The Sunshine State presents a unique landscape for vehicle ownership, characterized by its vibrant automotive culture, extensive road networks, and, unfortunately, a higher propensity for certain types of insurance claims. Understanding the intricacies of car insurance, particularly the concept of “full coverage,” is paramount for any Florida driver. While not a legally mandated term in itself, “full coverage” in Florida typically refers to a comprehensive suite of insurance policies designed to protect drivers from a wide array of financial risks, going beyond the state’s minimum liability requirements. This article will delve into what constitutes full coverage insurance in Florida, the individual components that comprise it, and why it’s a prudent choice for many residents navigating the complexities of the state’s insurance market.

Deconstructing “Full Coverage” in the Florida Context

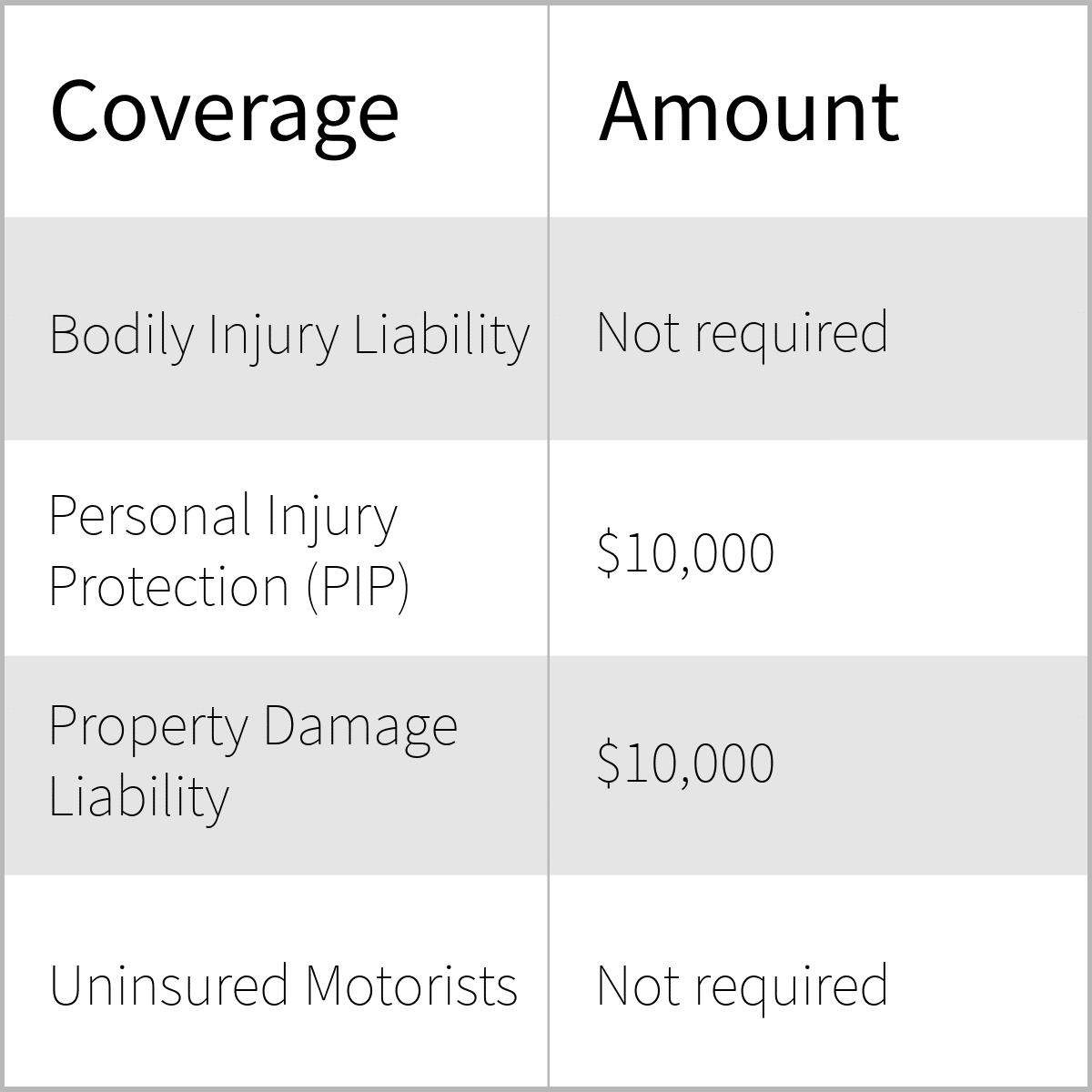

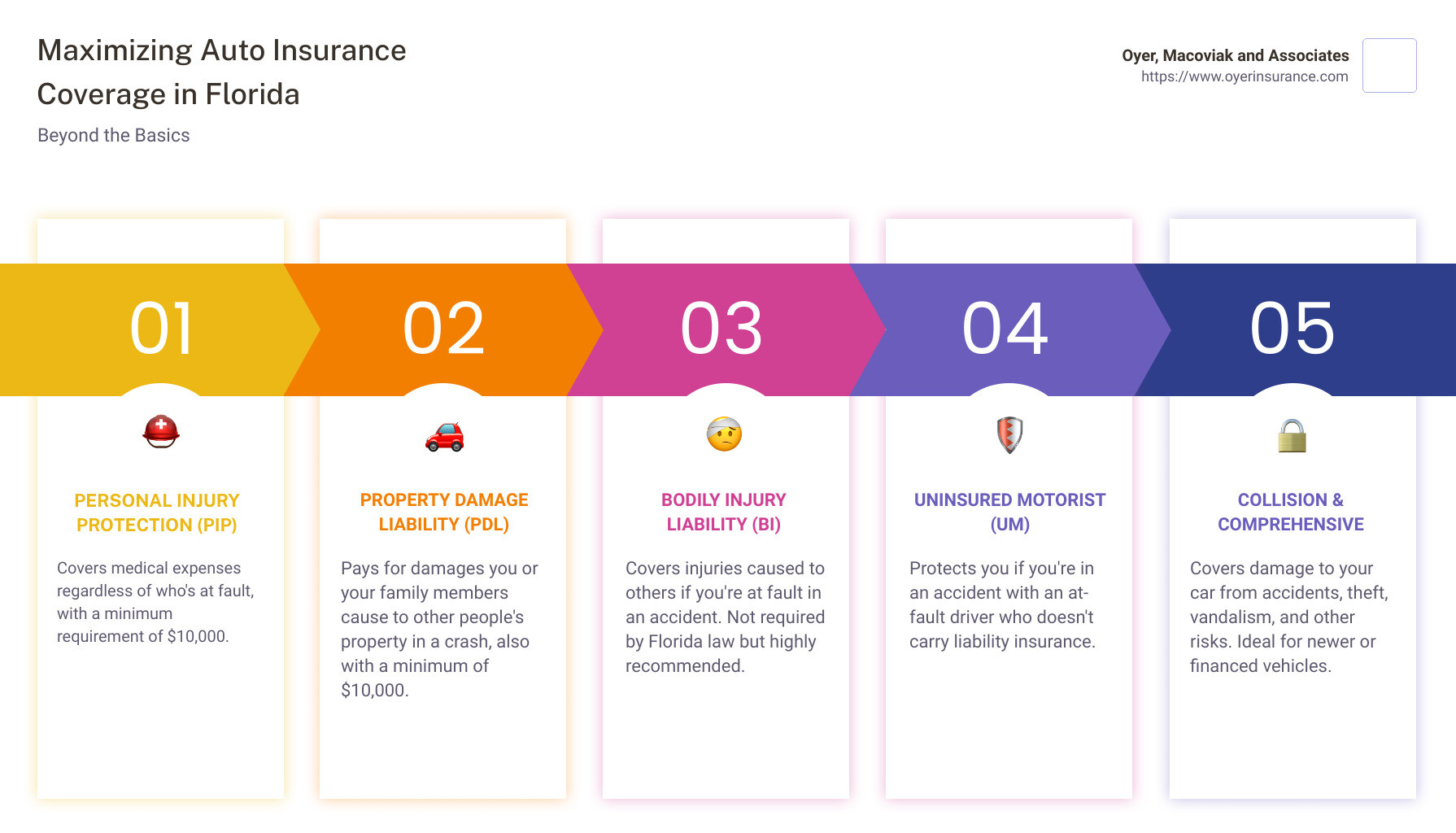

In Florida, the minimum insurance requirement is liability coverage, which includes Personal Injury Protection (PIP) and Property Damage Liability (PDL). PIP covers medical expenses and lost wages for you and your passengers, regardless of fault, up to a certain limit. PDL covers damage to other people’s property, such as their vehicles, in an accident you cause. However, this minimum coverage is often insufficient to shield drivers from significant financial burdens arising from damage to their own vehicle or other unforeseen events.

“Full coverage,” therefore, is a colloquial term used by consumers and insurance agents to describe a policy that bundles essential coverages to provide robust protection. It’s crucial to understand that “full coverage” is not a single, standardized policy. Instead, it’s a combination of different insurance types. The specific coverages included can vary slightly between insurers and depend on the driver’s choices and vehicle. However, the core components generally include:

Collision Coverage

This is a cornerstone of what most people consider “full coverage.” Collision insurance pays for damage to your vehicle if it collides with another vehicle or object, such as a tree, pole, or fence, regardless of who is at fault. This coverage is particularly important in Florida due to its dense traffic, frequent weather-related incidents, and the prevalence of fender benders. Without collision coverage, you would be personally responsible for the repair costs of your vehicle in such scenarios. The amount you pay out-of-pocket for this coverage is determined by your deductible, which is the amount you agree to pay before your insurance coverage kicks in. Choosing a higher deductible generally results in lower premiums, and vice versa.

Comprehensive Coverage

Often paired with collision coverage, comprehensive insurance, sometimes called “other than collision” coverage, protects your vehicle from damage caused by events other than a collision. This includes a wide range of incidents such as theft, vandalism, fire, natural disasters (like hurricanes, which are a significant concern in Florida), falling objects, and even animal strikes. Given Florida’s susceptibility to severe weather, including hurricanes and tropical storms, comprehensive coverage is invaluable for protecting your vehicle against wind damage, flooding, and debris impact. Like collision coverage, comprehensive coverage also has a deductible.

Uninsured/Underinsured Motorist (UM/UIM) Coverage

Florida has a significant number of uninsured drivers. Uninsured Motorist (UM) coverage protects you if you are involved in an accident with a driver who has no car insurance. Underinsured Motorist (UIM) coverage steps in when the at-fault driver has insurance, but their coverage limits are not high enough to cover the full extent of your damages. This coverage is vital in Florida because it ensures that you and your passengers are compensated for medical expenses, lost wages, and pain and suffering even if the negligent driver is unable to pay. UM/UIM coverage can be offered in two forms: bodily injury (UM/UIMBI) and property damage (UMPD). UMPD can be particularly useful in Florida as it can cover damage to your vehicle when an uninsured driver is at fault, often with a lower deductible than collision coverage.

Liability Coverage (Bodily Injury and Property Damage)

While Florida mandates minimum liability coverage, drivers opting for “full coverage” typically choose limits that far exceed these basic requirements. Bodily Injury Liability (BIL) covers medical expenses, lost wages, and pain and suffering for others if you are found to be at fault for an accident. Property Damage Liability (PDL) covers damage to the other party’s vehicle or other property. Increasing your liability limits is a critical component of true “full coverage” as it provides a substantial financial safety net, protecting your assets from lawsuits if you cause a serious accident.

Beyond the Basics: Additional Coverages for Florida Drivers

While the aforementioned coverages form the bedrock of “full coverage,” several other optional coverages can further enhance protection for Florida drivers:

Medical Payments (MedPay) Coverage

Though Florida has PIP, some drivers opt for MedPay to supplement its coverage, particularly for expenses not fully covered by PIP or for individuals who don’t qualify for full PIP benefits. MedPay can help pay for medical and funeral expenses for you and your passengers, regardless of fault.

Rental Reimbursement Coverage

If your vehicle is damaged in a covered incident and is undriveable, rental reimbursement coverage helps pay for the cost of a rental car while yours is being repaired. This can be a lifesaver in Florida, especially if you rely on your vehicle for daily commutes or family needs and live in an area with limited public transportation.

Roadside Assistance and Towing

This coverage provides assistance if your vehicle breaks down, runs out of gas, has a dead battery, or requires towing. Given Florida’s often hot and humid conditions, or during severe weather events, having roadside assistance can provide much-needed peace of mind.

Gap Insurance

If you have a loan or lease on your vehicle, gap insurance covers the difference between what you owe on your loan or lease and the actual cash value of your car if it’s declared a total loss due to an accident, theft, or natural disaster. This is especially relevant for newer vehicles that depreciate rapidly.

Why “Full Coverage” is Essential in Florida

Florida’s unique driving environment necessitates a more comprehensive approach to car insurance. Several factors contribute to the importance of “full coverage”:

High Traffic Density and Congestion

Major metropolitan areas in Florida, such as Miami, Orlando, and Tampa, experience significant traffic congestion. This increases the likelihood of accidents, making collision and liability coverages essential.

Weather-Related Risks

Florida is renowned for its susceptibility to hurricanes, tropical storms, and severe thunderstorms. These events can cause widespread damage to vehicles through wind, flooding, and falling debris. Comprehensive coverage is critical for mitigating the financial impact of such events.

High Rate of Uninsured Drivers

Despite mandatory insurance laws, Florida consistently ranks among states with a high percentage of uninsured drivers. This underscores the importance of Uninsured Motorist coverage to protect yourself from drivers who do not carry adequate insurance.

Cost of Vehicle Repairs and Replacements

Modern vehicles are equipped with sophisticated technology and safety features, making repairs expensive. “Full coverage” ensures that you are not saddled with exorbitant repair bills out-of-pocket.

Protecting Your Assets

In the event of a serious accident, liability claims can quickly escalate into substantial financial liabilities. Having ample liability coverage protects your personal assets, such as your home and savings, from being seized to satisfy legal judgments.

Making Informed Decisions

When discussing “full coverage” with an insurance provider in Florida, it’s vital to clarify precisely which coverages are included and at what limits. Do not assume that the term “full coverage” automatically encompasses every possible scenario. Always ask for a detailed breakdown of your policy, including:

- Deductible amounts: Understand how much you will pay out-of-pocket for collision and comprehensive claims.

- Coverage limits: Ensure your liability and uninsured/underinsured motorist limits are adequate to protect your financial well-being.

- Optional coverages: Evaluate whether add-ons like rental reimbursement or roadside assistance are beneficial for your lifestyle.

- Exclusions: Be aware of any specific situations or damages that your policy does not cover.

Ultimately, “full coverage” insurance in Florida is not a single product but rather a strategic combination of insurance policies designed to offer a robust safety net. By understanding its components and tailoring it to your individual needs and the specific risks present in Florida, you can secure peace of mind and financial security on the road.