The bedrock of all financial recording and reporting, from the simplest sole proprietorship to the most complex multinational corporation, lies in the fundamental principles of debit and credit. These two terms, often shrouded in a mystique that can deter newcomers, are not inherently complex. Instead, they represent a dual-entry system designed to meticulously track every financial transaction. Understanding debit and credit is paramount for anyone seeking to grasp the inner workings of accounting, financial statements, and ultimately, the economic health of a business.

The Double-Entry System: A Foundation of Balance

At its core, accounting operates on the principle of the double-entry system. This method dictates that every financial transaction affects at least two accounts. One account is debited, and another is credited. The fundamental accounting equation – Assets = Liabilities + Equity – is maintained through this system. When a transaction occurs, the total debits must always equal the total credits. This inherent balance provides an internal check, making it easier to detect errors and ensuring the integrity of the financial records.

Understanding the Accounting Equation

The accounting equation is the guiding principle for debit and credit entries.

- Assets: These are the resources owned by a company that have future economic value. Examples include cash, accounts receivable, inventory, property, and equipment.

- Liabilities: These represent obligations or debts that a company owes to external parties. Examples include accounts payable, salaries payable, notes payable, and bonds payable.

- Equity: This is the owners’ stake in the company. It represents the residual interest in the assets of an entity after deducting all its liabilities. Equity typically includes common stock, retained earnings, and additional paid-in capital.

The double-entry system ensures that this equation always remains in balance. If assets increase, either liabilities must also increase, or equity must increase. Conversely, if assets decrease, either liabilities must decrease, or equity must decrease.

The T-Account: A Visual Representation

The concept of debit and credit is often visualized using T-accounts. A T-account is a simple graphical representation of a single ledger account. It has a horizontal line representing the account balance and a vertical line dividing it into two sides: the left side (debit) and the right side (credit).

| Debit (Dr.) | Credit (Cr.) |

|---|---|

The side on which an increase is recorded depends on the type of account. This is where the nuances of debit and credit become critical.

The Mechanics of Debit and Credit: What They Mean

Debit and credit are not inherently “good” or “bad.” They are simply indicators of direction within the accounting equation. Their impact on an account’s balance depends on the nature of the account itself.

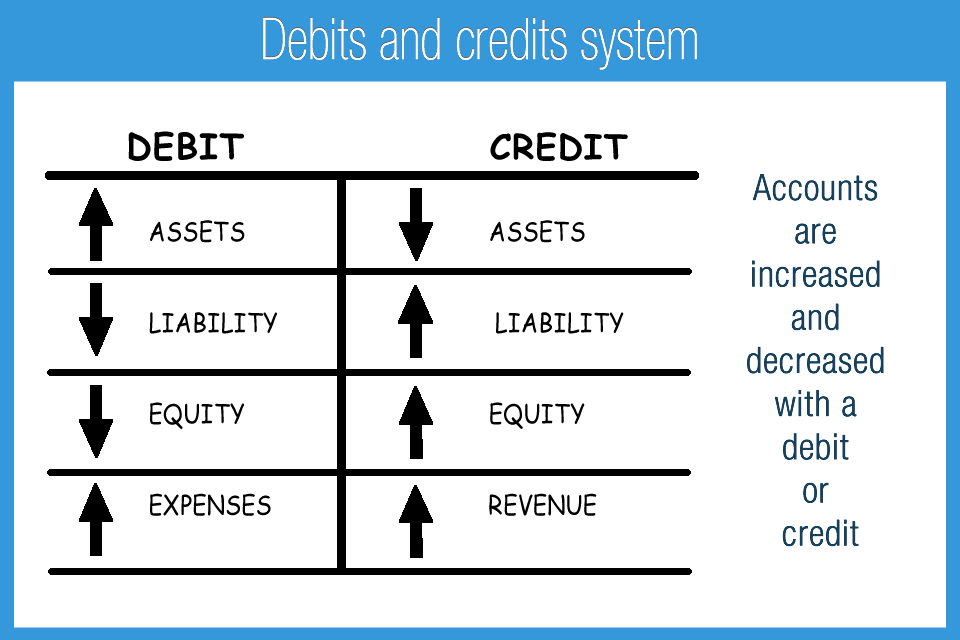

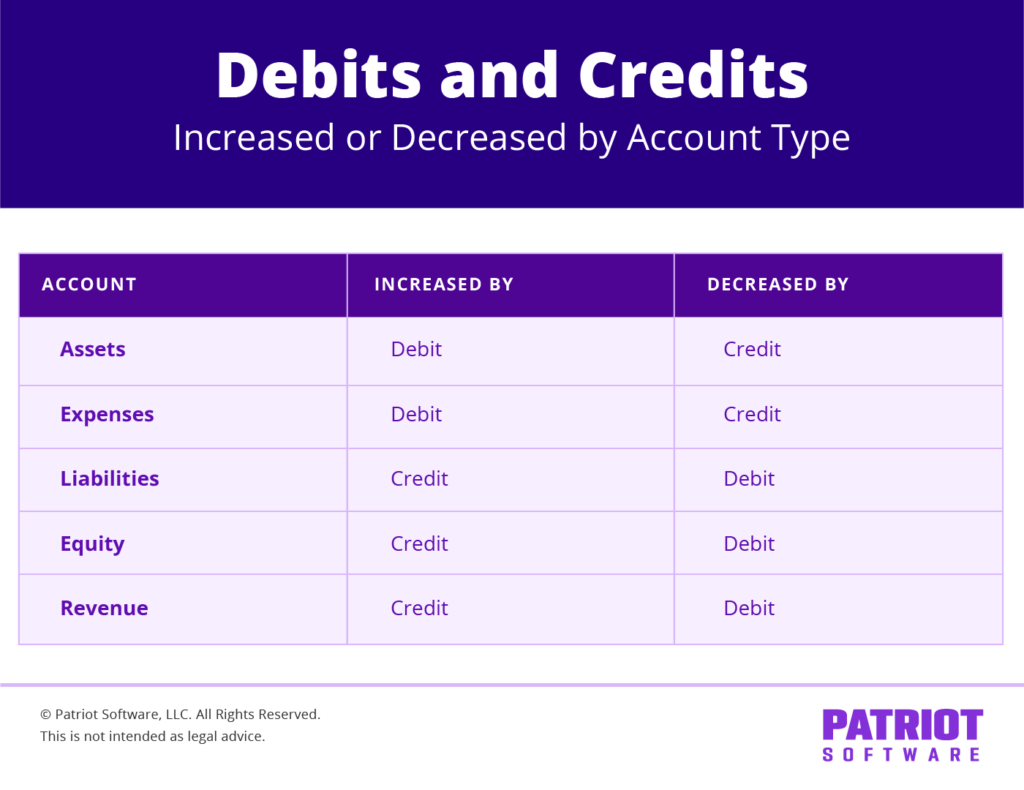

How Debits and Credits Affect Different Account Types

To understand how debits and credits work, we must categorize accounts based on their nature:

-

Assets:

- Debit: Increases an asset account. When a company receives cash, buys equipment, or its inventory grows, the corresponding asset accounts are debited.

- Credit: Decreases an asset account. When a company spends cash, sells inventory, or disposes of equipment, the asset accounts are credited.

-

Liabilities:

- Debit: Decreases a liability account. When a company pays off a debt or reduces an amount owed to a supplier, the corresponding liability accounts are debited.

- Credit: Increases a liability account. When a company takes out a loan, incurs a new debt, or owes more to its suppliers, the liability accounts are credited.

-

Equity:

- Debit: Decreases an equity account. This can happen through owner withdrawals (dividends or drawings), paying expenses that reduce profit (and thus retained earnings), or buybacks of company stock.

- Credit: Increases an equity account. This occurs through owner investments, profitable operations (increasing retained earnings), or issuing new stock.

The Role of Revenue and Expense Accounts

Revenue and expense accounts are often considered within the broader equity category, as they directly impact the company’s profit and, consequently, its retained earnings.

-

Revenue:

- Debit: Decreases a revenue account. This is less common but can occur with sales returns or allowances.

- Credit: Increases a revenue account. When a company earns income from sales or services, the revenue accounts are credited.

-

Expenses:

- Debit: Increases an expense account. When a company incurs costs such as salaries, rent, utilities, or marketing, the expense accounts are debited.

- Credit: Decreases an expense account. This is unusual and might occur with the correction of an erroneous expense entry.

The Expanded Accounting Equation and Debits/Credits

The accounting equation can be expanded to explicitly include revenue, expenses, and dividends to illustrate their impact on equity more clearly:

Assets = Liabilities + Equity (Beginning) + Owner Contributions + Revenues – Expenses – Dividends

Within this expanded framework:

- Revenues increase Equity, so they have a normal credit balance.

- Expenses decrease Equity, so they have a normal debit balance.

- Dividends decrease Equity, so they have a normal debit balance.

This distinction helps reinforce why revenues are credited and expenses are debited.

Illustrative Transactions and Journal Entries

To solidify the understanding of debit and credit, let’s examine a few common business transactions and how they are recorded using journal entries. A journal entry is the first record of a transaction in the accounting system.

Transaction 1: A Company Receives Cash for Services Rendered

Scenario: A consulting firm provides services to a client and receives $5,000 in cash.

Analysis:

- The company’s cash (an asset) increases.

- The company’s consulting revenue (which increases equity) increases.

Journal Entry:

| Date | Account | Debit | Credit |

|---|---|---|---|

| [Date] | Cash | $5,000 | |

| Consulting Revenue | $5,000 | ||

| To record cash received for services |

Explanation: Cash is debited because it is an asset account and it has increased. Consulting Revenue is credited because it is a revenue account that increases equity, and revenues have a normal credit balance.

Transaction 2: A Company Purchases Office Supplies on Credit

Scenario: A company buys $1,000 worth of office supplies from a vendor, agreeing to pay later.

Analysis:

- The company’s office supplies (an asset) increase.

- The company’s accounts payable (a liability) increase.

Journal Entry:

| Date | Account | Debit | Credit |

|---|---|---|---|

| [Date] | Office Supplies | $1,000 | |

| Accounts Payable | $1,000 | ||

| To record purchase of office supplies on credit |

Explanation: Office Supplies is debited because it’s an asset account that has increased. Accounts Payable is credited because it’s a liability account that has increased.

Transaction 3: A Company Pays its Rent Expense

Scenario: A company pays $2,000 for its monthly rent.

Analysis:

- The company’s cash (an asset) decreases.

- The company’s rent expense (which decreases equity) increases.

Journal Entry:

| Date | Account | Debit | Credit |

|---|---|---|---|

| [Date] | Rent Expense | $2,000 | |

| Cash | $2,000 | ||

| To record payment of monthly rent |

Explanation: Rent Expense is debited because it’s an expense account that has increased (and expenses have a normal debit balance). Cash is credited because it’s an asset account that has decreased.

The General Ledger and Financial Statements

Once journal entries are made, they are posted to the general ledger. The general ledger is a collection of all the T-accounts (or their digital equivalents) for a company. Each account in the general ledger summarizes all the debits and credits that have affected it.

The balances from the general ledger are then used to prepare the financial statements:

- The Balance Sheet: Presents the company’s assets, liabilities, and equity at a specific point in time. It directly reflects the accounting equation (Assets = Liabilities + Equity).

- The Income Statement: Reports the company’s revenues, expenses, and net income (or loss) over a period.

- The Statement of Cash Flows: Shows the movement of cash into and out of the company from its operating, investing, and financing activities.

The debit and credit system, by ensuring that all transactions are recorded in a balanced manner, is the invisible scaffolding that supports the accuracy and reliability of these crucial financial reports. Mastering the concept of debit and credit is not just about understanding accounting jargon; it’s about unlocking the ability to interpret and understand the financial story of any business.