Cost absorption, in the context of business and particularly within the operational framework of tech-driven industries like those involving aerial technology, refers to the accounting principle where all manufacturing or production costs, both fixed and variable, are incorporated into the cost of a product. This means that the expense of producing a unit of goods or services is deemed to include not only direct materials and direct labor but also a portion of the overhead costs associated with running the operation. When applied to companies developing, manufacturing, or servicing complex technological products, understanding cost absorption is critical for accurate pricing, profitability analysis, and strategic decision-making.

The principle is rooted in the fundamental concept of matching revenue with expenses. For a product to be truly profitable, its selling price must cover not only the direct costs incurred in its creation but also the indirect costs that are essential for its existence and delivery. In the world of drones, flight technology, and advanced imaging systems, this encompasses a vast array of expenditures that extend far beyond the assembly line.

Understanding the Core Principles of Cost Absorption

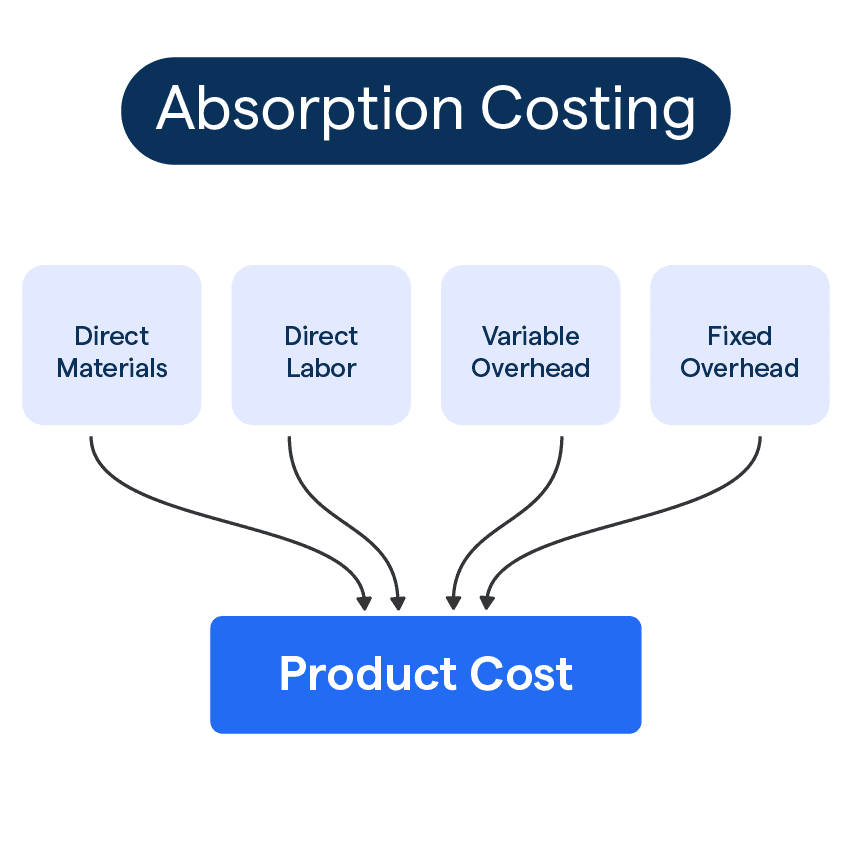

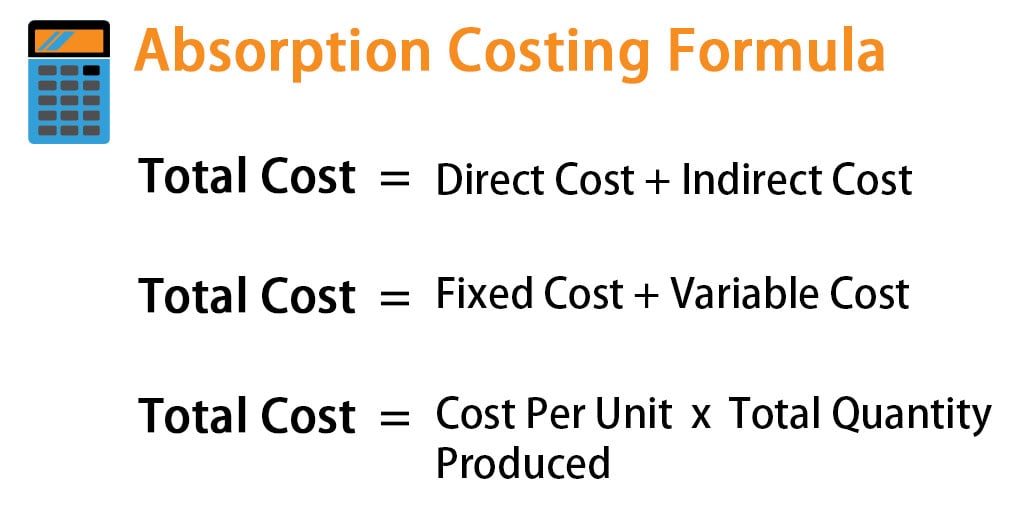

At its heart, cost absorption accounting, also known as full costing, aims to assign all costs related to production to the units manufactured. This contrasts with variable costing, which only allocates variable manufacturing costs to products. The rationale behind cost absorption is that fixed manufacturing overhead costs, such as factory rent, depreciation of machinery, and supervisory salaries, are necessary for the production process to occur. Therefore, they are considered a part of the cost of producing each unit.

Direct Costs: The Tangible Components

Direct costs are those that can be directly traced to a specific product. In the context of drone manufacturing, these would include:

- Direct Materials: The physical components that make up the drone. This spans from the carbon fiber for the frame, the plastic for the propellers, the wires and circuit boards for the electronics, and the sensors that form its ‘eyes’. For high-end imaging systems, this would also include lenses, image sensors, and stabilization hardware.

- Direct Labor: The wages paid to workers who are directly involved in the assembly and manufacturing process of the drone or its components. This includes assembly line workers, calibration technicians, and potentially specialized engineers working on the physical build.

Indirect Costs: The Essential Overheads

Indirect costs, or overheads, are those that cannot be directly traced to a specific product but are essential for the overall production process. These are the costs that cost absorption accounting seeks to allocate. They can be further categorized:

-

Manufacturing Overhead:

- Fixed Manufacturing Overhead: Costs that do not fluctuate with the level of production. Examples relevant to a drone manufacturer include:

- Rent or mortgage payments for the factory and assembly plant.

- Depreciation of manufacturing equipment, machinery, and tools used in production.

- Salaries of production supervisors, quality control managers, and maintenance staff.

- Insurance on the manufacturing facility and equipment.

- Property taxes on the manufacturing plant.

- Variable Manufacturing Overhead: Costs that vary in direct proportion to the level of production. Examples include:

- Indirect materials (e.g., lubricants for machinery, cleaning supplies for the factory floor).

- Indirect labor (e.g., wages for factory janitorial staff or security personnel whose hours might increase with facility usage).

- Electricity consumed by production machinery.

- Consumables for testing and calibration equipment.

- Fixed Manufacturing Overhead: Costs that do not fluctuate with the level of production. Examples relevant to a drone manufacturer include:

-

Non-Manufacturing Overhead: While cost absorption primarily focuses on manufacturing overhead, some interpretations and contexts might also consider allocating certain non-manufacturing overheads if they are deemed integral to the “cost of getting the product ready for sale.” However, standard cost absorption typically limits this to factory-related expenses. For a comprehensive understanding in industries with extensive R&D and support, it’s crucial to distinguish between product costs and period costs.

The Allocation Process: Distributing the Burden

The critical challenge in cost absorption accounting lies in how to equitably allocate indirect costs to individual product units. This is typically achieved through the use of overhead allocation rates. The process generally involves:

- Estimating Total Overhead Costs: At the beginning of an accounting period, the company forecasts its total indirect manufacturing costs.

- Identifying an Allocation Base: A driver or activity that is believed to have a strong relationship with the incurrence of overhead costs is chosen. Common allocation bases include:

- Direct labor hours

- Direct labor costs

- Machine hours

- Units produced

- Activity-based costing (ABC) drivers (e.g., number of setups, number of inspections, number of engineering changes)

- Calculating the Predetermined Overhead Rate: The total estimated overhead cost is divided by the total estimated amount of the allocation base.

- Formula: Predetermined Overhead Rate = Total Estimated Overhead / Total Estimated Allocation Base

- Applying Overhead to Products: As production occurs, overhead costs are applied to individual products or batches of products by multiplying the predetermined overhead rate by the actual amount of the allocation base used for that product.

- Formula: Applied Overhead = Predetermined Overhead Rate × Actual Amount of Allocation Base Used

For a drone manufacturer, this means that the cost of electricity powering the assembly robots, the depreciation of the automated soldering machines, and even a portion of the factory supervisor’s salary are all factored into the cost of each drone that rolls off the production line. This is crucial for understanding the true cost of producing a drone with advanced flight stabilization systems, sophisticated navigation sensors, or high-resolution gimbal cameras.

Why Cost Absorption Matters in Tech Manufacturing

The significance of cost absorption is amplified in industries characterized by high fixed costs and rapid technological advancement, such as drone technology and its associated sectors.

Pricing Strategies and Profitability Analysis

Accurate cost absorption is fundamental for setting competitive yet profitable prices. If a company understates its product costs by failing to absorb all manufacturing overhead, it might price its products too low, leading to insufficient profit margins or even losses. Conversely, over-absorption of costs can lead to prices that are uncompetitive, potentially driving customers to competitors.

For a company developing sophisticated FPV racing drones, the high cost of R&D, specialized tooling, and precision assembly requires a robust cost absorption method to ensure that the selling price of each drone adequately covers these investments. Similarly, manufacturers of professional aerial filmmaking gimbals must account for the extensive engineering, testing, and calibration involved in achieving cinematic-grade stability.

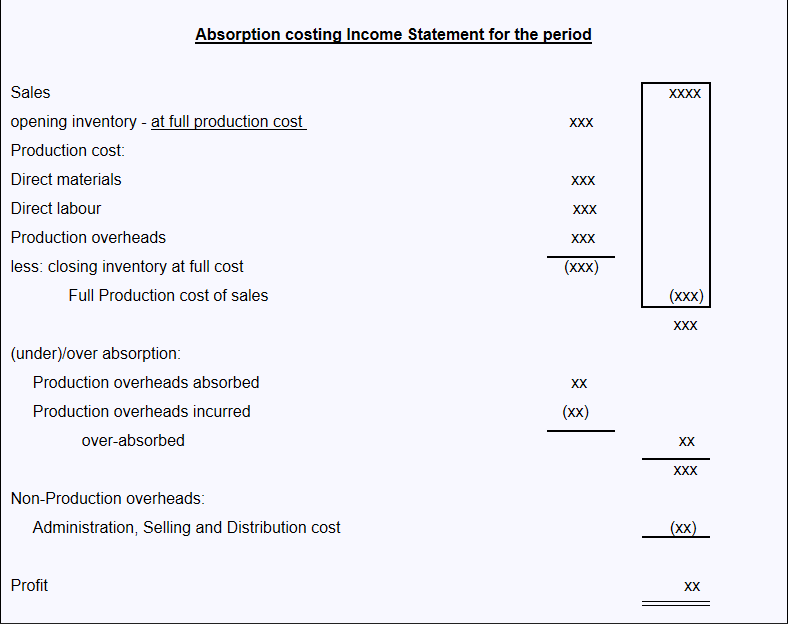

Inventory Valuation

Under cost absorption accounting, the cost of goods sold (COGS) and the value of ending inventory include direct materials, direct labor, and allocated manufacturing overhead. This is important for financial reporting, as it ensures that the balance sheet reflects a more complete cost of the inventory held.

If a drone company has a significant amount of inventory on hand—perhaps drones with advanced obstacle avoidance sensors or specialized thermal imaging payloads—the valuation of this inventory will directly reflect the absorbed overhead costs. This impacts the company’s reported assets and its gross profit when inventory is eventually sold.

Decision-Making and Strategic Planning

Understanding cost absorption provides management with deeper insights into the cost structure of their operations. This knowledge is invaluable for strategic decisions such as:

- Make-or-Buy Decisions: Should the company manufacture certain components in-house, or outsource them? This decision requires a clear understanding of the full cost of in-house production, including absorbed overhead.

- Product Line Evaluation: Which drone models or camera systems are the most profitable? Analyzing the absorbed costs per unit helps identify underperforming or highly profitable products.

- Investment in Automation: Investing in new machinery or automated assembly lines involves significant fixed costs. Cost absorption analysis helps justify these investments by demonstrating how increased efficiency and potential for higher production volumes can be leveraged to spread overhead over more units. For companies developing autonomous flight technology, the high upfront investment in software development and complex hardware necessitates careful consideration of how these costs will be absorbed over the life of the product.

Compliance with Accounting Standards

Cost absorption accounting is generally required by Generally Accepted Accounting Principles (GAAP) and International Financial Reporting Standards (IFRS) for external financial reporting. This ensures consistency and comparability across companies. Therefore, any company operating in the drone ecosystem that reports its financial results externally must adhere to these principles.

Challenges and Considerations in Cost Absorption

While cost absorption is a standard and essential accounting practice, it presents certain challenges, especially in dynamic industries:

-

Accuracy of Overhead Allocation: The choice of allocation base and the accuracy of overhead estimates can significantly impact product costs. If the chosen allocation base does not truly reflect the consumption of overhead resources, the resulting product costs will be distorted. For example, if machine hours are used to allocate overhead, but some products require significantly more setup time or quality inspections (which are also overhead-driven), those products might be under-costed. Activity-based costing (ABC) offers a more refined approach to allocating overhead by identifying specific activities that drive costs and assigning costs based on the consumption of those activities by each product.

-

Impact of Production Volume: Fixed overhead costs remain constant regardless of production volume. This means that as production volume increases, the fixed overhead cost per unit decreases (as the same total fixed overhead is spread over more units). Conversely, if production volume falls, the fixed overhead cost per unit rises. This can lead to fluctuations in reported profit even if the underlying operational efficiency hasn’t changed. This is particularly relevant for companies producing specialized drones or components, where demand can be cyclical or project-dependent.

-

Distinguishing Product vs. Period Costs: It’s crucial to correctly classify costs. Manufacturing overhead is a product cost, meaning it is inventoried and expensed when the product is sold. Non-manufacturing costs, such as marketing, sales, and administrative expenses, are period costs and are expensed in the period they are incurred, regardless of sales volume. Misclassification can lead to inaccurate inventory valuations and profitability assessments. For a company offering drone mapping services, the cost of the software used for analysis would typically be treated as a period cost (overhead for the service business) rather than a product cost embedded within each mapping report, unless a specific cost accounting model dictates otherwise.

In conclusion, cost absorption is a foundational accounting principle that dictates the inclusion of all manufacturing costs, both fixed and variable, in the cost of a product. For businesses operating in the cutting-edge fields of drones, flight technology, and advanced imaging, a thorough understanding and accurate application of cost absorption are not merely accounting exercises but critical drivers of pricing accuracy, profitability, informed decision-making, and ultimately, sustained success in a competitive and rapidly evolving technological landscape. It ensures that the true cost of innovation and production is recognized, enabling companies to invest wisely and deliver value effectively.