The term “forbearance” might sound complex, but at its core, it’s a crucial lifeline for homeowners facing temporary financial hardship. In the realm of mortgage lending, forbearance refers to a temporary agreement between a borrower and their lender to reduce or suspend mortgage payments for a specified period. This isn’t a handout; it’s a structured pause designed to help individuals navigate challenging circumstances, such as job loss, illness, or natural disasters, without immediately defaulting on their loan. Understanding forbearance is essential for any homeowner who may encounter financial difficulties, offering a pathway to financial recovery and preventing the devastating consequences of foreclosure.

Understanding the Fundamentals of Mortgage Forbearance

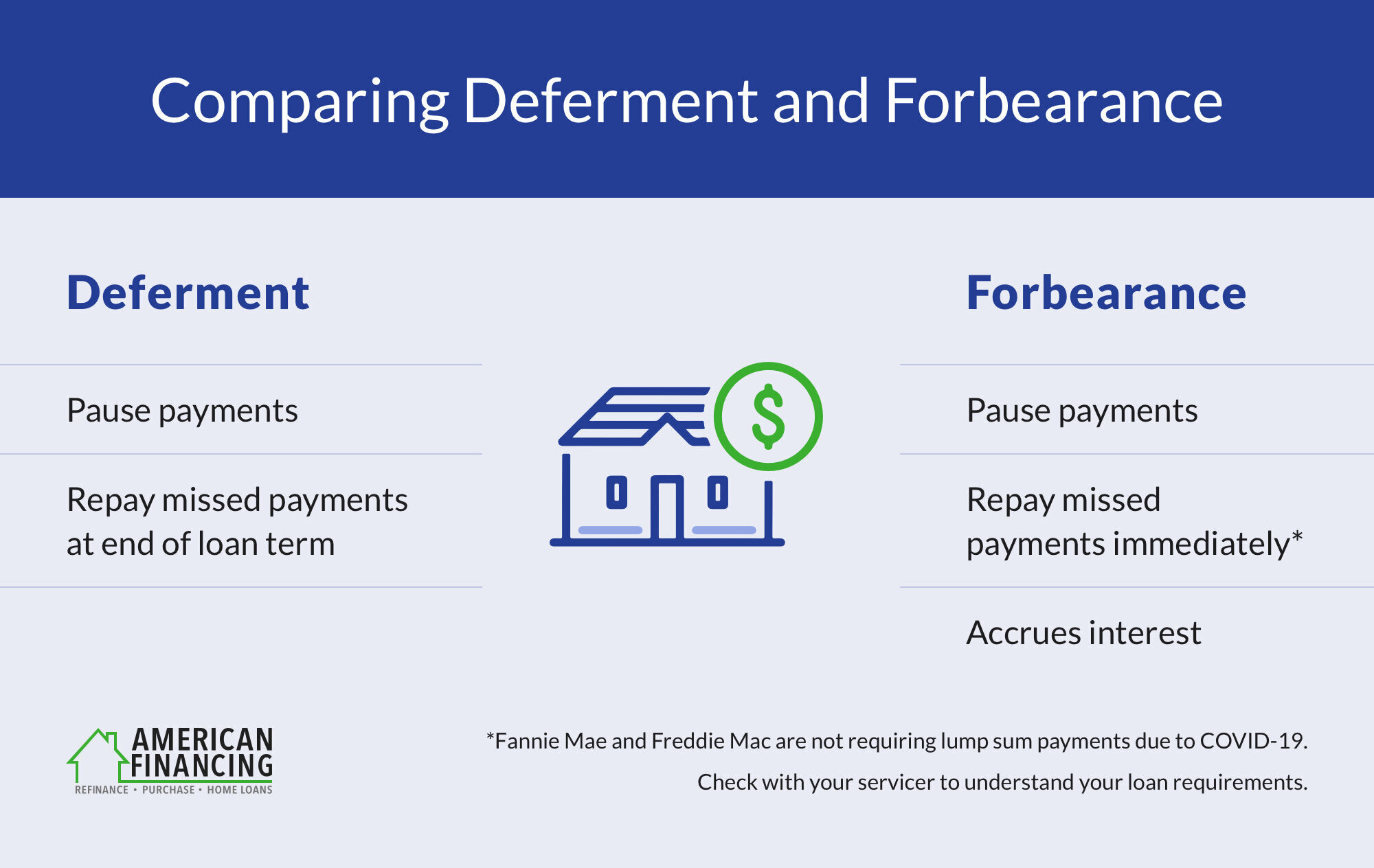

At its most basic, mortgage forbearance is a formal arrangement where a lender agrees to temporarily ease the payment obligations of a borrower. This is not a loan modification, which permanently alters the terms of your mortgage, nor is it a forgiveness of debt. Instead, it’s a deferral of payments that must eventually be repaid. The primary goal is to provide immediate relief, allowing borrowers time to regain their financial footing.

The Purpose and Benefits of Forbearance

The overarching purpose of forbearance is to prevent borrowers from falling behind on their mortgage payments to the point of default. By offering a temporary reprieve, lenders aim to:

- Prevent Foreclosure: This is the most significant benefit. Foreclosure is a lengthy and costly process for both the lender and the borrower. Forbearance provides a crucial window to avoid this outcome.

- Allow Time for Financial Recovery: Job loss, unexpected medical bills, or business setbacks can create severe financial strain. Forbearance gives individuals the breathing room they need to find new employment, recover from illness, or stabilize their financial situation.

- Maintain Homeownership: For many, their home is their most significant asset and a source of stability. Forbearance helps preserve this asset and the security it provides.

- Mitigate Damage to Credit Score: While forbearance might be reported to credit bureaus, it generally has a less severe impact on a credit score than missed payments or a foreclosure.

Eligibility and Application Process for Forbearance

While the specifics can vary by lender and loan type, several general criteria determine eligibility for mortgage forbearance. These often include:

- Demonstrated Financial Hardship: Lenders will typically require proof of a significant, involuntary reduction in income or an increase in essential living expenses. This could include documentation like termination letters, medical bills, or proof of reduced business revenue.

- Loan Type: Government-backed loans (FHA, VA, USDA) often have specific forbearance programs with defined terms. Conventional loans may also offer forbearance, but the terms can be more flexible and negotiated with the individual lender.

- Timeliness: It is crucial to contact your lender as soon as you anticipate or experience financial difficulty. Waiting until you’ve already missed payments can make the process more complicated.

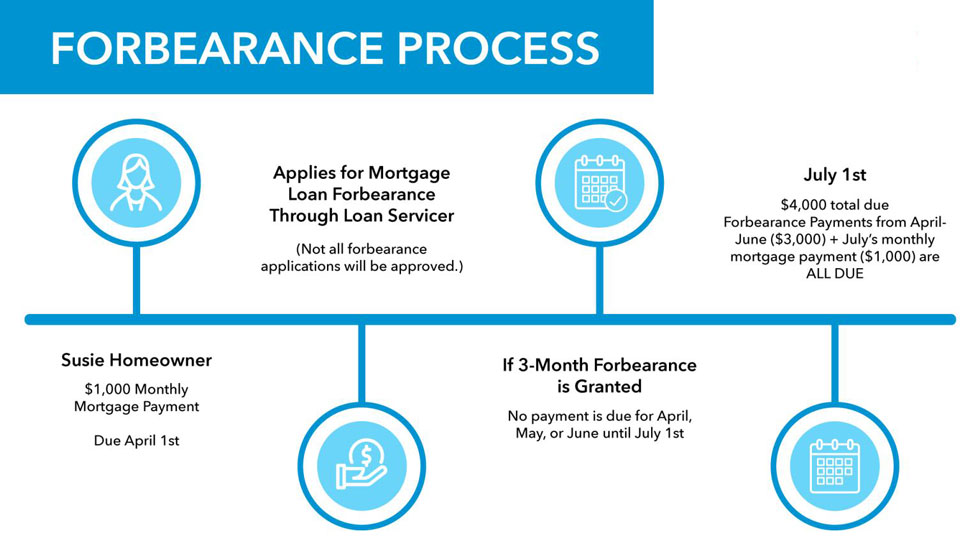

The application process typically involves:

- Contacting Your Lender: The first step is always to reach out to your mortgage servicer. Many lenders have dedicated departments or online portals for forbearance requests.

- Submitting Documentation: You will likely need to provide documentation to support your claim of financial hardship.

- Completing a Forbearance Request Form: This form will outline the terms of the forbearance, including the duration and repayment options.

- Receiving Approval: Once reviewed, the lender will inform you whether your request has been approved and the specific terms of the agreement.

Key Aspects and Considerations of Mortgage Forbearance

Once a forbearance agreement is in place, it’s vital to understand its implications and how payments will eventually be addressed. Forbearance is not a magic wand that erases debt; it merely postpones it.

Duration and Extension of Forbearance

Forbearance periods are not indefinite. They are typically granted for a set duration, often ranging from three to twelve months. The initial period is agreed upon at the outset, and in some cases, extensions may be possible, especially if the hardship is ongoing.

- Initial Forbearance Period: This is the initial timeframe agreed upon by both the borrower and the lender. It’s designed to provide immediate relief.

- Requesting Extensions: If your financial hardship persists beyond the initial forbearance period, you can typically request an extension. This usually requires a renewed demonstration of hardship and a discussion with your lender about continued relief. However, there are often limits to the total duration of forbearance allowed.

Repayment Options After Forbearance

This is arguably the most critical aspect of forbearance. When the forbearance period ends, the missed payments do not simply disappear. Lenders are required to offer various repayment options to help borrowers catch up. The specific option offered can depend on the loan type, lender policies, and the borrower’s ability to repay. Common repayment methods include:

- Repayment Plan: This involves adding a portion of the missed payments to your regular monthly payments over a set period. For example, if you missed three months of payments, you might pay your regular principal and interest, plus an additional amount spread over the next 6, 12, or even 24 months.

- Lump Sum Payment: In some less common scenarios, you might be required to pay all the missed payments in a single lump sum at the end of the forbearance period. This is typically only feasible if the borrower’s financial situation has significantly improved.

- Loan Modification: In cases where a borrower’s financial hardship is likely to be long-term, a loan modification may be an option. This permanently changes the terms of the loan, potentially by extending the loan term, reducing the interest rate, or even forgiving a portion of the principal balance. This is a more complex process than a simple repayment plan.

- Deferred Payment (Balloon Payment): Some forbearance agreements may allow you to defer the missed payments to the end of your loan term. This means your regular payments will continue, but when the loan matures, you’ll owe the accumulated missed payments as a large, final “balloon” payment. This option is less common and can be risky if you don’t anticipate having the funds available then.

It is imperative to thoroughly discuss these options with your lender and choose the one that best aligns with your financial capabilities. Failure to do so could still lead to serious consequences.

Understanding the Impact and Alternatives to Forbearance

While forbearance is a valuable tool, it’s essential to consider its potential impact on your financial future and to be aware of alternative solutions.

Impact on Credit Score and Future Borrowing

The impact of forbearance on your credit score can be nuanced. If your forbearance agreement is properly reported to credit bureaus as such, it generally has a less detrimental effect than missed payments or a foreclosure. However, it will still be noted on your credit report.

- Reporting to Credit Bureaus: Lenders are typically required to report forbearance to credit bureaus. The exact reporting can vary, but it may be marked as “current” or with a specific notation indicating the forbearance.

- Future Borrowing: While a forbearance can temporarily affect your creditworthiness, a properly managed forbearance that leads to a successful repayment plan or loan modification is generally viewed more favorably than a foreclosure. However, it can still make it more challenging to obtain new credit, such as a car loan or a new mortgage, in the short term. Lenders will look at your repayment history after forbearance to assess your reliability.

Alternatives to Forbearance

Forbearance isn’t the only option available when facing financial difficulties. Depending on your situation, other avenues might be more suitable:

- Loan Modification: As mentioned earlier, this is a permanent change to your loan terms. It’s ideal for borrowers facing long-term financial hardship who cannot realistically repay the missed payments.

- Refinancing: If interest rates have dropped significantly since you took out your mortgage, or if you can qualify for better terms, refinancing might lower your monthly payments. However, this requires a good credit score and stable income.

- Selling Your Home: In extreme cases where you cannot afford your mortgage payments even with forbearance or modification, selling your home might be the most responsible option to avoid foreclosure and preserve some equity.

- Hardship Programs: Some lenders and government agencies offer specific hardship programs beyond standard forbearance. These might include temporary interest-only payments or other tailored solutions.

- Financial Counseling: Non-profit credit counseling agencies can provide invaluable assistance. They can help you assess your financial situation, negotiate with creditors, and develop a budget and repayment plan.

In conclusion, mortgage forbearance is a vital safety net for homeowners in distress. It offers a temporary pause in payments, providing critical time to recover from financial setbacks and avoid foreclosure. However, it is not a debt cancellation. Understanding the terms, repayment obligations, and available alternatives is crucial for navigating this process successfully and securing your financial future. Proactive communication with your lender is the most important step when financial challenges arise.