Chase Quick Deposit represents a significant leap in the evolution of consumer banking, epitomizing the broader trend of financial technology (fintech) innovation. At its core, it is a service offered by Chase Bank that allows customers to deposit checks directly into their accounts using a smartphone or tablet camera, rather than requiring a physical visit to a branch or an ATM. This capability, born from advancements in mobile technology and secure digital processing, has fundamentally reshaped how millions manage their finances, offering unparalleled convenience and efficiency in an increasingly digital world. It’s an innovation that transcends simple automation, embedding complex technological safeguards and user-centric design principles to deliver a seamless banking experience.

The Digital Evolution of Banking Deposits

The concept of depositing funds has long been tethered to physical interaction: presenting a check or cash to a teller, or feeding it into a machine. The advent of the internet brought online banking, allowing for transfers and bill payments, but physical deposits remained largely untouched by the digital revolution for some time. Chase Quick Deposit, along with similar services from other financial institutions, closed this gap, marking a pivotal moment in banking history.

This digital transformation isn’t just about convenience; it’s about accessibility and reducing friction in financial transactions. For consumers in remote areas, those with busy schedules, or individuals with mobility challenges, the ability to deposit a check from anywhere at any time significantly democratizes access to banking services. It leverages ubiquitous mobile technology, turning a personal device into a portable, secure banking portal. This paradigm shift aligns perfectly with the overarching movement towards embedded finance and ubiquitous banking, where financial services are integrated seamlessly into daily life rather than existing as standalone, separate tasks.

The journey to mobile check deposit involved overcoming substantial regulatory hurdles and building robust trust frameworks. Traditional banking operated on paper trails and physical verification. Translating this into a digital realm required innovative solutions for fraud prevention, image capture accuracy, and data security. The successful implementation of services like Chase Quick Deposit is a testament to the collaborative efforts of financial institutions, technology developers, and regulatory bodies in adapting to the digital age. It reflects a deeper understanding of consumer needs and the strategic application of technology to meet those demands, setting a new standard for customer expectations in the financial sector.

Core Mechanics and Technological Underpinnings

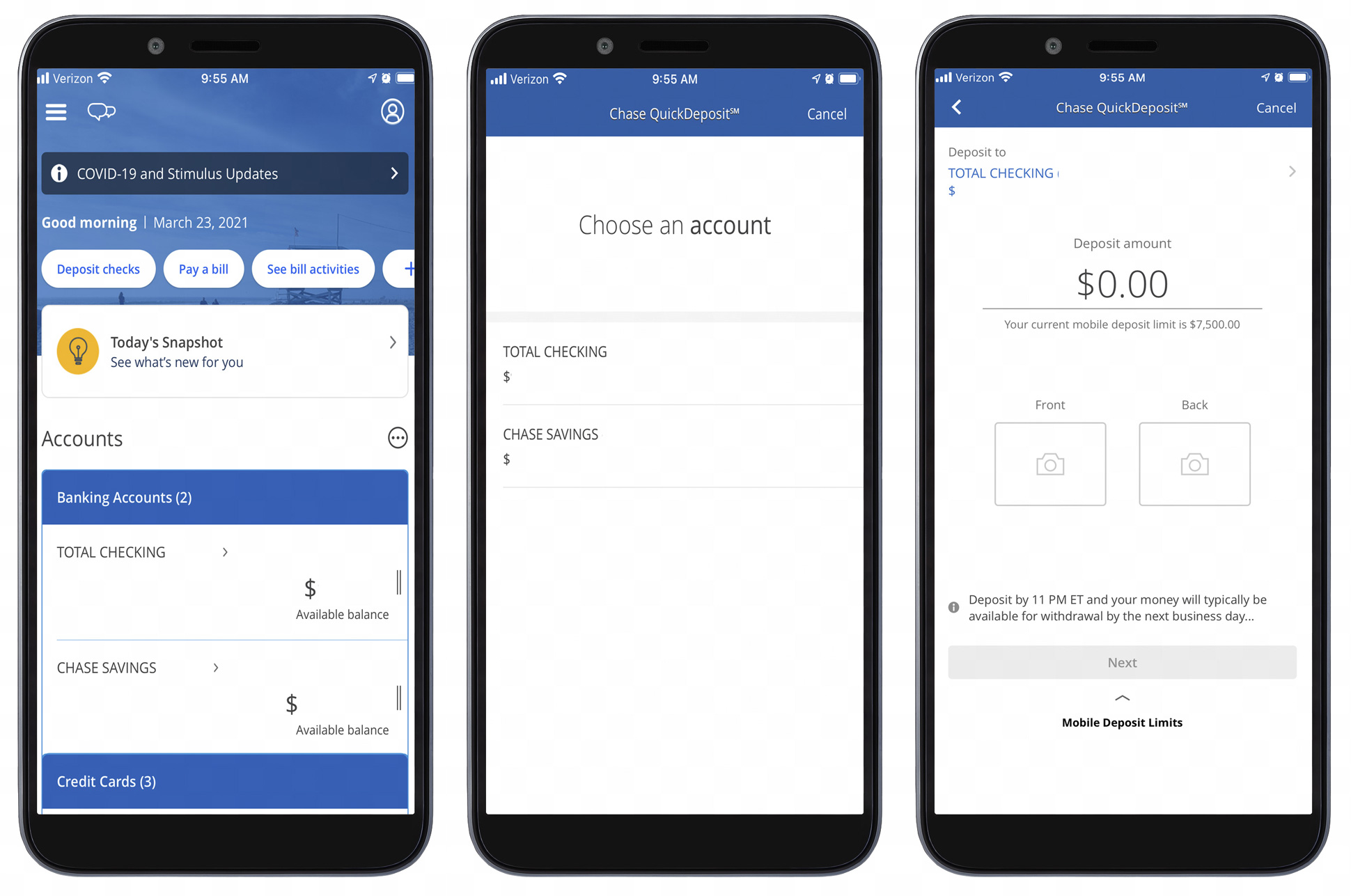

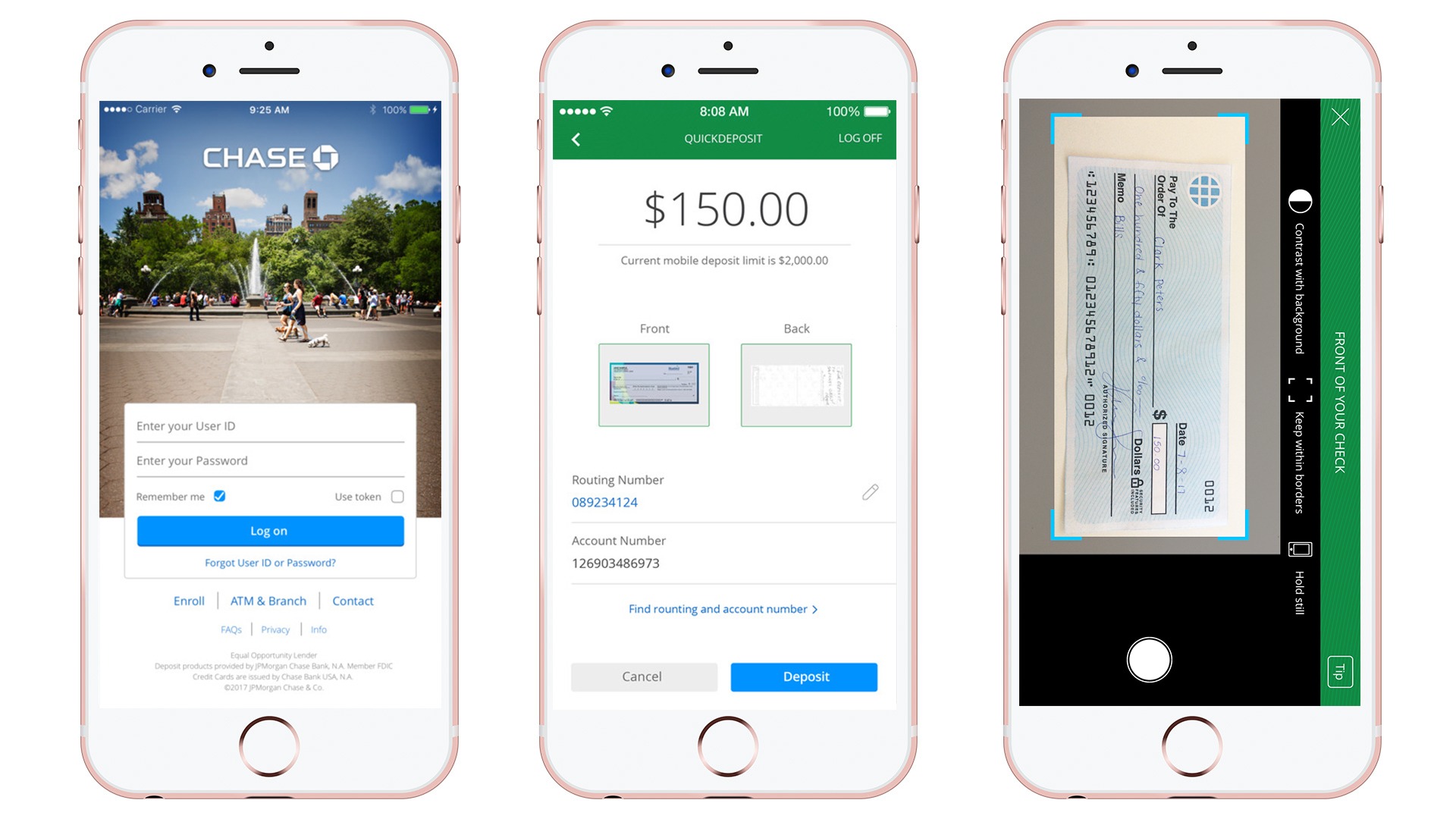

The seeming simplicity of Chase Quick Deposit belies a sophisticated array of technologies working in concert. When a user initiates a deposit, the process involves several critical steps, each underpinned by advanced software and security protocols.

Image Capture and Processing

The first step involves the smartphone’s camera capturing images of the front and back of the endorsed check. This is not merely a photograph; the application employs intelligent image recognition and processing algorithms. These algorithms are designed to detect the edges of the check, correct for distortions like skew and glare, and ensure the image is clear and legible. Optical Character Recognition (OCR) technology plays a crucial role here, automatically extracting key information such as the bank routing number, account number, check number, and the amount written in both numerical and textual formats. This data is then cross-referenced for consistency, flagging any discrepancies that might indicate an error or fraud. The quality of this image capture and data extraction is paramount to prevent processing delays or rejection of the deposit.

Data Transmission and Encryption

Once the check images and extracted data are processed locally on the device, they are transmitted to Chase’s secure servers. This transmission occurs over encrypted channels, typically using industry-standard protocols like TLS (Transport Layer Security), to protect sensitive financial information from interception. The data packets are heavily safeguarded, ensuring that account numbers, routing information, and personal details remain confidential throughout their journey from the user’s phone to the bank’s infrastructure.

Fraud Detection and Risk Management

Before a deposit is credited, it undergoes a rigorous fraud detection process. This involves a combination of automated systems and, in some cases, manual review. Algorithms analyze various parameters, including the check’s history, the account’s activity, the amount of the deposit, and behavioral patterns, to identify potential red flags. For instance, attempts to deposit the same check multiple times (known as “double dipping”) are swiftly detected by unique identifier tracking, often involving microprinting or other security features on the check itself, along with digital watermarking embedded during the initial processing. Holding periods for funds from mobile deposits are also a risk management tool, allowing time for the check to clear through the Automated Clearing House (ACH) network before funds become fully available, mitigating the risk of fraudulent checks.

Integration with Core Banking Systems

Finally, the validated deposit information is seamlessly integrated with Chase’s core banking systems. This updates the customer’s account balance, triggers the necessary accounting entries, and initiates the interbank clearing process. This integration relies on robust API (Application Programming Interface) frameworks, ensuring that different banking systems can communicate securely and efficiently in real-time or near real-time. The entire process, from capture to provisional credit, often takes mere minutes, dramatically reducing the time and effort associated with traditional deposit methods.

Enhancing User Experience and Accessibility

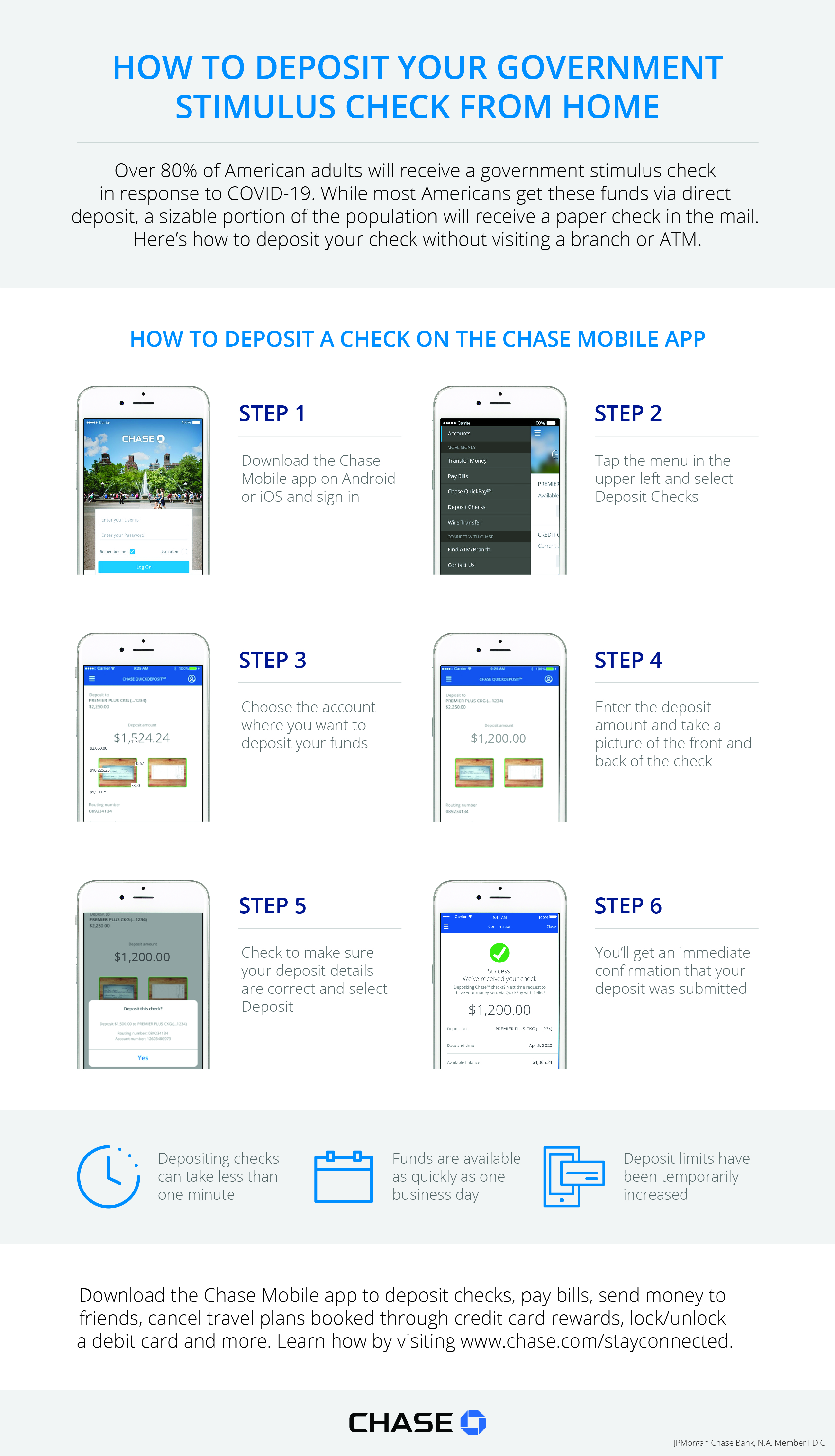

The success of any tech innovation, especially in consumer-facing services, hinges on its user experience (UX) design. Chase Quick Deposit excels in this area, making a complex financial transaction feel intuitive and effortless.

Intuitive Design and Guidance

The mobile application guides users through the deposit process with clear, step-by-step instructions. Visual cues, such as an outline to position the check correctly within the camera frame, and immediate feedback on image quality, simplify the capture process. This reduces user error and the frustration associated with retaking images. The design prioritizes minimal taps and clear calls to action, ensuring that even less tech-savvy individuals can complete a deposit with confidence. This focus on intuitive interaction lowers the barrier to entry for digital banking, expanding its reach to a broader demographic.

Real-Time Feedback and Confirmation

Upon successful image capture and initial processing, users receive immediate on-screen confirmation that their deposit is being reviewed. This instant feedback provides reassurance and transparency, a stark contrast to the uncertainty that might accompany mailing a check or dropping it into an after-hours slot. Further notifications, often via email or in-app alerts, confirm when the deposit has been accepted and when funds are available, keeping the customer informed at every stage. This continuous communication builds trust and confidence in the digital system.

Accessibility for Diverse Users

Beyond convenience, mobile deposit services significantly enhance accessibility. For individuals with disabilities that make branch visits challenging, or those living in areas without easy access to physical banking infrastructure, this technology is transformative. It levels the playing field, ensuring that geographical or physical limitations do not impede access to essential financial services. The ongoing development of mobile banking apps also includes features like screen reader compatibility and adjustable font sizes, further catering to a diverse user base and upholding principles of inclusive design.

Security Protocols and Trust in Digital Transactions

Security is paramount in financial technology, and services like Chase Quick Deposit are built upon multiple layers of protection to safeguard customer funds and data. The trust placed in these digital platforms is directly proportional to the perceived and actual security measures in place.

End-to-End Encryption

As noted, all data transmitted during the Quick Deposit process is encrypted. This end-to-end encryption means that sensitive information is converted into a secure code at the user’s device and remains encrypted until it reaches Chase’s secure servers, rendering it unreadable to unauthorized third parties. This is a foundational security measure against eavesdropping and data breaches during transit.

Multi-Factor Authentication (MFA)

Access to the Chase mobile app and its functionalities, including Quick Deposit, is typically protected by multi-factor authentication. This often involves combining something the user knows (password), something the user has (their phone with a unique identifier or biometric data like fingerprint/face ID), and sometimes something the user is (biometrics). MFA significantly reduces the risk of unauthorized access, even if a user’s password is compromised.

Fraud Monitoring Systems

Beyond initial check validation, sophisticated fraud monitoring systems continuously analyze transactions and account activity. These systems employ machine learning and artificial intelligence to identify unusual patterns or suspicious behaviors that may indicate fraudulent activity. They learn from vast datasets of legitimate and fraudulent transactions, evolving to detect new and emerging threats. This proactive monitoring is a critical line of defense, often flagging issues before they can cause significant harm.

Regulatory Compliance

Chase Quick Deposit adheres to stringent regulatory standards and compliance frameworks, including those set by federal banking authorities and payment networks. These regulations dictate how financial data must be handled, secured, and processed, ensuring consumer protection and the integrity of the financial system. Regular audits and assessments are conducted to ensure ongoing compliance and to adapt to evolving security threats and regulatory landscapes.

The Future Trajectory of Digital Banking Innovation

Chase Quick Deposit is a snapshot of current innovation, but the trajectory of digital banking continues to accelerate. Future enhancements will likely focus on even greater automation, predictive analytics, and personalized services, further integrating banking into the fabric of daily life.

Advanced AI and Machine Learning

The role of AI and machine learning will expand beyond fraud detection. We can expect AI to personalize financial advice, automate budgeting based on spending patterns, and even predict future financial needs, offering tailored products and services proactively. For deposits, AI could potentially enable voice-activated deposits or even integrate with IoT devices, further blurring the lines between physical and digital banking.

Blockchain and Distributed Ledger Technology

While still nascent in mainstream retail banking, blockchain and distributed ledger technology (DLT) hold promise for enhancing security, transparency, and efficiency in interbank settlements and international payments. While not directly applicable to a simple check deposit, the underlying principles could influence how financial data is verified and stored, potentially making transactions even more immutable and resistant to fraud in the long term.

Hyper-Personalization and Embedded Finance

The trend towards hyper-personalization will see banking services become even more context-aware. Imagine a future where your banking app anticipates your need to deposit a refund check from a specific retailer, automatically suggesting the Quick Deposit option as soon as it detects relevant activity. Embedded finance will see banking functionalities integrated directly into non-banking applications, making financial actions an invisible part of other digital experiences.

Chase Quick Deposit exemplifies how strategic application of technology and a deep understanding of user needs can transform established practices. It has set a precedent for convenience, security, and accessibility in personal finance, paving the way for a future where banking is less a task and more an integrated, intelligent part of our digital existence.