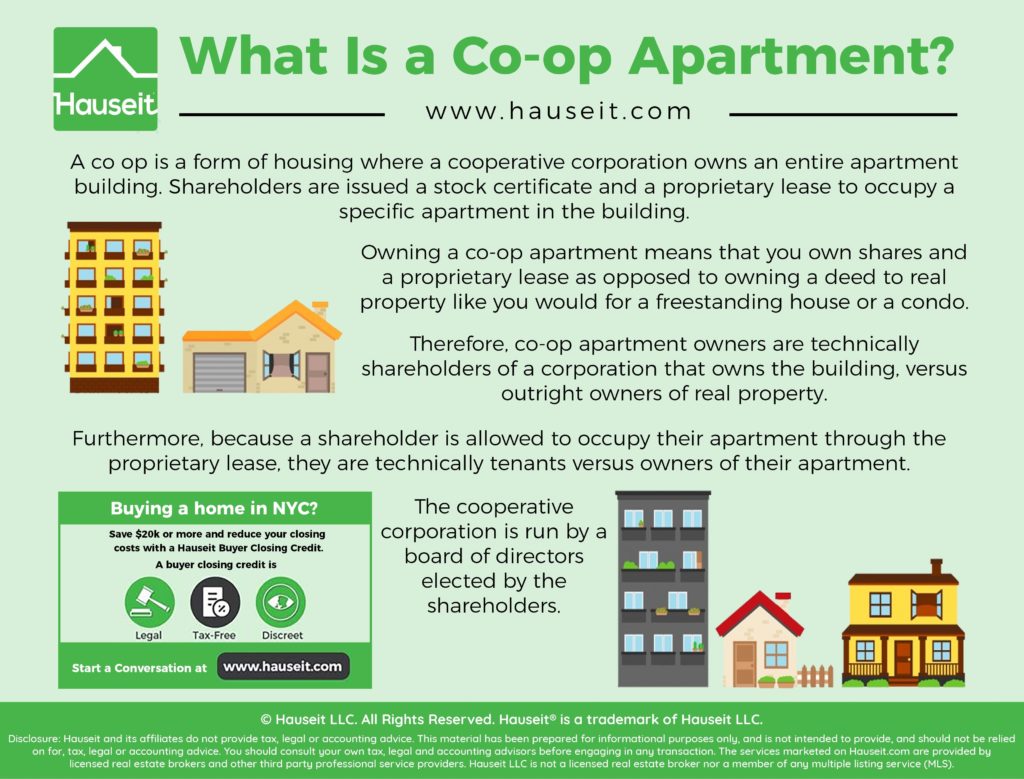

Cooperative housing, often shortened to co-op housing, represents a unique and increasingly popular model of homeownership and community living. Unlike traditional condominiums or single-family homes, co-op housing operates on a collective ownership principle, where residents are not individual property owners but rather shareholders in a corporation that owns the entire building or development. This fundamental difference shapes everything from governance and finances to the very fabric of community life. Understanding co-op housing requires delving into its structure, the rights and responsibilities of its members, and the distinct advantages and considerations it offers.

The Cooperative Structure Explained

At its core, a housing cooperative is a legal entity, typically a non-profit corporation, that owns the real estate where its members reside. When an individual purchases into a co-op, they are buying shares of stock in this corporation. These shares grant them the right to occupy a specific unit within the development, often through a long-term proprietary lease or occupancy agreement. This proprietary lease outlines the terms of their occupancy, including maintenance responsibilities, rules, and regulations.

The cooperative corporation itself is managed by a democratically elected board of directors, composed of resident shareholders. This board is responsible for the overall management of the property, including financial oversight, maintenance, and setting policies. Every shareholder has the right to vote for board members and, in many cases, to vote on significant decisions affecting the cooperative, such as major capital improvements or changes to the bylaws. This participatory governance is a hallmark of the co-op model, fostering a sense of collective responsibility and empowerment among residents.

Membership and Share Ownership

Purchasing a unit in a co-op involves acquiring a specific number of shares that correspond to the size and value of the unit. The total number of shares and their valuation are determined by the cooperative’s initial financing and subsequent market assessments. The price of these shares can fluctuate, but it generally reflects the underlying value of the property.

Beyond the initial share purchase, there are typically ongoing monthly fees, often referred to as “maintenance fees” or “carrying charges.” These fees are crucial for the cooperative’s financial health and cover a wide array of expenses. They are generally calculated based on the number of shares a member owns, with larger units or those with more desirable features often requiring higher monthly payments.

Proprietary Lease and Occupancy Rights

The proprietary lease is the legal document that governs a shareholder’s right to occupy a unit. It is not a traditional rental agreement, as the shareholder is, in essence, leasing their own unit from the corporation they co-own. This lease typically includes:

- Duration: Long-term, often extending for the life of the cooperative.

- Use of Premises: Outlines permitted uses of the unit and common areas.

- Maintenance Responsibilities: Delineates what the shareholder is responsible for within their unit and what the cooperative is responsible for in common areas and the building’s structure.

- Rules and Regulations: Incorporates the cooperative’s bylaws and any additional rules established by the board.

- Transfer of Shares: Details the process for selling or transferring shares, which often involves board approval.

This lease provides security of tenure for residents, as they are not subject to the arbitrary decisions of a single landlord. Their occupancy is tied to their ownership of shares and adherence to the cooperative’s rules.

Governance and Decision-Making

The democratic governance structure is a defining characteristic of cooperative housing. The resident shareholders are not passive occupants; they are active participants in the management and direction of their community.

The Board of Directors

The board of directors is the executive arm of the cooperative. Composed of elected shareholders, the board’s responsibilities are extensive and vital to the smooth operation of the co-op. These include:

- Financial Management: Budgeting, collecting maintenance fees, paying mortgages (if any) and operating expenses, and managing reserve funds for future repairs.

- Property Maintenance: Overseeing the upkeep of the building’s common areas, grounds, and structural elements.

- Policy Enforcement: Ensuring that residents abide by the cooperative’s bylaws and rules.

- Capital Improvements: Planning and approving major renovations or upgrades to the property.

- Liaison with Residents: Communicating with shareholders, addressing concerns, and facilitating meetings.

Board members are typically volunteers who dedicate their time and effort to the cooperative’s well-being. Their decisions are made in the best interest of the entire membership.

Shareholder Meetings and Voting

Regular shareholder meetings are essential for transparency and collective decision-making. These meetings provide a platform for:

- Information Dissemination: The board reports on the financial status, operational updates, and any significant developments.

- Elections: Shareholders elect members to the board of directors.

- Discussion and Debate: Residents can voice concerns, ask questions, and engage in discussions about the cooperative’s future.

- Voting on Major Issues: Crucial decisions, such as approving large capital expenditures, amending bylaws, or selling the property, often require a shareholder vote.

The principle of “one share, one vote” is common, though some cooperatives may have variations. This democratic process ensures that residents have a direct say in the management of their homes and communities.

Financial Aspects of Co-op Living

The financial model of co-op housing differs significantly from traditional homeownership. Understanding these nuances is crucial for anyone considering this form of living.

Maintenance Fees and What They Cover

The monthly maintenance fees are a significant component of co-op living. These fees are pooled to cover all operational costs of the cooperative. A comprehensive list of what these fees typically entail includes:

- Mortgage Payments: If the cooperative holds a blanket mortgage on the property, a portion of the fees goes towards servicing this debt.

- Property Taxes: Taxes on the entire property are paid by the cooperative.

- Utilities: Often includes water, sewer, and sometimes heating and electricity for common areas and, in some cases, for individual units.

- Building Insurance: Comprehensive insurance for the structure and common areas.

- Maintenance and Repairs: Routine upkeep of the building, grounds, and systems (plumbing, electrical, HVAC).

- Staff Salaries: For building superintendents, porters, or administrative staff.

- Reserve Funds: Contributions to a reserve fund for future capital expenditures and unexpected repairs.

- Management Fees: If a professional management company is hired.

The transparency in how these fees are allocated is a key benefit, as shareholders can see exactly where their money is going.

The “Flip Tax” and Other Fees

When a shareholder decides to sell their shares and move out, they typically encounter a “flip tax” or transfer fee. This is a one-time fee, usually a percentage of the sale price, paid to the cooperative. The purpose of the flip tax can vary:

- Funding Capital Improvements: To finance major projects without special assessments.

- Maintaining Lower Maintenance Fees: By providing an additional revenue stream.

- Discouraging Speculation: To encourage long-term residency.

Other fees might include move-in/move-out fees, subletting fees (if permitted), or fees for minor renovations that require board approval.

Subletting and Resale

Co-op policies regarding subletting and the resale of shares are generally more restrictive than in condominiums.

- Subletting: Many cooperatives have strict limitations on subletting, often requiring board approval and limiting the duration of subleases. This is to maintain the owner-occupancy nature of the community and prevent transient populations.

- Resale: When selling shares, the cooperative board typically has the right to approve prospective buyers. This screening process can involve reviewing financial information, conducting interviews, and ensuring that the buyer will be a suitable member of the community. This aspect can sometimes lead to longer sale timelines compared to other property types.

Advantages of Co-op Living

Cooperative housing offers a distinct set of benefits that appeal to a broad range of individuals and families.

Affordability and Value

In many markets, co-op units can be more affordable to purchase than comparable condominiums or single-family homes. This is often due to the cooperative’s ability to leverage economies of scale, secure favorable financing, and manage expenses collectively. The ongoing maintenance fees, while substantial, can provide a more predictable cost of living compared to the potential for unexpected special assessments in some other housing types.

Strong Sense of Community

The participatory governance and shared responsibility inherent in co-op living foster a robust sense of community. Residents are more likely to know their neighbors, be involved in decision-making, and feel a collective stake in the well-being of their building and neighborhood. This can translate into a more supportive and engaged living environment.

Stability and Predictability

The cooperative structure, with its democratically elected board and established bylaws, tends to promote stability and predictability. Major decisions are made through consensus and voting, reducing the likelihood of sudden, disruptive changes. The financial management, overseen by the board and often by professional management, aims for long-term fiscal health, which can offer peace of mind to residents.

Equity and Investment

While not direct property ownership, owning shares in a cooperative represents an investment in real estate. The value of these shares can appreciate over time, reflecting the overall value of the underlying property. Residents build equity through their share ownership and by contributing to the cooperative’s financial health through their maintenance fees.

Considerations and Potential Downsides

Despite its many advantages, co-op living is not for everyone. Several factors warrant careful consideration.

Board Approval and Restrictions

The board’s approval process for prospective buyers, as well as potential restrictions on subletting and renovations, can be a significant hurdle for some. The screening process, while aimed at maintaining community standards, can feel intrusive or lead to lengthy delays.

Financial Scrutiny

Potential buyers in a co-op will undergo rigorous financial scrutiny. Lenders and the cooperative board will want to see a strong financial history and a healthy debt-to-income ratio. This is to ensure that a shareholder can meet their ongoing financial obligations, particularly the monthly maintenance fees.

Limited Control Over Individual Unit

While residents have proprietary leases for their units, they do not have the same degree of autonomy as a fee-simple homeowner. Major renovations or alterations to the interior of a unit typically require board approval, and there may be restrictions on what can be done to preserve the building’s integrity and aesthetic.

Potential for Special Assessments

Although cooperatives strive for predictable finances, unexpected major repairs or capital expenditures can sometimes necessitate special assessments. These are additional charges levied on shareholders to cover unforeseen costs that exceed the reserve fund. While less common than in some other ownership models, they are a possibility that residents must be prepared for.

Conclusion

Cooperative housing offers a compelling alternative to traditional homeownership, blending communal living with a structured approach to property management. It appeals to those who value community, democratic participation, and a degree of financial predictability. By understanding the cooperative structure, the rights and responsibilities of shareholders, and the unique financial and governance models, individuals can determine if this vibrant form of living is the right fit for their lifestyle and aspirations. The inherent commitment to collective well-being makes co-op housing a powerful model for building strong, sustainable communities.