The world of corporate finance and investment can seem like a labyrinth of jargon and complex calculations. For those looking to understand how companies fund their operations and how investors generate returns, a fundamental concept is the corporate bond. At the heart of any bond’s income generation lies its coupon rate, a seemingly simple figure that carries significant weight in the financial markets. Understanding the coupon rate is crucial for both issuers seeking capital and investors aiming for predictable income streams.

The Anatomy of a Corporate Bond

Before delving into the specifics of the coupon rate, it’s essential to grasp the basic structure of a corporate bond. A corporate bond is essentially a loan made by investors to a corporation. The corporation promises to repay the principal amount (face value) on a specific maturity date and to make periodic interest payments to the bondholder until that date. These periodic interest payments are what we commonly refer to as “coupons.”

Key Components of a Bond

- Face Value (Par Value): This is the principal amount of the bond that the issuer will repay to the bondholder at maturity. It is typically $1,000 or $100 for most corporate bonds.

- Maturity Date: This is the date on which the issuer is obligated to repay the face value of the bond to the bondholder. Bonds can have maturities ranging from a few years to several decades.

- Coupon Rate: This is the annual interest rate that the issuer agrees to pay on the face value of the bond. It is expressed as a percentage of the face value.

- Coupon Payments: These are the actual cash payments of interest made by the issuer to the bondholder. They are typically paid semi-annually (twice a year) but can also be paid annually or quarterly.

The interplay of these components determines the overall return an investor can expect from a corporate bond. While the face value and maturity date define the repayment schedule, the coupon rate is the primary driver of the bond’s income-generating potential during its life.

Defining the Coupon Rate

The coupon rate, often simply called the “coupon,” is the stated interest rate on a bond. It represents the annual interest payment as a percentage of the bond’s face value. For instance, if a corporate bond has a face value of $1,000 and a coupon rate of 5%, the issuer will pay $50 in interest per year to the bondholder.

Calculation of Coupon Payments

The calculation is straightforward:

Annual Interest Payment = Face Value × Coupon Rate

If the interest payments are made semi-annually, as is common, each payment would be half of the annual amount:

Semi-Annual Interest Payment = (Face Value × Coupon Rate) / 2

So, in our example of a $1,000 bond with a 5% coupon rate paid semi-annually, the investor would receive $25 every six months ($50 / 2 = $25).

Distinction from Yield

It’s crucial to distinguish the coupon rate from the bond’s yield. While the coupon rate is fixed for the life of the bond, the bond’s yield can fluctuate. The yield to maturity (YTM) is the total return anticipated on a bond if it is held until it matures. YTM takes into account the bond’s current market price, its coupon payments, and its face value.

- Coupon Rate: A fixed percentage set at issuance, determining the absolute dollar amount of interest payments.

- Yield: The actual rate of return an investor earns, which is influenced by the bond’s market price relative to its face value and coupon rate. If a bond is trading above its face value (at a premium), its yield will be lower than its coupon rate. Conversely, if it’s trading below its face value (at a discount), its yield will be higher than its coupon rate.

Factors Influencing the Coupon Rate

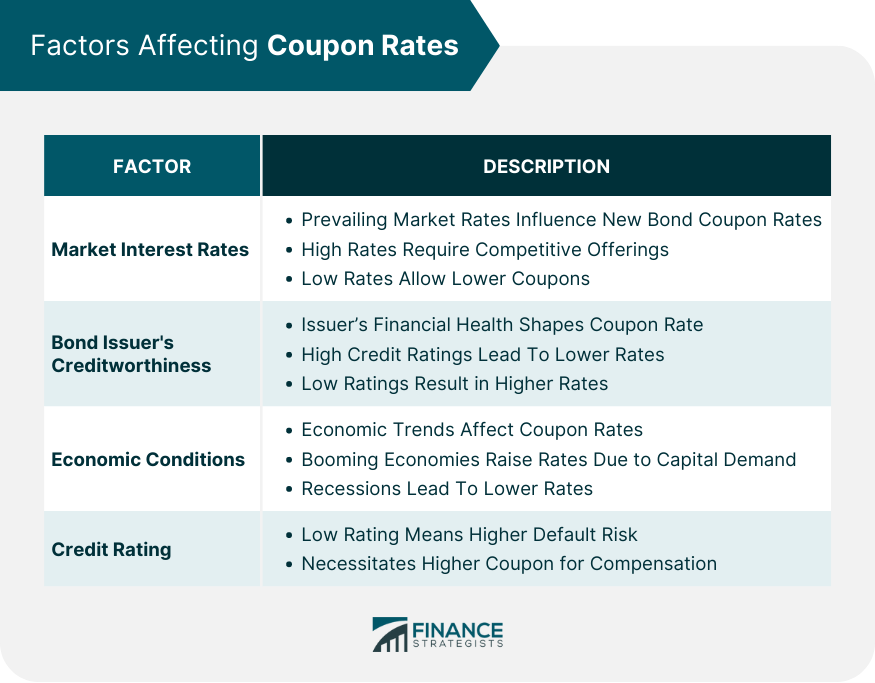

The coupon rate a corporation can offer on its bonds is not arbitrary. It is determined by a complex interplay of several factors, primarily reflecting the perceived risk of the issuer and prevailing market interest rates.

Issuer’s Creditworthiness

The most significant determinant of a bond’s coupon rate is the issuer’s creditworthiness, often assessed by credit rating agencies. Companies with strong financial health, a proven track record of profitability, and low levels of debt are considered less risky. These issuers can typically offer lower coupon rates because investors are willing to accept a smaller return for the higher security of their investment.

Conversely, companies with weaker financial positions, higher debt loads, or a history of financial instability are considered riskier. To attract investors, these issuers must offer higher coupon rates to compensate for the increased risk of default. This is often referred to as a “risk premium.” Bonds issued by companies with poor credit ratings are known as “high-yield” or “junk” bonds, characterized by significantly higher coupon rates.

Prevailing Interest Rates

The coupon rate is also influenced by the general level of interest rates in the economy. If interest rates are high across the market, corporations will generally need to offer higher coupon rates on their new bond issuances to be competitive with other investment opportunities. Conversely, in a low-interest-rate environment, companies can issue bonds with lower coupon rates.

Central banks, such as the Federal Reserve in the United States, play a pivotal role in setting benchmark interest rates. Their monetary policy decisions can significantly impact the cost of borrowing for corporations.

Maturity of the Bond

Generally, longer-term bonds carry higher coupon rates than shorter-term bonds from the same issuer. This is because investors demand a higher return for tying up their capital for a longer period. Longer maturities expose investors to greater interest rate risk (the risk that prevailing rates will rise, making their existing lower-rate bonds less attractive) and inflation risk.

Bond Covenants and Features

Certain features and covenants within a bond’s indenture (the legal contract between the issuer and bondholders) can also affect the coupon rate. For example:

- Seniority: Bonds that are higher in the capital structure (senior debt) are typically considered less risky and thus may have lower coupon rates than subordinated debt.

- Call Provisions: If a bond is “callable,” meaning the issuer has the right to redeem the bond before its maturity date, this can increase risk for the investor. To compensate for this, callable bonds often carry slightly higher coupon rates than non-callable bonds.

- Convertibility: Bonds that are convertible into shares of the issuer’s common stock offer investors the potential for capital appreciation. This added feature often allows the issuer to offer a lower coupon rate.

Market Demand and Supply

Like any other financial instrument, the demand and supply dynamics in the bond market can influence coupon rates. If there is high demand for corporate bonds from investors, issuers may be able to offer slightly lower coupon rates. Conversely, if the supply of new corporate bonds outweighs investor demand, issuers may need to offer more attractive coupon rates to attract buyers.

The Significance of the Coupon Rate for Investors

For investors, the coupon rate is a critical factor in evaluating a corporate bond. It directly determines the amount of regular income they can expect from their investment.

Income Generation

The primary appeal of corporate bonds for many investors is their predictable income stream. The coupon payments provide a steady source of cash flow, which can be particularly attractive for retirees or those seeking to supplement their regular income. Investors can analyze the coupon rate to estimate their potential earnings from a bond portfolio.

Reinvestment Risk

While coupon payments provide income, they also present an opportunity for reinvestment risk. When investors receive coupon payments, they have the option to reinvest these funds. If prevailing interest rates have fallen since the bond was issued, investors may have to reinvest their coupon payments at lower rates, reducing their overall potential return. Conversely, if interest rates have risen, reinvesting coupon payments can lead to a higher overall yield.

Impact on Bond Pricing

As mentioned earlier, the coupon rate is a key input in determining a bond’s market price. Bonds are often issued at or near their face value. However, as market interest rates change, the price of existing bonds adjusts to reflect their attractiveness relative to new bonds being issued.

- Higher Coupon Bonds: Bonds with higher coupon rates are generally more attractive when market interest rates are stable or falling. They tend to trade at a premium (above face value) because their fixed payments are more valuable than what new bonds offer.

- Lower Coupon Bonds: Bonds with lower coupon rates become less attractive when market interest rates rise. They typically trade at a discount (below face value) as investors demand a higher yield to compensate for the lower fixed payments.

Diversification and Risk Management

Corporate bonds, with their varying coupon rates and maturities, play a vital role in portfolio diversification. By including bonds with different risk profiles and income characteristics, investors can potentially reduce the overall volatility of their portfolio and manage risk more effectively. The coupon rate helps investors select bonds that align with their income needs and risk tolerance.

The Coupon Rate’s Role for Issuers

From the perspective of a corporation, the coupon rate represents the cost of borrowing. It is a significant expense that impacts the company’s profitability and financial strategy.

Cost of Capital

The coupon rate directly contributes to the issuer’s cost of capital. A higher coupon rate means a higher annual interest expense, which reduces the company’s net income. Companies strive to issue debt at the lowest possible coupon rate to minimize their borrowing costs. This is why strong credit ratings are so valuable to corporations.

Financial Planning and Budgeting

The predictable nature of coupon payments allows corporations to accurately forecast their interest expenses. This predictability is essential for sound financial planning, budgeting, and cash flow management. Companies can allocate funds accordingly to meet their debt obligations.

Capital Raising Strategy

When a corporation decides to raise capital through debt issuance, the prevailing coupon rates in the market play a crucial role in their decision-making. They must assess whether the current interest rate environment is favorable for issuing bonds. If rates are high, a company might postpone a bond issuance or consider alternative financing methods. If rates are low, it can be an opportune time to lock in lower borrowing costs for the long term.

Investor Relations

The coupon rate and the overall terms of a bond offering are key considerations for attracting investors. A well-structured bond offering with a competitive coupon rate can help a company build and maintain positive relationships with the investment community, potentially making future capital raises easier and more cost-effective.

Conclusion: The Enduring Importance of the Coupon Rate

The coupon rate on a corporate bond, while a single numerical value, is a cornerstone of understanding corporate finance and fixed-income investing. It encapsulates the risk associated with the issuer, the prevailing economic conditions, and the time value of money. For investors, it is the direct promise of income, a vital component for portfolio building and wealth generation. For issuers, it represents the cost of capital, a critical element in their financial strategy and operational success. In the complex tapestry of financial markets, the coupon rate remains a fundamental and enduring concept, providing clarity and predictability in the world of corporate debt.