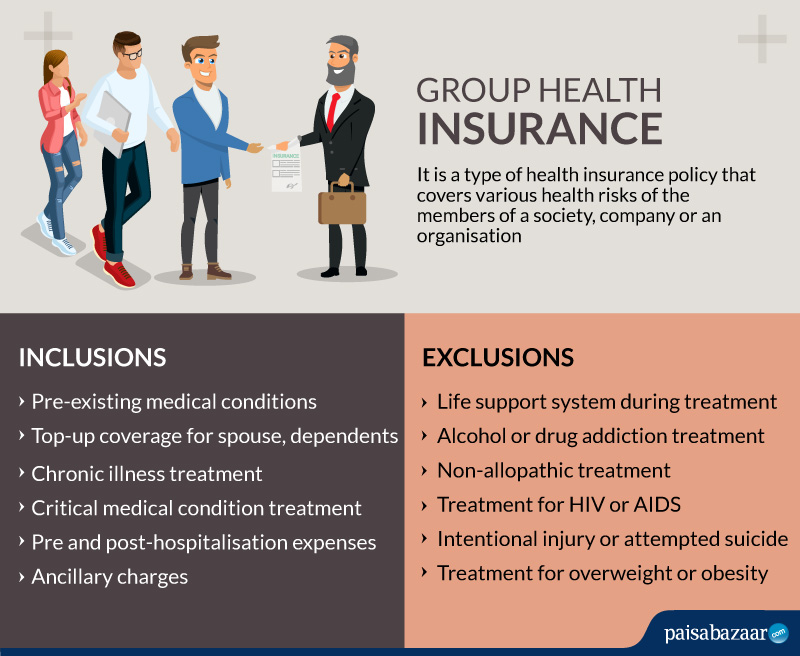

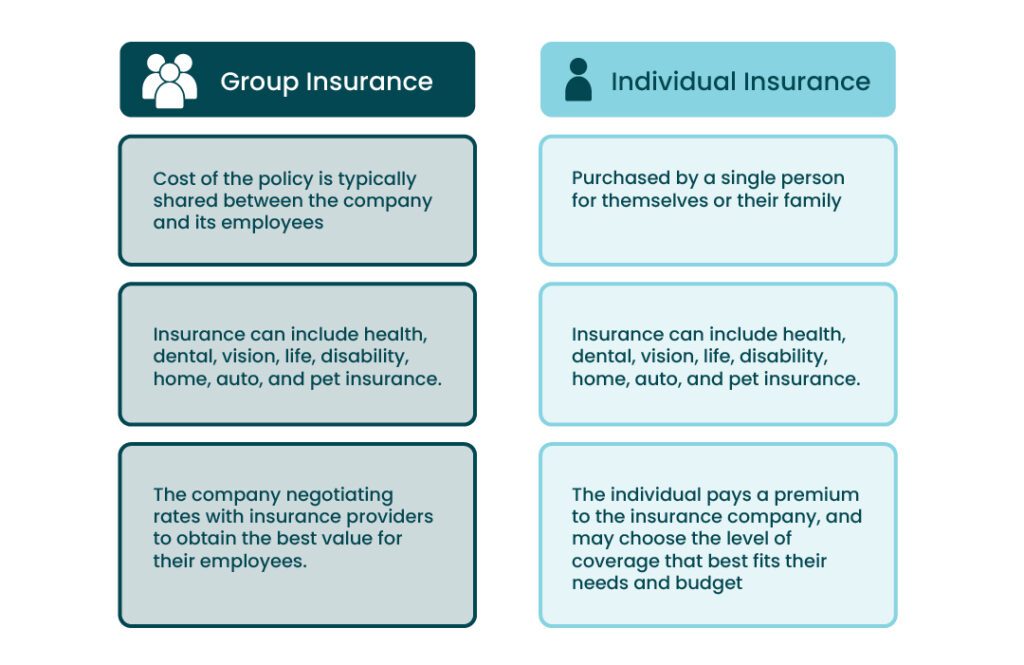

Group coverage health insurance is a type of health insurance plan that provides medical benefits to a group of individuals, typically employees of a company or members of an organization. Unlike individual health insurance plans, which are purchased by individuals or families on their own, group plans are offered by an employer or other entity to its members. This collective purchasing power often leads to more affordable premiums and a wider range of benefits.

Understanding the Basics of Group Health Insurance

At its core, group coverage health insurance is a benefit designed to protect the health and financial well-being of a group of people. Employers, unions, associations, and other organizations can offer these plans to their members as a valuable perk. The primary advantage lies in the pooling of risk. When a larger group of people are insured together, the likelihood of any single individual facing extremely high medical costs is spread across the entire group. This generally results in lower per-person premiums compared to what individuals might pay for similar coverage on the open market.

The structure of a group health insurance plan is typically determined by the sponsoring organization. This includes selecting the type of plan, the level of coverage, the deductible amounts, copayments, and coinsurance. While the employer or organization often pays a portion, if not all, of the premium, employees usually contribute a share as well. The specific details of these contributions are outlined in the plan documents provided by the employer.

One of the key differentiators of group coverage is its group-specific underwriting. Insurers assess the risk of the entire group rather than individual applicants. This means that pre-existing conditions are generally not a barrier to obtaining coverage for group members, a significant departure from many individual plans prior to the Affordable Care Act (ACA). The ACA, however, has introduced regulations that protect individuals with pre-existing conditions in both individual and group markets.

Types of Group Health Insurance Plans

Group health insurance plans come in various forms, each offering different ways to access healthcare services and manage costs. Understanding these different types is crucial for both employers selecting a plan and employees choosing their coverage options.

Preferred Provider Organization (PPO) Plans

PPO plans are among the most popular types of group coverage. They offer members the flexibility to see any doctor or specialist they choose, whether they are in the network or out of network. However, PPOs encourage members to use providers within the plan’s network by offering lower out-of-pocket costs. This means that if you see a doctor within the network, your copayments, deductibles, and coinsurance will generally be less than if you see an out-of-network provider. PPOs typically do not require a referral to see a specialist, further enhancing flexibility.

Health Maintenance Organization (HMO) Plans

HMOs are a more restrictive type of plan but often come with lower premiums. With an HMO, you must choose a primary care physician (PCP) from the plan’s network. This PCP acts as your gatekeeper, coordinating your care and requiring a referral before you can see a specialist. All care, except for emergency services, must be obtained from providers within the HMO’s network. If you go outside the network, the HMO will likely not cover the costs, except in specific emergency situations.

Point of Service (POS) Plans

POS plans combine elements of both PPO and HMO plans. Like an HMO, you will typically need to select a PCP. However, POS plans offer more flexibility than traditional HMOs. You can choose to receive care from providers within the plan’s network, or you can go out of network. If you go out of network, you will likely have higher out-of-pocket costs and may need to file claims yourself. Referrals from your PCP are usually required for specialist care, even if you are staying within the network.

Exclusive Provider Organization (EPO) Plans

EPO plans are a hybrid that limits coverage to providers within a specific network. There is no coverage for out-of-network providers, except in emergencies. Unlike HMOs, EPOs typically do not require you to select a PCP, and you generally do not need a referral to see a specialist, as long as they are within the EPO network. The cost-effectiveness of EPOs often stems from their more limited network of providers.

High Deductible Health Plans (HDHPs) with Health Savings Accounts (HSAs)

HDHPs are characterized by lower monthly premiums but significantly higher deductibles. These plans are often paired with Health Savings Accounts (HSAs). An HSA is a tax-advantaged savings account that allows individuals to set aside money for qualified medical expenses. The contributions to an HSA are tax-deductible, the funds grow tax-free, and withdrawals for qualified medical expenses are also tax-free. HDHPs are attractive to individuals who are generally healthy and anticipate lower healthcare utilization, as they can benefit from lower premiums and the tax advantages of an HSA.

Key Components and Considerations of Group Coverage

When an organization offers group coverage health insurance, there are several critical components and considerations that come into play, affecting both the employer and the employees.

Employer Contributions and Cost Sharing

A significant aspect of group health insurance is how the premium costs are shared. Employers can choose to cover a portion or the entirety of the monthly premiums. This decision is a crucial factor in employee satisfaction and retention. The percentage of premium an employer covers can vary widely, with some covering 100% of employee-only coverage and others contributing a set amount or percentage. Employees are typically responsible for the remaining portion of the premium, which is often deducted from their paychecks on a pre-tax basis, offering tax savings.

Eligibility and Enrollment

Group health insurance plans have specific eligibility requirements. Generally, employees who work a certain number of hours per week (e.g., 30 hours) are eligible for coverage. New employees typically have a waiting period before they can enroll, which can range from 30 to 90 days. During an open enrollment period, typically held once a year, employees can enroll in a plan, make changes to their existing coverage, or drop coverage. Special enrollment periods may also be available for life events such as marriage, divorce, or the birth of a child.

Benefits and Coverage Levels

The benefits offered under a group health insurance plan are determined by the employer in consultation with the insurance provider. These benefits commonly include:

- Medical Services: Doctor visits (primary care and specialists), hospital stays, emergency room services, surgical procedures.

- Prescription Drugs: Coverage for medications, often with different tiers of copayments based on whether the drug is generic, preferred brand, or non-preferred brand.

- Preventive Care: Services aimed at preventing illness or detecting it early, such as annual physicals, vaccinations, and screenings. These are often covered at 100% by the ACA.

- Mental Health Services: Counseling, therapy, and psychiatric care.

- Maternity and Newborn Care: Prenatal care, delivery, and postnatal care for newborns.

- Pediatric Services: Well-child visits, immunizations, and treatment for childhood illnesses.

The level of coverage refers to how much of the healthcare costs the plan will pay for after deductibles and copayments. This is often measured by the actuarial value of the plan.

Network Restrictions and Out-of-Pocket Costs

As discussed in the plan types, group coverage often involves network restrictions. Staying within the plan’s network of doctors, hospitals, and other healthcare providers usually results in lower costs for the insured. Out-of-pocket costs are the expenses that the insured person pays directly. These include:

- Deductibles: The amount you pay for covered healthcare services before your insurance plan starts to pay.

- Copayments (Copays): A fixed amount you pay for a covered healthcare service after you’ve paid your deductible.

- Coinsurance: Your share of the costs of a covered healthcare service, calculated as a percentage of the allowed amount for the service.

- Out-of-Pocket Maximum: The most you will have to pay for covered services in a plan year. Once you reach this limit, your health plan pays 100% of the allowed amount for covered benefits for the rest of the year.

Advantages of Group Coverage Health Insurance

Group health insurance offers a multitude of benefits for both employers and employees, making it a cornerstone of employee benefits packages.

For Employees:

- Affordability: Group plans typically have lower premiums than individual plans due to the collective bargaining power of the group. Employers also often subsidize a significant portion of the premium costs.

- Access to Comprehensive Benefits: Group plans often include a broader range of benefits and services than might be affordable through individual plans, including prescription drug coverage, mental health services, and preventive care.

- Simplified Enrollment: Open enrollment periods make it relatively straightforward to enroll or make changes to coverage.

- Pre-Tax Premiums: Premiums are usually deducted from paychecks before taxes are calculated, reducing an employee’s taxable income.

- No Medical Underwriting (Generally): For most group plans, pre-existing conditions do not prevent an individual or their dependents from obtaining coverage, ensuring access to necessary care.

For Employers:

- Attracting and Retaining Talent: Offering competitive health benefits is a major draw for prospective employees and a key factor in retaining existing staff.

- Improved Employee Health and Productivity: Healthier employees are more productive and take fewer sick days. Group coverage encourages employees to seek preventive care and treatment for illnesses.

- Tax Advantages: Employer contributions to group health insurance premiums are generally tax-deductible as a business expense.

- Employee Morale and Loyalty: Providing a valuable benefit like health insurance demonstrates that an employer cares about the well-being of its workforce, fostering a positive work environment.

- Risk Pooling: Employers help their employees manage healthcare costs by pooling risk across the entire group.

The Role of the Affordable Care Act (ACA)

The Affordable Care Act (ACA), also known as Obamacare, has significantly impacted group health insurance. Key provisions of the ACA that affect group plans include:

- Guaranteed Issue: Insurers cannot deny coverage to any applicant in the individual or group market, regardless of health status or pre-existing conditions.

- Essential Health Benefits: Plans must cover a set of ten essential health benefits, including ambulatory patient services, emergency services, hospitalization, prescription drugs, and mental health services.

- Preventive Care Coverage: Most group plans must cover a range of preventive services without cost-sharing (no copay, deductible, or coinsurance).

- Medical Loss Ratio (MLR): Insurers must spend a minimum percentage of premium revenue on medical claims and quality improvement activities. If they don’t meet this threshold, they must issue rebates to policyholders.

- No Lifetime or Annual Limits: The ACA prohibits lifetime and annual dollar limits on essential health benefits.

These regulations ensure that group health insurance plans provide meaningful coverage and protect consumers from financial hardship due to medical expenses.

Navigating Group Coverage Decisions

Choosing a group health insurance plan can be a complex process, involving careful consideration of personal healthcare needs, financial situations, and the options provided by the employer. It is important to review the plan documents thoroughly, compare deductibles, copayments, coinsurance, and out-of-pocket maximums. Understanding the network of providers and whether preferred doctors or hospitals are included is also critical. For many, group coverage health insurance remains the most accessible and affordable way to secure comprehensive medical protection.