In the rapidly evolving landscape of unmanned aerial vehicles (UAVs), the focus is often placed on rotor speed, battery density, or the latest CMOS sensor. However, as the industry shifts from a hobbyist pastime to a sophisticated enterprise sector, the “invisible” infrastructure—specifically financial identity and digital transactions—has become just as critical as the hardware itself. When we ask, “What is a credit card account number?” in the context of Tech & Innovation (Category 6), we are not merely discussing a string of sixteen digits on a piece of plastic. We are discussing the primary key for the modern drone economy, the gateway to SaaS (Software as a Service) integration, and the fundamental component of secure, autonomous commerce.

The Commercial Backbone: Why Financial Identity Matters in UAV Operations

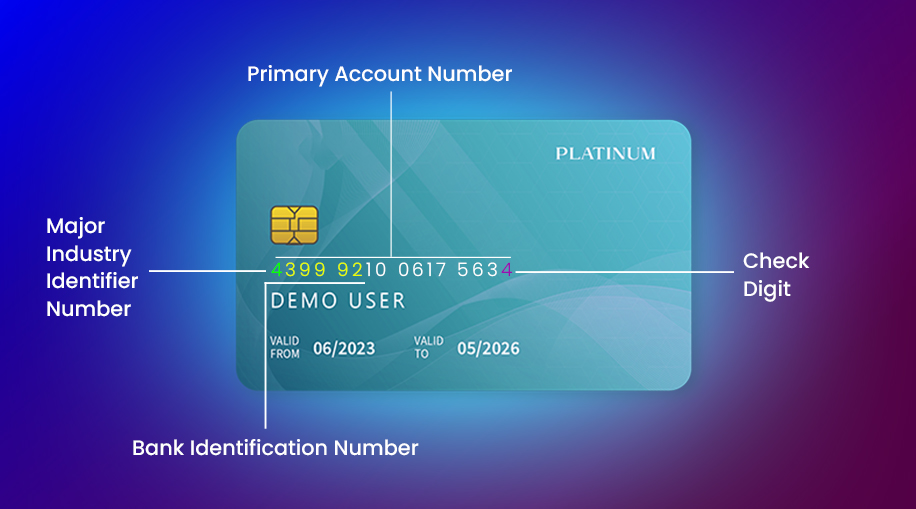

At its simplest level, a credit card account number is a unique identifier used to facilitate the transfer of funds between a cardholder and a service provider. In the world of drone innovation, this number acts as the bridge between the physical aircraft and the digital services required to make that aircraft useful. Today’s professional drones are rarely “standalone” devices; they are nodes in a massive data-processing network.

The Rise of the Subscription-Based Drone Economy

Modern drone technology relies heavily on proprietary software for mapping, thermal analysis, and fleet management. Platforms like DroneDeploy, Pix4D, or DJI Terra require active subscriptions to process the gigabytes of photogrammetry data collected during a flight. Here, the credit card account number is the “digital fuel” that keeps these systems running. Without a verified account number linked to a drone operator’s profile, the advanced AI-driven mapping and autonomous flight paths become inaccessible. Innovation in this sector is driven by recurring revenue models that allow developers to push over-the-air (OTA) updates, ensuring that the hardware remains at the cutting edge of safety and efficiency.

Regulatory Compliance and Remote ID Payments

As global aviation authorities like the FAA (Federal Aviation Administration) and EASA (European Union Aviation Safety Agency) implement stricter Remote ID requirements, the financial identity of the operator becomes a tool for accountability. Registering a drone often requires a nominal fee, where the credit card account number serves as a secondary form of identity verification. This ensures that the pilot in command is a verifiable entity, bridging the gap between anonymous flight and integrated airspace management.

Insurance and On-Demand Liability

Innovation in drone “InsureTech” has led to the development of micro-policies. Using mobile apps, a pilot can purchase flight insurance for a specific two-hour window over a specific GPS coordinate. This real-time transaction is powered by the stored credit card account number, allowing for instantaneous coverage that makes professional operations in high-risk environments legally and financially viable.

Technical Security: Encryption and Data Protection in Drone Applications

When an operator enters their credit card account number into a drone controller or a mobile flight app, they are initiating a high-stakes exchange of sensitive data. In the realm of Tech & Innovation, the security of this financial data is as paramount as the encryption used to protect the drone’s command-and-control (C2) link.

PCI DSS Compliance in UAV Software Ecosystems

For developers of drone apps, adhering to the Payment Card Industry Data Security Standard (PCI DSS) is a significant technical hurdle. Innovation in this space involves creating “tokenized” environments. When a credit card account number is entered, it is immediately swapped for a “token”—a unique string of characters that has no value to hackers but allows the drone service to bill the user for data processing or cloud storage. This ensures that even if a drone manufacturer’s database is breached, the actual financial identifiers of the pilots remain secure.

End-to-End Encryption from Controller to Cloud

Modern drone controllers are essentially high-powered Android or iOS tablets. Because they are connected to the internet to download maps and sync flight logs, they are susceptible to the same cyber threats as any other mobile device. Innovations in drone “fintech” involve securing the transmission of account numbers through Secure Socket Layer (SSL) and Transport Layer Security (TLS) protocols. This prevents “man-in-the-middle” attacks where a malicious actor might attempt to intercept financial data while the pilot is connected to a public Wi-Fi network to sync flight data.

Multi-Factor Authentication (MFA) and Biometric Links

To further protect the credit card account number associated with a drone fleet, many enterprise platforms are integrating biometric security. A pilot may need to provide a fingerprint or facial scan on their smart controller to authorize a high-value purchase, such as a “Unlock Zone” license or an expensive software plugin. This merges the physical security of the operator with the digital security of the financial account.

The Future of Autonomous Commerce: Drones as Independent Economic Agents

The most exciting innovation regarding financial identifiers in the drone space is the move toward “Machine-to-Machine” (M2M) payments. In this futuristic but rapidly approaching scenario, the “account holder” might not be a human, but the drone itself.

Digital Wallets for Autonomous Delivery Drones

As we move toward autonomous delivery networks, drones will need to interact with smart infrastructure. Imagine a delivery drone landing on a third-party charging pad. To “pay” for the electricity, the drone must communicate its financial credentials to the charging station. In this context, the credit card account number is integrated into the drone’s onboard computer as part of a secure digital wallet. This allows the drone to autonomously navigate, recharge, and pay for its own maintenance without human intervention.

Smart Contracts and Blockchain Integration

Tech innovators are exploring the use of blockchain to manage drone transactions. Instead of a traditional credit card account number, a drone might use a cryptographic public key linked to a digital ledger. This allows for “smart contracts,” where payment for a successful delivery or a completed mapping mission is automatically released to the drone’s account the moment the telemetry data confirms the task is complete. This level of automation is the pinnacle of current drone tech research, aiming to create a frictionless “Drone Economy.”

Fleet Management and Automated Procurement

For large-scale enterprise operations—such as a fleet of 500 drones monitoring agricultural yields—the traditional method of manual billing is inefficient. Innovation in fleet management software allows for “automated procurement.” When the software detects that a drone’s propeller has reached its fatigue limit (based on flight hours), it can automatically use the stored credit card account number to order a replacement part from the manufacturer. This creates a self-sustaining lifecycle for the hardware.

Mitigating Risks: Protecting Sensitive Financial Data in Remote Sensing

While the integration of financial accounts enables incredible innovation, it also introduces new risks. In professional drone work, specifically remote sensing and infrastructure inspection, the data collected is often highly sensitive (e.g., inspecting a nuclear power plant or a military base).

The Danger of Account Linking

If a credit card account number is linked to a drone account that also contains sensitive flight logs and GPS coordinates, it creates a “honey pot” for corporate espionage. Tech innovators are currently working on “de-linking” these data sets. By using different encryption keys for financial data and flight data, companies can ensure that a breach of a pilot’s billing information does not lead to a breach of their confidential mission data.

Cloud Storage and Data Sovereignty

Many drone service providers are moving toward localized data storage to protect both financial and flight information. For instance, a European drone operator may require that their credit card account number and their 3D models be stored on servers located within the EU to comply with GDPR. The innovation here lies in “Geo-fencing” data, ensuring that financial identifiers never leave a specific jurisdiction, thereby protecting the user from international data theft.

The Evolution of the “Account Number”

In the coming years, we may see the traditional 16-digit credit card account number replaced by more sophisticated “Virtual Account Numbers” (VANs). These are temporary, drone-specific numbers that expire after a single transaction. If an operator is using a drone in a high-risk area or using a new, unverified third-party app, they can generate a VAN. This represents the ultimate innovation in financial security for the UAV industry, ensuring that the primary credit line remains untouched even if the temporary drone-ID is compromised.

Conclusion: The Financial Infrastructure of Flight

The question “What is a credit card account number?” yields a complex answer when viewed through the lens of Drone Tech & Innovation. It is the foundation of the subscription models that power AI analysis; it is the identity marker that ensures regulatory compliance; and it is the key to the future of autonomous M2M commerce.

As we continue to push the boundaries of what UAVs can achieve—from autonomous 5G-linked delivery swarms to AI-driven search and rescue—we must remember that the software and hardware are only half of the story. The secure, innovative management of financial data is the silent engine that allows these machines to take flight, ensuring that the drone industry remains a viable, professional, and secure frontier of modern technology. By understanding the critical role of the credit card account number today, we prepare ourselves for a future where drones are not just tools, but active, financially independent participants in the global economy.