The world of insurance can often feel like navigating a complex maze of acronyms and specialized terminology. One such term that may surface, particularly in discussions related to health benefits and employee compensation, is “FSA.” Understanding what an FSA is and how it operates within the insurance landscape is crucial for individuals and employers alike to make informed decisions about healthcare spending and financial planning. This article delves into the intricacies of Flexible Spending Accounts (FSAs), clarifying their purpose, operation, and the advantages they offer.

Understanding the Basics of Flexible Spending Accounts (FSAs)

At its core, a Flexible Spending Account is a pre-tax benefit account that allows individuals to set aside money from their paycheck to pay for qualified medical expenses. These accounts are typically offered by employers as part of their employee benefits package. The primary advantage of an FSA is the tax savings it provides. Because contributions are made before federal, state, and Social Security taxes are calculated, the amount of taxable income is reduced, leading to lower tax liabilities.

The Purpose and Functionality of an FSA

The fundamental purpose of an FSA is to make healthcare more affordable by reducing the out-of-pocket costs associated with medical care. It acts as a supplementary savings vehicle, distinct from regular health insurance, which primarily covers costs after deductibles, copayments, and coinsurance have been met. An FSA, on the other hand, can be used to pay for a wide range of eligible medical, dental, and vision expenses that might not be fully covered by a traditional insurance plan, or for those with high-deductible plans.

The functionality of an FSA is relatively straightforward. An employee elects to contribute a certain amount of money from their salary to their FSA during an open enrollment period. This amount is then deducted from each paycheck on a pre-tax basis. The accumulated funds in the FSA can then be used throughout the plan year to pay for eligible expenses. It’s important to note that FSAs have specific rules regarding what expenses are considered “qualified” and how the funds can be accessed.

Key Features and Eligibility

Eligibility for an FSA is typically tied to employment. If an employer offers an FSA as a benefit, employees can choose to participate. There are generally two main types of FSAs: health FSAs and dependent care FSAs. This article will focus primarily on health FSAs, as they are more commonly associated with the term “insurance” in a broader sense.

A key feature of health FSAs is the “use-it-or-lose-it” rule. This means that generally, any funds remaining in the account at the end of the plan year are forfeited. However, employers may offer a grace period or a carryover option, allowing a certain amount of unused funds to be rolled over to the next plan year. The specifics of these provisions vary by employer and plan.

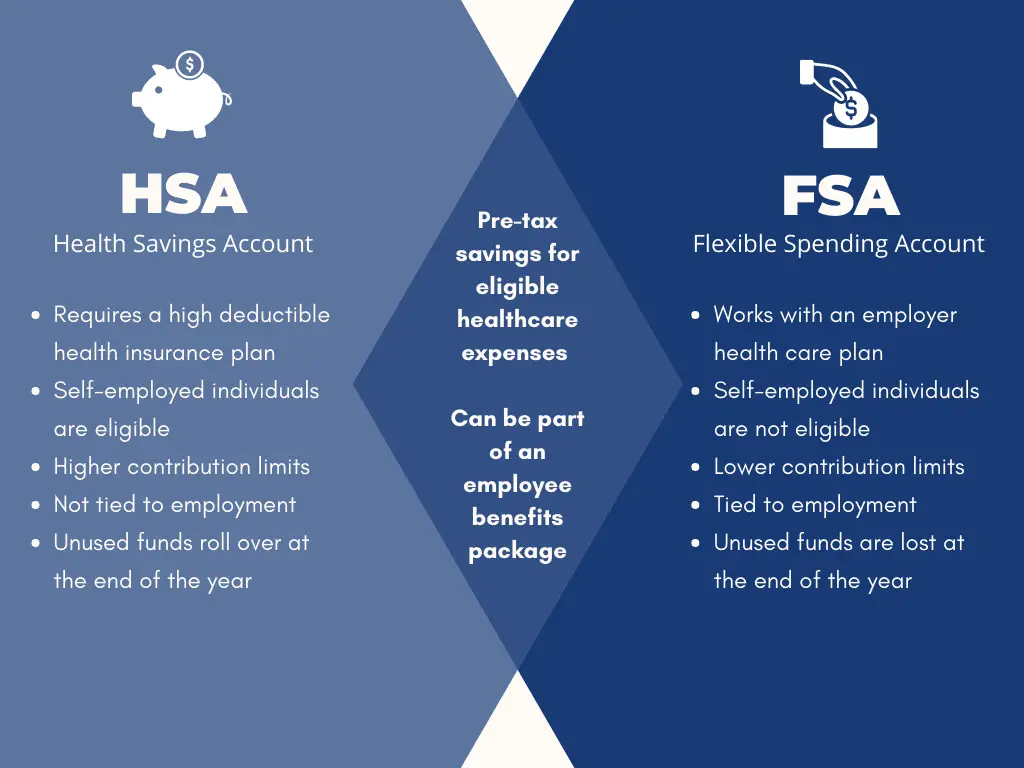

Distinguishing FSAs from Health Savings Accounts (HSAs)

It is common for FSAs to be confused with Health Savings Accounts (HSAs). While both offer tax advantages for healthcare spending, they have significant differences. HSAs are only available to individuals enrolled in High Deductible Health Plans (HDHPs). Unlike FSAs, HSAs are owned by the individual, not the employer, and funds do not expire. Unused HSA funds roll over year after year and can even be invested, growing over time. FSAs, on the other hand, are employer-sponsored, have a shorter time horizon for use, and typically do not offer investment options. The “use-it-or-lose-it” nature of FSAs is a critical distinction.

Navigating the Mechanics of an FSA

Understanding how to effectively utilize an FSA requires a grasp of its operational mechanics, from contribution limits to the process of reimbursement and the types of expenses it covers. This section will break down these elements to provide a comprehensive picture of FSA management.

Contribution Limits and Plan Year

Each year, the IRS sets maximum contribution limits for health FSAs. These limits are subject to change annually. Employers will communicate these limits to their employees. During the open enrollment period, employees decide how much they wish to contribute for the upcoming plan year, up to the maximum allowed. This elected amount is then divided equally across the pay periods within that year.

The plan year for an FSA typically runs for 12 months, but the start and end dates are determined by the employer. It’s crucial for participants to be aware of their specific plan year dates to ensure they utilize their funds before they expire, considering any grace periods or carryover options.

Reimbursement and Claim Submission

There are typically two common methods for accessing FSA funds:

- Debit Card: Many FSAs come with a special debit card that can be used directly at the point of service for eligible expenses. This offers immediate convenience, eliminating the need for upfront out-of-pocket payment and subsequent reimbursement requests. The card is linked to the FSA balance, and purchases are automatically deducted.

- Reimbursement: Alternatively, participants can pay for eligible expenses out-of-pocket and then submit a claim for reimbursement. This usually involves filling out a claim form and providing supporting documentation, such as receipts or Explanation of Benefits (EOBs) from insurance companies. The administrator then processes the claim and issues reimbursement, typically via direct deposit or check.

It is essential to keep all receipts and supporting documentation for at least the duration of the plan year and often a little longer, as the FSA administrator may request them for verification.

Eligible Expenses and Qualified Medical Costs

The IRS outlines a comprehensive list of qualified medical, dental, and vision expenses that can be paid for with FSA funds. These are generally expenses that would also be deductible on your federal income tax return if you itemized deductions. Common examples include:

- Medical Services: Doctor visits, hospital stays, prescription medications, and co-payments for specialists.

- Dental Care: Cleanings, fillings, braces, and other dental procedures.

- Vision Care: Eye exams, prescription eyeglasses, contact lenses, and corrective surgery like LASIK.

- Medical Equipment: Crutches, bandages, and diagnostic devices.

- Preventive Care: Certain screenings and wellness programs not fully covered by insurance.

- Mental Health Services: Therapy and counseling.

There are also specific rules for certain expenses, such as over-the-counter medications. Prior to the CARES Act, many over-the-counter medications required a prescription to be eligible for FSA reimbursement. However, the CARES Act expanded eligibility to include most over-the-counter medicines and menstrual care products without a prescription. Always consult your FSA plan administrator or the IRS guidelines for the most up-to-date information on eligible expenses.

Maximizing the Benefits of Your FSA

Effectively managing an FSA can lead to significant cost savings. This involves careful planning, understanding the rules, and making strategic decisions throughout the plan year.

Strategic Planning and Budgeting

The key to maximizing an FSA is proactive planning. Before the open enrollment period, it’s wise to review your anticipated healthcare needs for the upcoming year. Consider:

- Known Medical Expenses: Are you expecting any surgeries, dental work, or ongoing treatments?

- Chronic Conditions: Do you or a family member have a chronic condition that requires regular medication or doctor visits?

- Vision Needs: Do you anticipate needing new glasses or contact lenses?

- Co-pays and Deductibles: How much do you typically spend on these out-of-pocket costs?

Based on these assessments, you can make a more informed decision about the contribution amount. It’s generally better to slightly overestimate your needs rather than underestimate them, given the “use-it-or-lose-it” nature of the account. However, excessive overestimation can lead to forfeited funds.

Understanding the “Use-It-or-Lose-It” Rule and Rollover Options

As mentioned, the “use-it-or-lose-it” rule is a critical aspect of FSAs. To mitigate the risk of losing funds, consider these strategies:

- Regularly Monitor Your Balance: Keep track of how much you have spent and how much remains in your account.

- Plan for Year-End Expenses: If you have remaining funds towards the end of the plan year, consider purchasing items that you will need in the near future, such as prescription refills, contact lens solution, or over-the-counter pain relievers.

- Utilize the Grace Period or Carryover: If your employer offers a grace period, this gives you an additional 2.5 months into the next plan year to incur and submit claims for expenses incurred during the previous plan year. If a carryover is offered, a specific amount (determined by the IRS and your employer) can be rolled over to the next year. Be aware that if you have a carryover, you may not be able to contribute the full amount to your FSA in the following year, depending on the rules.

Tips for Effective FSA Management

- Keep Detailed Records: Maintain a clear record of all expenses paid with FSA funds and keep all original receipts and EOBs. This is crucial for reimbursement claims and for your own financial tracking.

- Stay Informed: Regularly check communications from your FSA administrator and employer regarding deadlines, eligible expenses, and any changes to the plan rules.

- Consult Your Plan Documents: Familiarize yourself with the specific terms and conditions of your employer’s FSA plan.

- Seek Professional Advice: If you are unsure about eligible expenses or how to best manage your FSA, consider consulting with a financial advisor or your HR department.

In conclusion, a Flexible Spending Account (FSA) is a valuable pre-tax benefit that can significantly reduce the cost of healthcare for employees. By understanding its purpose, mechanics, and by employing strategic planning and diligent management, individuals can effectively leverage FSAs to save money on qualified medical, dental, and vision expenses, thereby enhancing their overall financial well-being and access to necessary care.