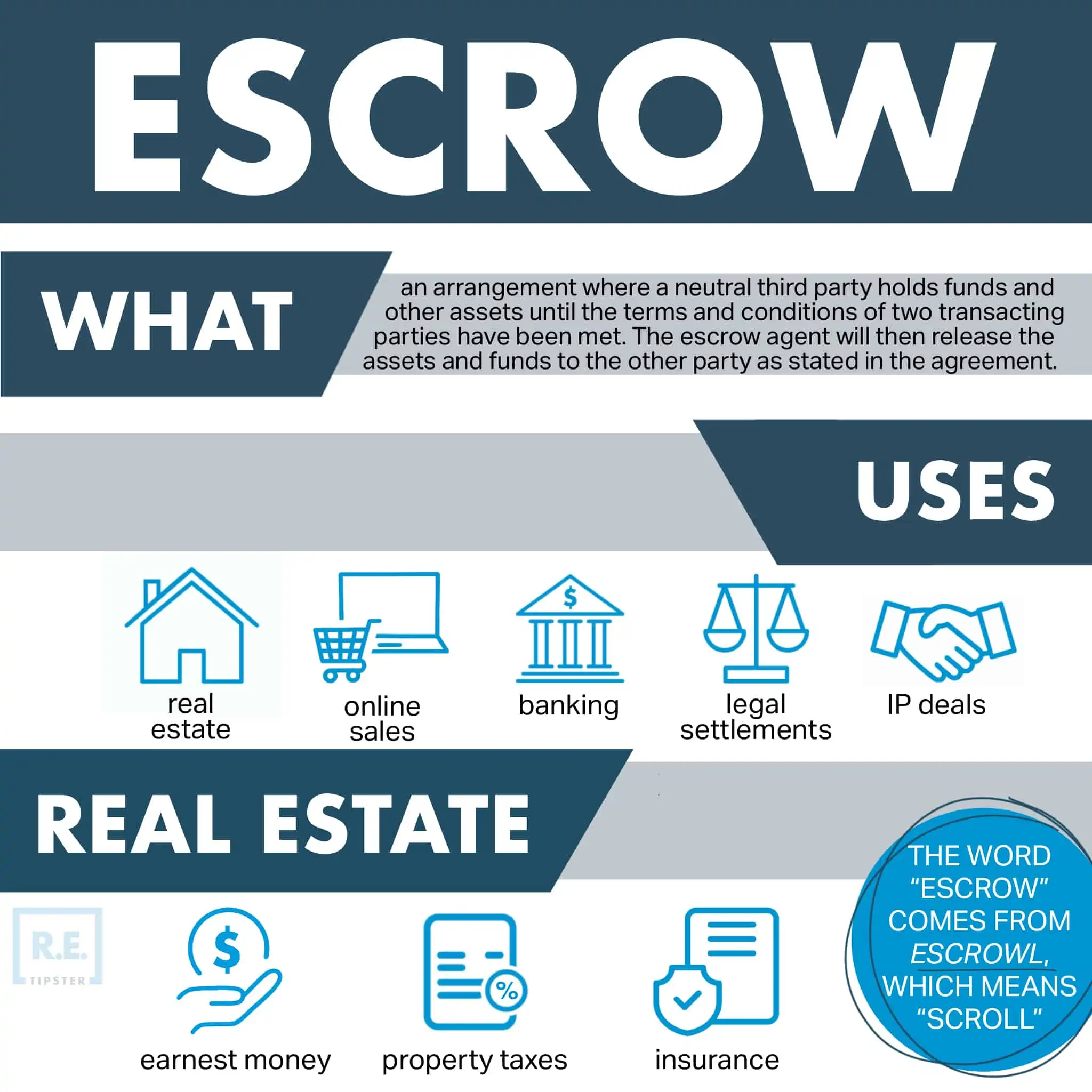

Escrow, in the context of a mortgage, is a crucial financial arrangement that safeguards both the borrower and the lender by holding funds and documents in trust until specific conditions are met. It acts as an impartial third party, facilitating the complex transaction of a home purchase or refinance. Understanding the mechanics of escrow is vital for any homeowner, as it directly impacts the management of their property taxes, homeowner’s insurance, and potentially other vital payments associated with their mortgage.

The Role of the Escrow Holder

The escrow holder, often a specialized escrow company, a title company, or sometimes an attorney, plays a pivotal role in ensuring a smooth and secure real estate transaction. Their primary function is to act as a neutral intermediary, receiving and disbursing funds and important documents from all parties involved in the transaction – the buyer, the seller, the lender, and even potentially government entities.

Holding Funds and Documents

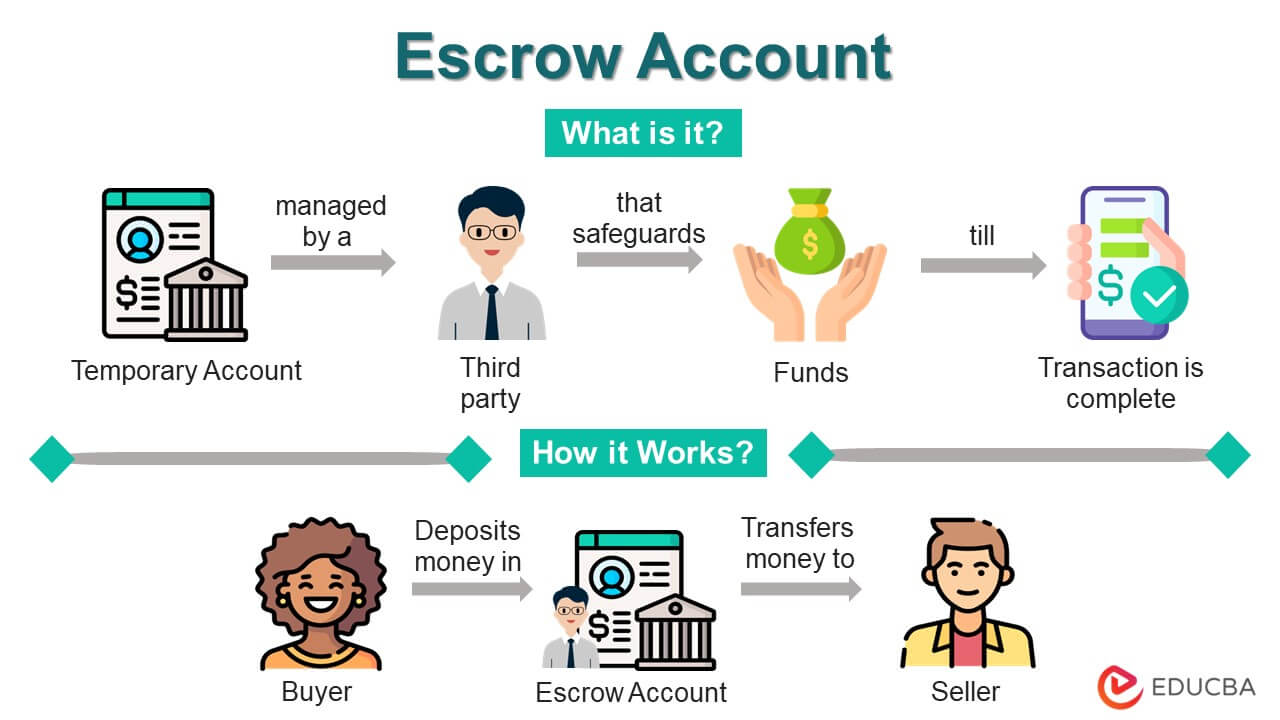

At the outset of a real estate transaction, the buyer typically deposits earnest money, which is a deposit showing their serious intent to purchase. This money is held securely in an escrow account. As the transaction progresses, the buyer will also deposit the remaining portion of their down payment and closing costs into this account. Similarly, the lender will deposit the mortgage funds. All these funds are held by the escrow holder until all the conditions of the sale or refinance agreement have been satisfied.

Beyond funds, the escrow holder also manages critical documents. This can include the signed purchase agreement, loan documents, title insurance policies, deeds, and other legal paperwork. The escrow holder ensures that all parties sign and deliver these documents as required by the contract and the lender.

Facilitating Closing

The ultimate goal of the escrow process is to facilitate a successful closing. Once all contingencies have been met (such as satisfactory home inspections, appraisals, and loan approvals), the escrow holder meticulously reviews all the paperwork and funds. They then proceed to disburse the funds according to the instructions of the buyer, seller, and lender. This includes paying off existing mortgages for the seller, transferring title to the buyer, paying real estate agent commissions, and covering other associated closing costs.

The escrow holder also ensures that all necessary documents are recorded with the appropriate government agencies, officially transferring ownership of the property. This impartial oversight by the escrow holder provides a level of security and certainty that is essential for large financial transactions like buying a home. Without escrow, parties would have to directly exchange large sums of money and sensitive documents, creating significant risk and potential for fraud.

Escrow Accounts for Ongoing Mortgage Payments

Beyond the initial closing, the term “escrow” commonly refers to an account managed by the mortgage lender or a designated loan servicer for ongoing property-related expenses. This is known as an “escrow account” or “impound account.” When you take out a mortgage, your lender often requires you to fund this account to ensure that crucial payments, like property taxes and homeowner’s insurance, are made on time.

Purpose of the Escrow Account

The primary purpose of an escrow account is to protect the lender’s investment. By collecting a portion of these payments each month as part of your mortgage payment, the lender ensures that the property remains adequately insured and that property taxes are paid, preventing potential liens or foreclosures that could jeopardize their collateral.

How the Escrow Account Works

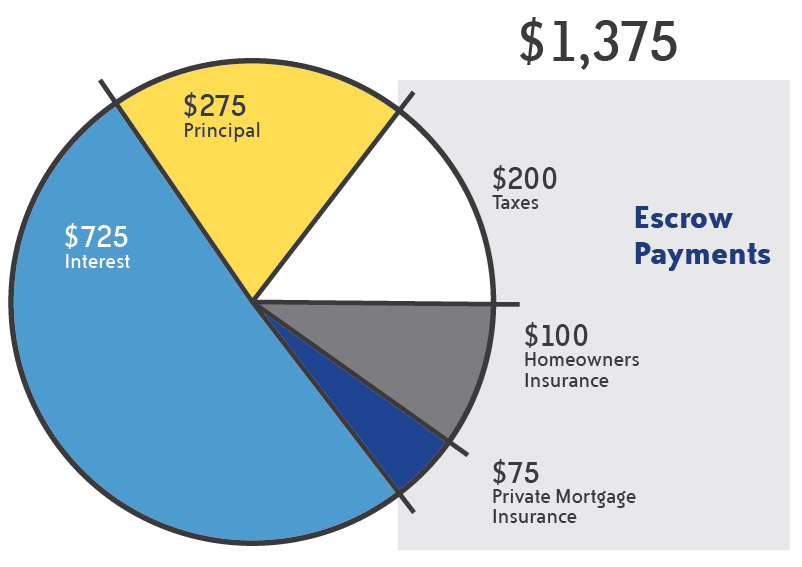

Each month, a portion of your total mortgage payment goes into your escrow account. This amount is typically calculated by taking the total annual cost of your property taxes and homeowner’s insurance, dividing it by twelve, and adding a small buffer (usually a two-month cushion) to ensure there are always sufficient funds.

For example, if your annual property taxes are $3,600 and your annual homeowner’s insurance premium is $1,200, the total annual cost is $4,800. Divided by twelve, this is $400 per month. Your lender might add a buffer, so your monthly escrow payment could be around $800 (the $400 for taxes and insurance, plus a $400 buffer).

Disbursements from the Escrow Account

When your property tax bills or homeowner’s insurance premiums become due, the lender or loan servicer will pay these bills directly from your escrow account. They will typically notify you in advance of these payments. This automated system ensures that these critical payments are not missed, which could lead to late fees, increased insurance premiums, or even a tax lien on your property.

Escrow Analysis

Lenders are required by law to perform an escrow analysis at least once a year. This analysis reviews the projected payments for the upcoming year against the actual amount in the escrow account. If there’s a shortfall (meaning the projected payments exceed the current balance plus the buffer), your monthly escrow payment will likely increase to make up the difference. Conversely, if there’s a surplus, your payment might decrease, or the excess funds may be returned to you.

Benefits of Using Escrow

The escrow system, whether for closing or ongoing payments, offers significant benefits to all parties involved in a mortgage transaction.

For Buyers

- Security and Protection: Escrow provides a secure environment for depositing funds and sensitive documents, minimizing the risk of fraud or mishandling. Buyers can be confident that their money will only be released once all contractual obligations are met.

- Reduced Stress: The escrow holder manages the complex process of coordinating with all parties, ensuring deadlines are met, and that all paperwork is in order, thereby reducing stress for the buyer.

- Peace of Mind: Knowing that essential payments like property taxes and homeowner’s insurance are being managed reliably through an escrow account offers significant peace of mind.

For Sellers

- Guaranteed Payment: Sellers are assured that they will receive the agreed-upon sale price once all conditions are met. The escrow holder ensures that the buyer has secured the necessary funds.

- Clean Transaction: The escrow holder handles the payoff of any existing liens or mortgages on the property, ensuring a clear title is transferred to the buyer.

- Professional Management: Sellers benefit from the professional management of the closing process, avoiding direct disputes or complications with the buyer.

For Lenders

- Collateral Protection: For ongoing mortgage payments, the escrow account is crucial for protecting the lender’s interest in the property. Timely payment of property taxes and homeowner’s insurance ensures the property is free from liens and adequately insured, maintaining its value as collateral.

- Reduced Risk: The escrow system reduces the lender’s risk of financial loss due to non-payment of these critical expenses by the borrower.

When Escrow Might Not Be Required

While escrow accounts for ongoing payments are common, they are not always mandatory. In some cases, particularly with larger down payments or strong credit histories, lenders may allow borrowers to opt out of an escrow account. This means the borrower would be responsible for directly managing and paying their property taxes and homeowner’s insurance bills.

Pros of Waiving Escrow

- Control: Borrowers have direct control over their funds and can choose their own payment schedules for taxes and insurance.

- Potential for Higher Returns: If a borrower is disciplined, they could potentially earn higher interest on the funds they would have otherwise placed in an escrow account.

Cons of Waiving Escrow

- Increased Responsibility: The borrower assumes the full responsibility for tracking payment due dates and ensuring timely payments. Forgetting a payment can lead to severe consequences.

- Risk of Missed Payments: The risk of accidentally missing a tax or insurance payment is higher for individuals who are not accustomed to managing these expenses directly.

- Potential for Higher Insurance Premiums: Some insurance companies may offer slightly lower premiums to borrowers who have their mortgage payments and insurance handled through an escrow account, as it reduces the insurer’s risk.

- Higher Interest Rates: In some instances, lenders might charge a slightly higher interest rate on the mortgage if the borrower opts out of escrow, as it represents a higher risk for the lender.

Conclusion

Escrow is an indispensable component of the mortgage process, offering a secure and structured framework for both the initial closing of a home purchase and the ongoing management of property-related expenses. Whether it’s the neutral holding of funds and documents during a transaction or the proactive collection and disbursement for taxes and insurance, the escrow system provides vital protection and peace of mind for buyers, sellers, and lenders alike. While the option to waive an escrow account for ongoing payments exists, its benefits in terms of financial discipline and risk mitigation often make it a wise and preferred choice for homeowners. Understanding the intricacies of escrow empowers individuals to navigate their homeownership journey with greater confidence and security.