Understanding the security protocols that protect our digital transactions is paramount in today’s interconnected world. While the acronym CVV might not be as immediately recognizable as other online security terms, it plays a crucial role in safeguarding credit and debit card information. Often referred to as a security code, authorization code, or card verification value, the CVV is a vital element in preventing fraudulent use of your payment cards.

The Genesis and Purpose of CVV Codes

The Card Verification Value (CVV) was developed by Visa in the late 1990s as a response to the escalating issue of online credit card fraud. As e-commerce began to gain traction, so too did the ability for criminals to exploit stolen card details without needing the physical card itself. Unlike the magnetic stripe on the back of a card, which can be easily duplicated, the CVV is a unique security feature printed directly on the card and, crucially, is not stored in the magnetic stripe data.

How CVV Works in a Transaction

When you make a purchase online or over the phone, you’ll typically be asked to provide not only your card number, expiry date, and billing address but also the CVV code. This seemingly small piece of information acts as a crucial verification step. The merchant’s payment gateway or processor sends the CVV to the card issuer (your bank) along with the transaction details. The issuer then checks if the provided CVV matches the one on file for that specific card.

If the CVV matches, it provides a strong indication that the person making the transaction is in possession of the physical card. This is because, in most cases, CVV codes are not meant to be stored by merchants for future transactions. This “card-present” verification significantly reduces the risk of fraudulent transactions where only the card number and expiry date have been compromised.

The Different Names and Formats

While the core function remains the same, the CVV code goes by different names depending on the card network:

- CVV (Card Verification Value): Used by Visa. It’s typically a 3-digit number.

- CVC (Card Verification Code): Used by Mastercard. It’s also a 3-digit number.

- CID (Card Identification Number): Used by American Express. This is a distinctive 4-digit number, usually located on the front of the card, above the embossed account number.

- CSC (Card Security Code): A more generic term often used interchangeably with CVV/CVC.

- CVV2/CVC2/CID2: These suffixes (V2, C2, ID2) often denote that the code is intended for use in “card-not-present” transactions, distinguishing it from the data encoded in the magnetic stripe.

Regardless of the nomenclature, the underlying principle is to provide an additional layer of security beyond just the primary card details.

Locating Your CVV Code

The physical location of the CVV code varies slightly depending on the type of card you possess:

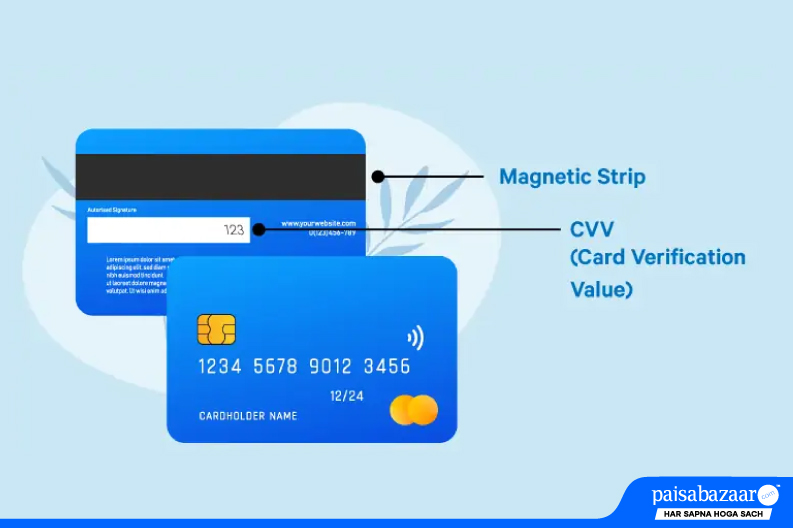

For Visa, Mastercard, and Discover Cards

On these cards, the CVV is almost universally found on the back of the card. It’s usually printed in the signature area, appearing as a 3-digit number that is separate from, or at the end of, the embossed account number.

For American Express Cards

American Express cards present a slight variation. Their security code, the CID, is typically a 4-digit number and is located on the front of the card, just above the embossed account number.

It’s important to note that for some newer chip-enabled cards, the CVV might be more subtly printed or embedded. However, the principle of it being a distinct code for online verification remains.

The Importance of CVV in Online Security

The CVV code is a cornerstone of online transaction security, and its importance cannot be overstated. Its primary function is to deter fraudsters by making it more difficult to use stolen card information.

Preventing Card-Not-Present (CNP) Fraud

Card-Not-Present (CNP) fraud occurs when a transaction is initiated without the physical card being presented at a point of sale. This is the most common type of credit card fraud and happens frequently in online and telephone transactions. Without the CVV, a fraudster who has only managed to obtain a card number and expiry date could more easily complete a purchase. The requirement for the CVV significantly raises the bar for such fraudulent activities.

Merchant Responsibilities and PCI DSS Compliance

The Payment Card Industry Data Security Standard (PCI DSS) is a set of security standards designed to ensure that all companies that accept, process, store, or transmit credit card information do so securely. A critical aspect of PCI DSS compliance is the prohibition of merchants from storing CVV data after a transaction has been authorized. This is a crucial security measure. If a merchant’s systems were breached, and they had stored CVVs, this sensitive information would also be exposed, greatly amplifying the damage. The fact that merchants are forbidden from storing this code ensures that even if their systems are compromised, the CVV itself cannot be easily misused in subsequent fraudulent transactions.

The Role of CVV in Tokenization

While CVV is a vital security feature, it’s not the only one. Modern payment systems increasingly utilize tokenization. Tokenization replaces sensitive data, like the actual card number and CVV, with a unique, non-sensitive identifier called a token. This token can be used for subsequent transactions without exposing the original card details. In this context, while the CVV might be used for the initial transaction to generate a token, the token itself might not directly contain or require the CVV for subsequent authorizations, further enhancing security.

Protecting Your CVV

Given its importance, protecting your CVV code is essential for preventing unauthorized use of your cards.

Never Share Your CVV Unnecessarily

Treat your CVV like your PIN. Only provide it when you are making a legitimate purchase through a secure and trusted channel. Be wary of unsolicited requests for your CVV, whether via email, text message, or phone call. Legitimate merchants will only ask for your CVV during the checkout process on their secure website or when you are making a purchase over the phone.

Be Cautious of Phishing Attempts

Phishing scams often try to trick individuals into revealing sensitive information, including their CVV code. These scams can appear as legitimate emails or websites from banks or online retailers. Always verify the legitimacy of a website or request before entering your card details. Look for the “https://” in the website’s address and a padlock icon in your browser’s address bar, indicating a secure connection.

Secure Your Physical Cards

While the CVV is not stored electronically in a way that’s easily accessible to cybercriminals through typical data breaches, the physical card itself can be lost or stolen. It’s important to keep your cards in a secure place and report any lost or stolen cards to your bank immediately.

Regular Review of Statements

Periodically review your credit and debit card statements for any unauthorized transactions. If you notice anything suspicious, contact your bank or card issuer immediately to report the fraudulent activity and initiate a dispute.

Limitations of CVV

While the CVV is a powerful security tool, it’s not infallible and has its limitations.

Susceptibility to Physical Theft

The most significant limitation is that the CVV is printed on the physical card. If your card is physically stolen, the thief will have direct access to the CVV along with your card number and expiry date, allowing them to make fraudulent purchases, particularly in “card-present” scenarios where the CVV might not be as rigorously checked as in online transactions.

Merchant Data Breaches (Without CVV Storage)

Although merchants are prohibited from storing CVVs, a compromised merchant still poses a risk. If a fraudster gains access to a merchant’s database, they might obtain card numbers and expiry dates. While they wouldn’t get the CVV from that specific breach, they could potentially use this information for targeted phishing attempts to trick customers into revealing their CVVs separately.

Evolving Fraud Techniques

As security measures evolve, so do the methods employed by fraudsters. While CVV helps, sophisticated scams might involve social engineering to obtain CVV codes, or exploiting vulnerabilities in less secure online platforms.

The Future of Card Security

The CVV has been a successful mechanism for enhancing transaction security for decades. However, the payment industry is constantly innovating to provide even more robust protection. Technologies like EMV chips (chip-and-PIN) and advanced tokenization are becoming standard. EMV chips provide dynamic data for each transaction, making them much harder to counterfeit than magnetic stripes. Tokenization, as mentioned earlier, replaces sensitive card data with unique tokens, significantly reducing the risk if a database is breached.

Despite these advancements, the CVV remains a crucial layer of defense. It continues to serve as a vital verification step in many online and telephone transactions, ensuring that the person initiating the purchase is likely in possession of the physical card. Understanding what a CVV code is, where to find it, and how to protect it empowers consumers to engage in digital commerce with greater confidence and security.