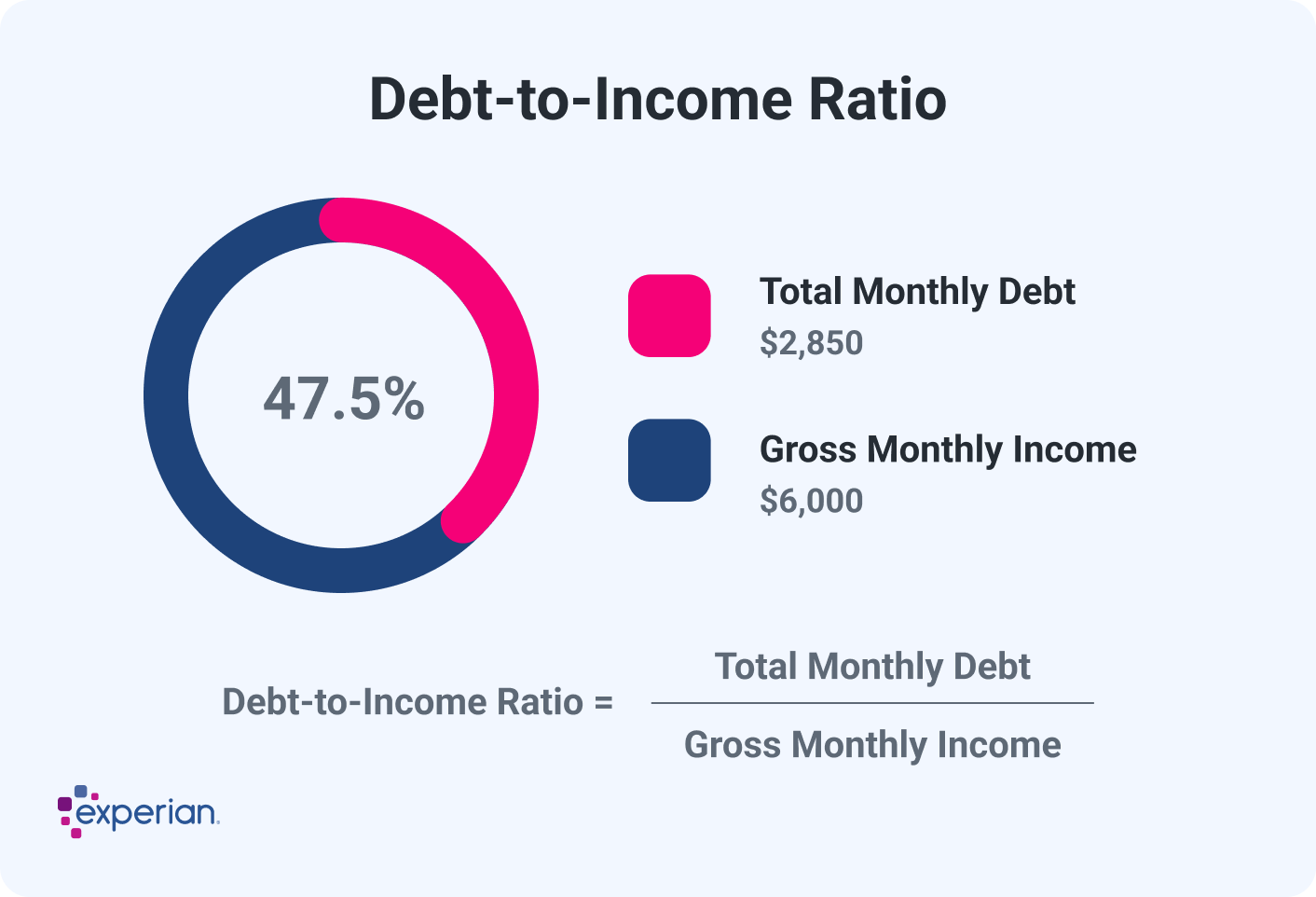

The debt-to-income (DTI) ratio is a fundamental financial metric that lenders use to assess a borrower’s ability to manage monthly debt payments and repay loans. It essentially compares your total monthly debt obligations to your gross monthly income. In simpler terms, it tells lenders how much of your pre-tax income is already committed to paying off debts. Understanding your DTI is crucial not only for securing new credit, such as mortgages or auto loans, but also for managing your personal finances effectively and ensuring long-term financial health.

Financial institutions, particularly mortgage lenders, heavily rely on the DTI ratio as a key indicator of risk. A lower DTI generally signifies a borrower who has more disposable income and is therefore considered a lower risk for default. Conversely, a high DTI suggests that a significant portion of your income is already allocated to debt, potentially leaving you with less flexibility to handle unexpected expenses or to manage new debt obligations. This can significantly impact your ability to qualify for loans or to secure favorable interest rates.

The Mechanics of Calculating Your Debt-to-Income Ratio

Calculating your debt-to-income ratio is a straightforward process, but it requires careful attention to detail to ensure accuracy. Lenders typically look at two types of DTI: the front-end ratio (also known as the housing ratio) and the back-end ratio (also known as the total debt ratio). While both are important, the back-end DTI is generally considered more comprehensive and is the one most commonly referenced when discussing loan eligibility.

Front-End Debt-to-Income Ratio (Housing Ratio)

The front-end DTI, often referred to as the housing ratio or the mortgage ratio, focuses exclusively on the proposed housing expenses as a percentage of your gross monthly income. This ratio is particularly important for mortgage lenders as it gives them a clear picture of how much of your income will be dedicated to housing costs if you take out a new mortgage.

Calculation:

The formula for the front-end DTI is:

(Proposed Monthly Housing Expenses / Gross Monthly Income) * 100 = Front-End DTI (%)

Components of Monthly Housing Expenses:

- Principal and Interest (P&I): This is the core payment for the loan used to purchase your home.

- Property Taxes: The annual property taxes, divided by 12 to get the monthly amount.

- Homeowner’s Insurance: The annual cost of homeowner’s insurance, divided by 12.

- Private Mortgage Insurance (PMI) or FHA Mortgage Insurance Premium (MIP): If you have less than 20% down payment on a conventional loan, you’ll likely pay PMI. For FHA loans, there’s an upfront and annual MIP.

- Homeowner’s Association (HOA) Dues: If applicable, the monthly cost of HOA fees.

Example:

Let’s say your gross monthly income is $6,000. Your estimated monthly housing expenses (P&I, taxes, insurance, PMI) are $1,500.

Front-End DTI = ($1,500 / $6,000) * 100 = 25%

A 25% front-end DTI would generally be considered favorable by lenders.

Back-End Debt-to-Income Ratio (Total Debt Ratio)

The back-end DTI, or total debt ratio, provides a more holistic view of your financial obligations. It includes all of your monthly debt payments, including housing expenses, plus all other recurring monthly debts. This is the ratio lenders most often focus on because it reflects your overall debt burden and your capacity to handle additional financial commitments.

Calculation:

The formula for the back-end DTI is:

(Total Monthly Debt Payments / Gross Monthly Income) * 100 = Back-End DTI (%)

Components of Total Monthly Debt Payments:

- All Front-End DTI Components: This includes your proposed monthly housing expenses as calculated above.

- Credit Card Minimum Payments: The minimum amount you’re required to pay each month on all your credit cards. Lenders often use the listed minimum, not what you actually pay.

- Student Loan Payments: The minimum monthly payment for any outstanding student loans.

- Auto Loan Payments: The monthly payment for any car loans.

- Personal Loan Payments: Monthly payments for any unsecured personal loans.

- Alimony or Child Support Payments: Court-ordered payments you are obligated to make.

- Other Installment Loans: Payments on any other loans that are repaid over a fixed period with regular installments.

Important Note on Included Debts: Lenders typically consider debts that will continue for at least 10 months after the loan closing date. For example, if you have a car loan that will be paid off in 8 months, it might not be included in the DTI calculation for a mortgage. However, it’s always best to clarify with your lender.

Example:

Continuing with the previous example, let’s say your gross monthly income is $6,000, and your front-end DTI components amount to $1,500.

Now, let’s add other monthly debt payments:

- Minimum credit card payments: $200

- Auto loan payment: $400

- Student loan payment: $300

Total Monthly Debt Payments = $1,500 (housing) + $200 (credit cards) + $400 (auto loan) + $300 (student loan) = $2,400

Back-End DTI = ($2,400 / $6,000) * 100 = 40%

A 40% back-end DTI is a common threshold, with many lenders having different guidelines for approval.

Understanding What Lenders Look For in Your DTI

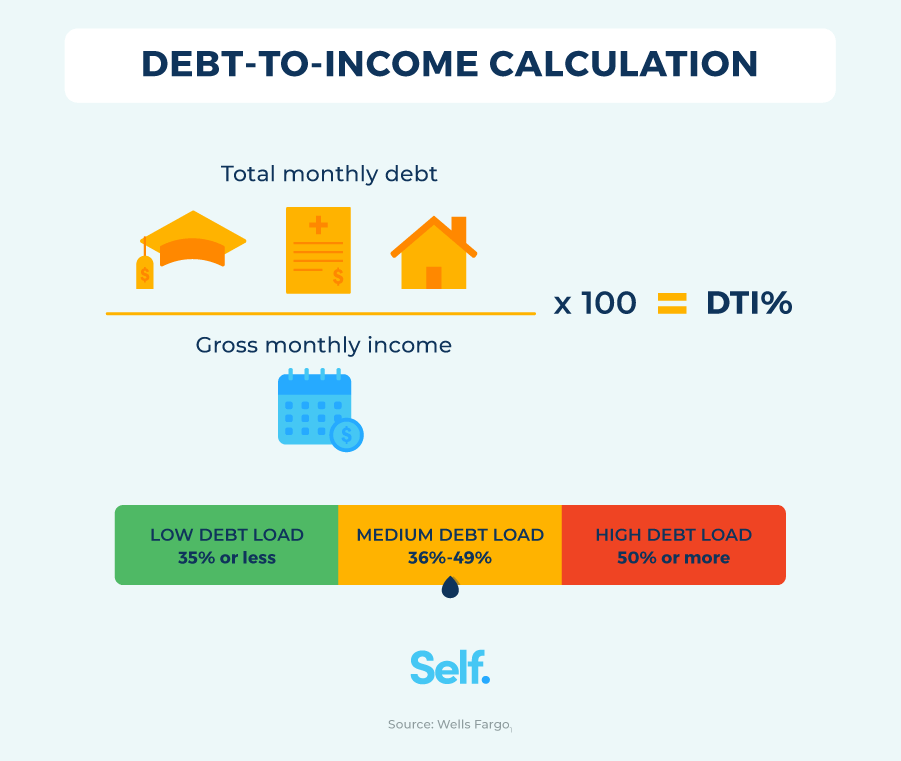

Lenders use the debt-to-income ratio as a primary tool to gauge your financial stability and your ability to handle new debt. While the exact thresholds can vary significantly between lenders and depend on the type of loan, there are general ranges that are commonly accepted. It’s important to remember that DTI is just one piece of the puzzle; lenders also consider your credit score, employment history, assets, and the loan-to-value ratio for secured loans.

Acceptable DTI Ranges and Lender Guidelines

Lenders typically categorize DTI ratios into several tiers, each associated with different levels of risk and loan approval likelihood.

-

Lower than 36%: This is generally considered an excellent DTI ratio. Borrowers with DTIs in this range are viewed as financially responsible and have a high likelihood of loan approval, often with competitive interest rates. This indicates that a substantial portion of your income is available for discretionary spending and savings after debt obligations are met.

-

36% to 43%: This range is often considered the acceptable limit for many mortgage lenders. While you might still qualify for a loan, your options may be more limited, and interest rates could be slightly higher than for those with lower DTIs. Lenders will scrutinize your application more closely in this range, looking for other positive financial indicators.

-

44% to 49%: This is a higher DTI range, and qualifying for a loan can become significantly more challenging. Many lenders will automatically deny applications with DTIs in this bracket, or they will require very strong compensating factors, such as a large down payment, excellent credit history, or substantial reserves.

-

50% or higher: A DTI of 50% or above is typically considered very high and indicates a significant financial strain. Borrowers in this situation are generally not considered eligible for new loans, especially mortgages, as they are perceived to have a very high risk of default.

Important Considerations:

- Loan Type: Different loan products have different DTI requirements. For example, FHA loans may allow for higher DTIs than conventional mortgages.

- Lender Specifics: Each lender has its own underwriting guidelines. Some may be more conservative, while others might be more flexible.

- Compensating Factors: Even with a slightly higher DTI, strong credit scores, significant savings, a stable job history, or a large down payment can sometimes help you overcome a less-than-ideal DTI.

The Impact of DTI on Loan Approval and Interest Rates

Your debt-to-income ratio has a direct and significant impact on your ability to obtain credit and the cost of that credit.

-

Loan Approval: As outlined above, a lower DTI significantly increases your chances of loan approval. Lenders see a lower DTI as a sign of financial discipline and a reduced risk of default. A high DTI, conversely, can be an immediate disqualifier for many loan products.

-

Interest Rates: Even if you qualify for a loan with a higher DTI, you may be offered less favorable interest rates. Lenders charge higher interest rates to borrowers they perceive as higher risk to compensate for that increased risk. A lower DTI signals to lenders that you are in a stronger financial position, making you a more attractive borrower, and thus eligible for lower interest rates. This can translate into substantial savings over the life of a loan, especially for long-term debts like mortgages.

-

Loan Amount: Your DTI can also influence the maximum loan amount you can qualify for. Lenders will not approve a loan that pushes your DTI beyond their acceptable limits, even if you have a good credit score. This means a high DTI could limit your purchasing power for a home or the amount you can borrow for other significant purchases.

Strategies for Improving Your Debt-to-Income Ratio

If your current debt-to-income ratio is higher than you’d like, or if you’re concerned about its impact on future borrowing, there are several effective strategies you can employ to improve it. These strategies generally involve either increasing your income or decreasing your debt obligations.

Decreasing Your Monthly Debt Obligations

Reducing your monthly debt payments is often the most direct way to lower your DTI. This requires a concerted effort to tackle your existing debts.

- Pay Down Existing Debts: Focus on aggressively paying down debts with higher interest rates or those that will be paid off sooner. Consider the “debt snowball” or “debt avalanche” methods.

- Debt Snowball: Pay the minimum on all debts except the smallest one, which you attack with extra payments. Once it’s paid off, add that payment to the next smallest debt. This provides psychological wins.

- Debt Avalanche: Pay the minimum on all debts except the one with the highest interest rate, which you attack with extra payments. This saves the most money on interest over time.

- Consolidate or Refinance Debt: Look into options like debt consolidation loans or refinancing existing loans (e.g., mortgage refinance, auto loan refinance) to secure lower interest rates or extend payment terms. Be cautious, as extending terms can lower your monthly payment but increase the total interest paid.

- Avoid Taking on New Debt: While working to improve your DTI, refrain from taking on new loans or increasing credit card balances unless absolutely necessary.

- Negotiate with Creditors: In some cases, you may be able to negotiate lower interest rates or more manageable payment plans with your creditors, especially if you’re experiencing financial hardship.

Increasing Your Gross Monthly Income

Boosting your income directly impacts your DTI ratio by increasing the denominator in the calculation.

- Seek a Raise or Promotion: If you’re employed, discuss opportunities for a salary increase or a promotion within your current company. Highlight your contributions and market value.

- Take on a Second Job or Side Hustle: Consider part-time work, freelance opportunities, or starting a small business that generates additional income. Even a few hundred extra dollars a month can make a difference.

- Sell Unused Assets: Liquidating assets you no longer need, such as electronics, furniture, or vehicles, can provide lump sums that can be used to pay down debt, thereby improving your DTI.

- Monetize Skills or Hobbies: Explore ways to earn money from your skills or hobbies, whether through teaching, crafting, or providing services.

By implementing a combination of these strategies, you can systematically reduce your debt burden and/or increase your income, leading to a healthier debt-to-income ratio. This not only improves your chances of securing future loans but also provides greater financial flexibility and peace of mind.