The 1099-R, officially known as the “Distributions From Pensions, Annuities, Retirement or Profit-Sharing Plans, IRAs, Insurance Contracts, etc.,” is a crucial tax form that reports distributions from various retirement accounts and insurance products. Understanding the codes used on this form is vital for accurate tax filing. Among the various distribution codes, Code 7 holds a specific and important meaning that directly impacts how a distribution is treated for tax purposes. This article delves into the intricacies of Distribution Code 7 on a 1099-R, explaining its significance, implications, and how it relates to common retirement account withdrawals.

Understanding Distribution Code 7: Direct Rollover

Distribution Code 7 on a 1099-R signifies a direct rollover of a retirement plan distribution. In simpler terms, it indicates that funds were moved directly from one eligible retirement account to another, without the funds ever passing through the hands of the account holder. This is a common and advantageous strategy for individuals who are changing employers, consolidating retirement accounts, or seeking to adjust their investment strategy.

The core principle behind a direct rollover is to preserve the tax-deferred status of the retirement funds. When you take a distribution from a retirement account and it’s not rolled over within the specified timeframe, it’s generally considered a taxable event. This means you might owe income tax on the withdrawn amount in the year of distribution, and if you are under age 59½, you could also face a 10% early withdrawal penalty. A direct rollover bypasses these immediate tax consequences.

The Mechanics of a Direct Rollover

A direct rollover can occur in several scenarios. The most common is when an employee leaves a job and has funds in a 401(k), 403(b), or other employer-sponsored retirement plan. Instead of cashing out the account, which would trigger taxes and penalties, the employee can instruct their former employer’s plan administrator to send the funds directly to an IRA or a new employer’s retirement plan.

The process typically involves the following steps:

- Initiation: The account holder contacts the administrator of their current retirement plan and requests a direct rollover. They will need to provide information about the destination account, including the financial institution’s name, address, and account number.

- Transfer: The administrator of the distributing plan then directly sends the funds to the custodian of the receiving account. This transfer can be done via check or electronic funds transfer (EFT).

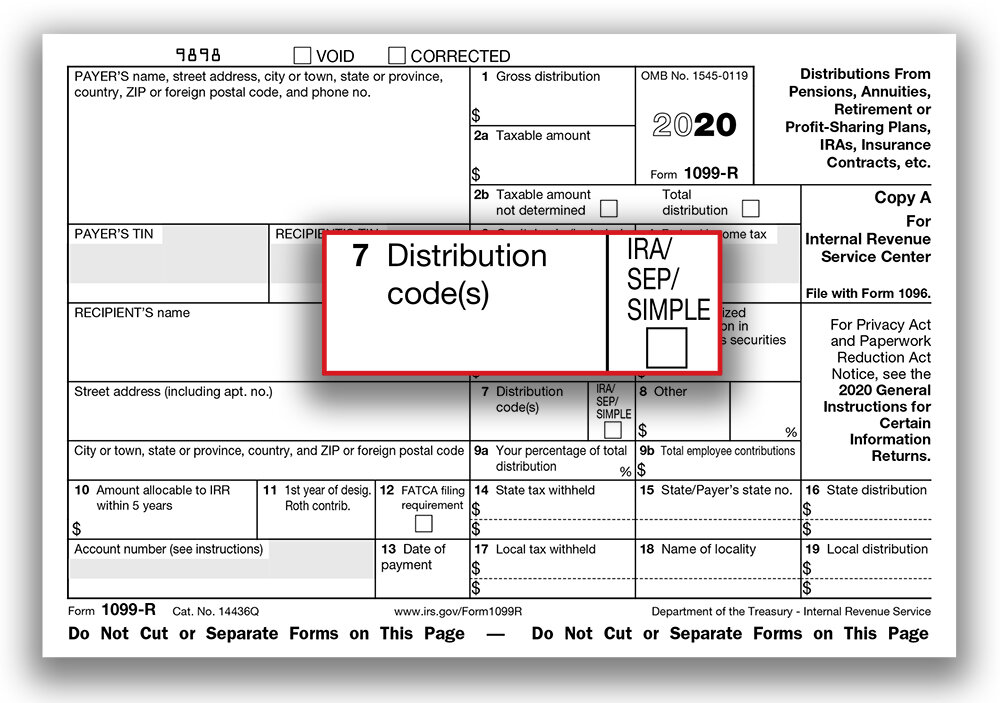

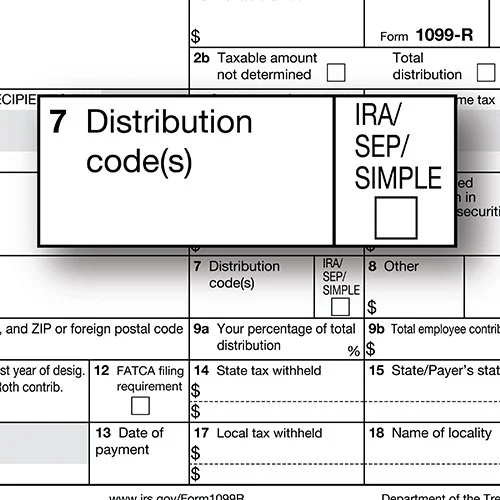

- Reporting: The distributing institution is required to issue a 1099-R to the account holder, with Distribution Code 7 entered in Box 7. This code informs the IRS that the distribution was a direct rollover and therefore should not be treated as a taxable withdrawal.

Benefits of Direct Rollover (Code 7)

The primary benefit of utilizing a direct rollover, and thus receiving a 1099-R with Code 7, is the deferral of taxes. By moving the funds directly, you avoid the immediate tax liability that would arise from an indirect rollover or a cash distribution. This allows your retirement savings to continue growing on a tax-deferred basis, maximizing your long-term wealth accumulation.

Beyond tax deferral, direct rollovers offer several other advantages:

- Avoiding the 10% Early Withdrawal Penalty: If you are under the age of 59½, a direct rollover ensures you avoid the 10% penalty on early withdrawals from retirement accounts. This can be a substantial saving, as the penalty applies to the entire amount withdrawn if not rolled over properly.

- Maintaining Investment Momentum: A direct rollover allows you to maintain continuity in your investment strategy. You can move your funds to an account where you have greater control over investment choices or to an account that better aligns with your current financial goals and risk tolerance.

- Consolidation of Assets: For individuals with multiple retirement accounts from previous employers, direct rollovers provide an excellent opportunity to consolidate these assets into a single IRA or a current employer’s plan. This simplifies account management, makes it easier to track performance, and can potentially reduce fees.

- Preserving Retirement Account Options: Certain retirement plans, like qualified employer-sponsored plans, may offer unique features or investment options not available in an IRA. Conversely, IRAs often provide a wider array of investment choices. A direct rollover allows you to move your funds to the account type that best suits your needs.

Distinguishing Code 7 from Other Rollover Codes

It is crucial to understand that while Code 7 signifies a direct rollover, other codes on the 1099-R pertain to different types of distributions, including other rollover scenarios. The most important distinction is between a direct rollover (Code 7) and an indirect rollover.

Indirect Rollover (Code G)

An indirect rollover occurs when a distribution is made payable to the account holder, who then has 60 days to deposit those funds into another eligible retirement account. If the full amount is rolled over within this 60-day window, it is treated similarly to a direct rollover, with taxes deferred. However, the 1099-R for an indirect rollover will typically have Distribution Code G in Box 7.

The key difference and potential pitfall of an indirect rollover is that the distributing institution is usually required to withhold 20% of the distribution for federal income tax purposes. This withholding is a mandatory step, even though the entire distribution might ultimately be rolled over. If the account holder fails to roll over the full amount (including the withheld 20%), they will owe income tax and potentially the 10% penalty on the portion not rolled over. To avoid this, the account holder must make up the 20% withholding from their own funds when rolling over the distribution.

Example: If you receive a $10,000 distribution that you intend to roll over indirectly, the administrator will send you $8,000 and withhold $2,000. To complete a full rollover and defer taxes on the entire $10,000, you must deposit $10,000 into your new account. This means you would need to add $2,000 from your personal funds to cover the withheld amount. When you file your taxes, you would then claim a credit for the $2,000 withholding.

Why Code 7 is Preferred

Given the mandatory withholding associated with indirect rollovers, Distribution Code 7 (direct rollover) is generally the preferred method for moving retirement funds. It eliminates the immediate concern of the 20% withholding and the need to supplement the rollover amount from other sources. The funds are transferred seamlessly between custodians, ensuring the entire eligible amount continues to grow tax-deferred without interruption or immediate tax implications.

Reporting a Code 7 Distribution on Your Tax Return

When you receive a 1099-R with Distribution Code 7, it signifies that the distribution itself is not taxable. However, it still needs to be reported on your tax return. The IRS uses this information to track retirement account activity and ensure that rollovers are completed correctly.

Filing with Form 1040

Typically, you will report the distribution on Form 1040, Schedule 1 (Form 1040), Additional Income and Adjustments to Income. You will enter the taxable amount (which for a direct rollover is $0) and any withheld tax in the appropriate lines. Crucially, you will then take an “Other Income” deduction on Schedule 1 for the same amount that was rolled over. This deduction effectively offsets the initial distribution, resulting in a net taxable amount of zero for that distribution.

For example, if your 1099-R shows a total distribution of $50,000 with Code 7, you would report the $50,000 on the relevant lines indicating a distribution received. Then, in the “Adjustments to Income” section of Schedule 1, you would claim an adjustment (a rollover deduction) of $50,000, bringing your taxable income for that distribution back down to zero.

Importance of Documentation

It is imperative to maintain thorough documentation of your direct rollover. This includes:

- The 1099-R form: Keep this form with your tax records.

- Rollover confirmation statements: The statements from both the distributing and receiving institutions will provide details of the transfer, including dates and amounts.

- Any correspondence with plan administrators: This can be helpful if any questions arise.

Accurate record-keeping ensures that you can easily substantiate your rollover when filing your taxes and provides a reference in case of an IRS inquiry.

Common Scenarios Leading to a Code 7 Distribution

Several life events and financial planning decisions can lead to a 1099-R with Distribution Code 7:

- Changing Employers: As mentioned earlier, when you leave a job, you can directly roll over your 401(k) or other employer-sponsored plan into an IRA or your new employer’s plan.

- Consolidating IRAs: If you have multiple IRAs from different financial institutions or from past rollovers, you can consolidate them into a single IRA through a direct rollover. This simplifies management and can potentially lower fees.

- Inheriting an IRA: While not always a direct rollover in the traditional sense, beneficiaries inheriting retirement accounts often have options to move the inherited funds into an inherited IRA, which can involve a direct transfer process.

- Moving Funds Between Retirement Account Types: You might decide to move funds from an employer-sponsored plan to an IRA for greater investment flexibility or vice-versa.

- Age 59½ and Beyond: Even after reaching retirement age, individuals may choose to roll over funds for various reasons, such as consolidating assets or changing investment providers.

Conclusion

Distribution Code 7 on a 1099-R is a clear indicator that retirement funds have been transferred directly from one eligible account to another. This process is designed to preserve the tax-deferred status of those funds, allowing them to continue growing without immediate taxation or penalties. Understanding the implications of Code 7 is essential for every individual who manages retirement accounts. By opting for direct rollovers whenever possible, individuals can effectively manage their retirement savings, maximize their long-term investment growth, and ensure a smoother and more advantageous retirement planning journey. Always consult with a tax professional or financial advisor to navigate specific situations and ensure accurate tax reporting.