The financial world, while seemingly straightforward on the surface, is built upon intricate systems designed to facilitate the seamless movement of money. Among these essential components is the bank sorting code, a vital piece of information that, while perhaps not as widely recognized as an account number, plays a crucial role in domestic banking transactions. Understanding what a bank sorting code is, its purpose, and how it functions is key to demystifying the process of sending and receiving funds within a particular country.

The Fundamentals of Bank Sorting Codes

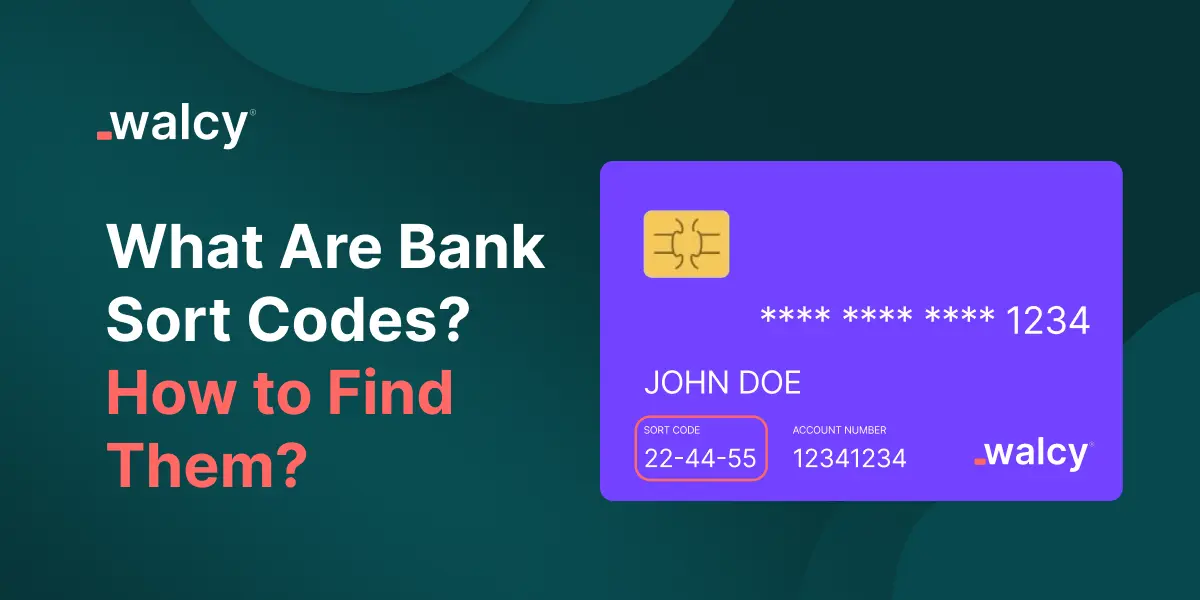

At its core, a bank sorting code is a numerical identifier assigned to financial institutions, specifically their individual branches or offices. Think of it as a postal code for your bank account, but instead of directing mail, it directs financial transfers. These codes are instrumental in routing money accurately and efficiently to the correct bank and branch where an account is held.

Origin and Purpose

The concept of sorting codes emerged from the need for a standardized system to process checks and other payment methods in an increasingly automated banking environment. Before widespread electronic transfers, physical checks were the primary method of payment. Banks needed a way to quickly and accurately sort these checks to the correct destination for processing. The sorting code, alongside the account number, provided this essential information.

Today, even with the dominance of electronic transfers, sorting codes remain fundamental. When you initiate a bank transfer, whether online, via a mobile app, or through a teller, the sorting code is a critical piece of data that the banking system uses to determine which specific institution and branch the funds should be directed to. It ensures that your money doesn’t get lost in transit and reaches the intended recipient’s account without delay.

Structure and Variations

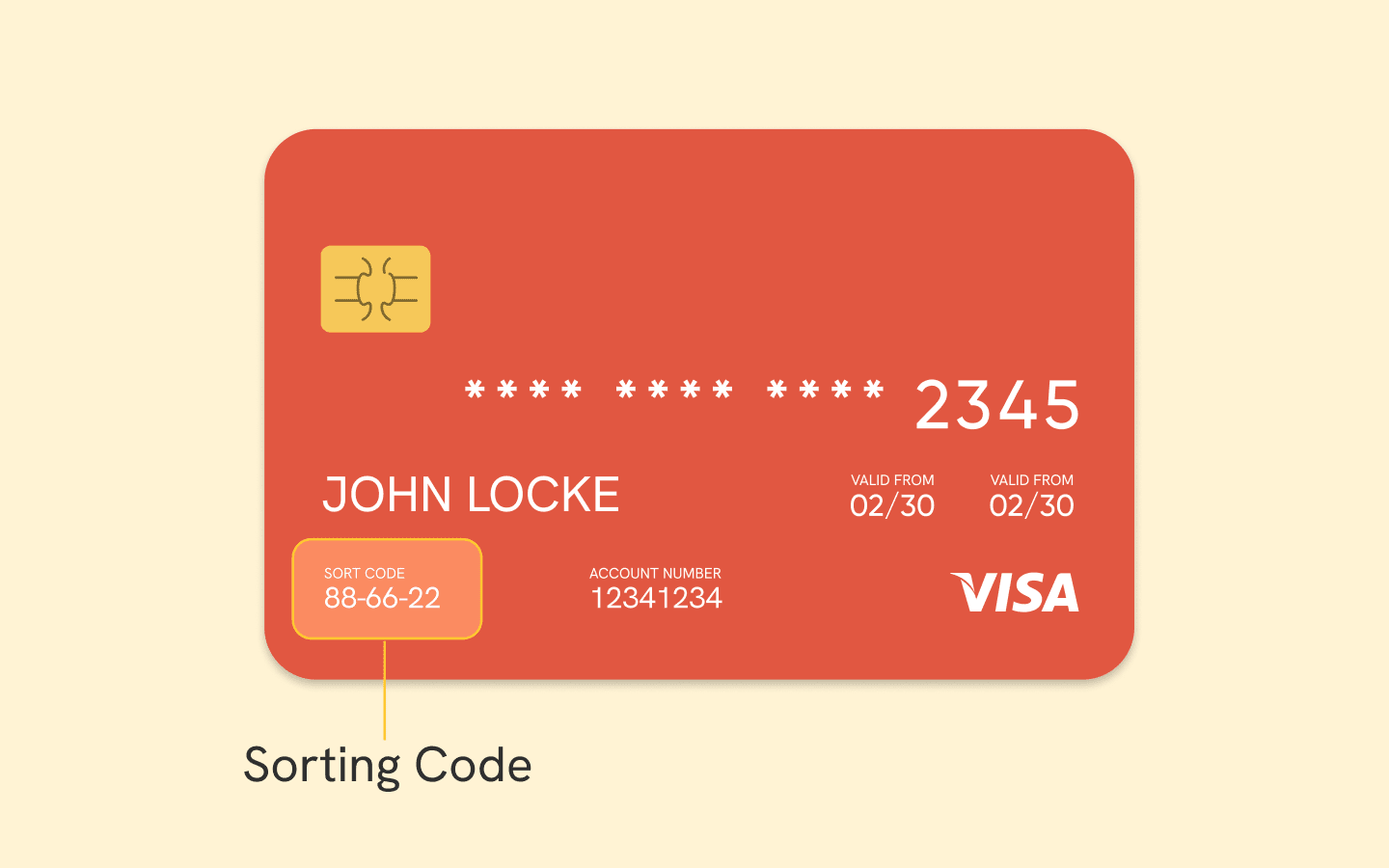

The typical structure of a bank sorting code varies by country. In the United Kingdom, for instance, sorting codes are six digits long, usually presented in a XXXX-XXXX format. These digits are not random; they are systematically assigned. The first two digits often indicate the bank itself, while the subsequent four digits identify the specific branch. This allows banks to manage their branch network efficiently and for the clearing system to process transactions effectively.

In other countries, the structure might differ. For example, in Australia, the Bank Identification Code (BIC) or SWIFT code is more commonly used for international transfers, but domestically, their own systems have their own identifiers. The United States uses the Routing Transit Number (RTN), which is typically nine digits long and also serves the purpose of identifying the financial institution and its location. While the numerical format might differ, the underlying principle remains the same: to uniquely identify a bank and its specific branch for transactional purposes.

Beyond Simple Identification

It’s important to recognize that a sorting code is more than just a random string of numbers. It’s a carefully constructed identifier that forms part of a larger, interconnected financial infrastructure. When you provide a sorting code and an account number, you are essentially giving the banking system a precise address for your funds. This allows for automated clearing houses (ACH) and other payment networks to process transactions with speed and accuracy. Without these codes, the sheer volume of daily transactions would be unmanageable, leading to significant delays and potential errors.

How Bank Sorting Codes Facilitate Transactions

The practical application of bank sorting codes is most evident when initiating or receiving payments. Their role is multifaceted, ensuring security, accuracy, and efficiency in every financial exchange.

Sending Money

When you send money from your account to another, whether it’s a friend, family member, or a business, you will typically be asked for the recipient’s bank sorting code and account number. For domestic transfers, this is the primary routing information.

- Initiation: You log into your online banking, use a mobile app, or visit a branch and specify the recipient’s details, including their sorting code and account number.

- System Routing: The banking system takes this information and, using sophisticated algorithms and databases, identifies the specific bank and branch associated with the provided sorting code.

- Transfer Execution: The funds are then electronically routed to that designated bank and branch.

- Crediting the Account: The recipient’s bank receives the funds and, using the provided account number, credits the money to the correct account.

The sorting code acts as the crucial first step in this journey, ensuring the money is sent to the right place to begin with. If an incorrect sorting code is provided, the transaction will likely fail, or worse, be sent to the wrong account if a similar sorting code exists for another branch or bank.

Receiving Money

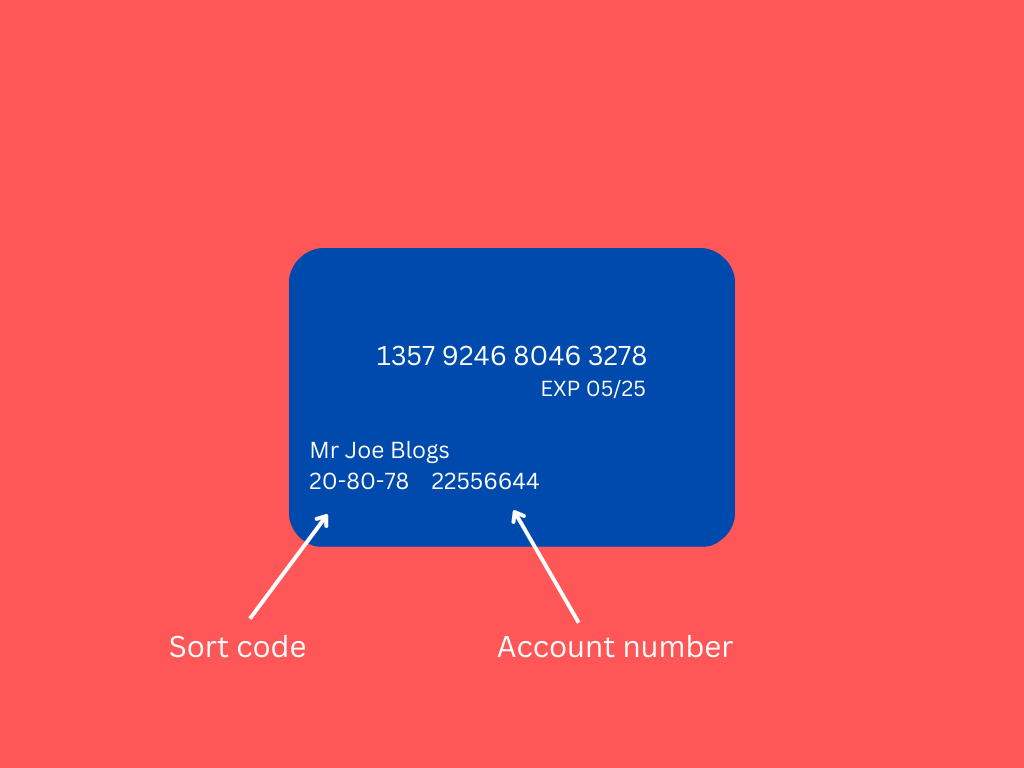

Conversely, when someone sends you money, they will need your bank’s sorting code and your account number. This information is typically found on your bank statements, on your bank’s website, or by contacting your bank directly.

- Information Sharing: You provide your sorting code and account number to the sender.

- Sender’s Action: The sender uses this information to initiate a transfer from their account.

- System Processing: As described above, the banking system uses your sorting code to direct the funds to your bank and branch.

- Deposit: Your bank receives the funds and credits them to your account based on your account number.

This seemingly simple exchange of numbers is the bedrock of most domestic payment systems, enabling a fluid and reliable flow of funds that underpins everyday commerce and personal finance.

The Importance of Accuracy

The efficiency and reliability of the banking system are heavily dependent on the accuracy of the information provided. When it comes to bank sorting codes, even a minor error can have significant consequences.

Common Errors and Their Impact

- Typos: The most common error is a simple typo in one or more digits of the sorting code. This can lead to a transaction being misrouted.

- Incorrect Code: Using a sorting code for the wrong bank or the wrong branch is another frequent mistake. This often occurs when individuals confuse codes for different institutions or branches within the same institution.

- Outdated Information: While less common, banks can occasionally update their sorting codes, especially during mergers or reorganizations. Using an outdated code will result in a failed transaction.

The impact of these errors can range from minor inconveniences to more serious issues:

- Delayed Transactions: The most common outcome of an incorrect sorting code is a delayed transaction. The payment system will often flag the transaction as problematic, requiring manual intervention or rejection.

- Returned Funds: In many cases, if a transaction cannot be successfully routed due to an incorrect sorting code, the funds will be returned to the sender’s account. This can cause frustration and necessitate resubmission of the payment.

- Misdirected Funds: In the worst-case scenario, an incorrect sorting code might accidentally direct funds to an entirely different account. While banks have protocols to prevent this and recover misdirected funds, it can be a complex and time-consuming process for all parties involved. Recovering these funds can be challenging and may involve legal processes, especially if the recipient of the misdirected funds is unwilling to return them.

Verification and Best Practices

To avoid these issues, it’s crucial to exercise diligence when dealing with bank sorting codes:

- Double-Check: Always double-check the sorting code before submitting a transaction. Ensure each digit is correct and in the right order.

- Official Sources: Obtain the sorting code directly from the recipient or from official bank documentation. Avoid relying on memory or unofficial lists found online, as these may be outdated.

- Bank Websites: Most banks provide a tool on their website to look up their sorting codes. This is a reliable way to verify the correct code for a specific branch.

- Contact the Bank: If you are unsure about a sorting code, contact the bank directly. They will be able to provide the accurate information.

- Use Account Verification Services: Some payment platforms offer account verification services that can cross-reference sorting codes and account numbers to help prevent errors before a transaction is finalized.

Sorting Codes in the Context of Modern Banking

While the fundamental purpose of sorting codes remains unchanged, their integration into modern banking systems has evolved significantly, becoming even more crucial in the digital age.

The Role in Electronic Payments

With the advent of Faster Payments, Bacs, and other electronic payment systems, the speed at which money moves has increased dramatically. Sorting codes are integral to the efficiency of these systems. They allow for automated routing of payments at high volumes, ensuring that transfers initiated moments ago can be credited to the recipient’s account within minutes or hours, rather than days. The digital infrastructure of modern banking relies on these precise identifiers to perform the complex choreography of fund movements across different institutions and branches.

International vs. Domestic Transfers

It’s important to distinguish between sorting codes and international payment identifiers. Sorting codes are primarily used for domestic transfers within a specific country. For international money transfers, different systems are employed, such as the SWIFT (Society for Worldwide Interbank Financial Telecommunication) network, which uses BIC (Bank Identifier Code) or SWIFT codes. These codes are longer and more globally standardized to facilitate cross-border transactions. While a BIC/SWIFT code identifies a bank globally, a sorting code identifies a specific branch within a country’s domestic banking system.

Security and Fraud Prevention

While sorting codes themselves are not directly a security feature in the sense of encryption, their accuracy contributes to the overall security of the banking system. By ensuring that funds are directed to the intended recipient’s account, sorting codes help prevent fraudulent diversions of money. When combined with other security measures, such as multi-factor authentication for online banking and the unique nature of account numbers, the sorting code forms another layer in a robust system designed to protect financial assets. Banks also use sorting codes in conjunction with account numbers and other data to flag suspicious transaction patterns, which can be an early indicator of fraud.

In conclusion, the bank sorting code, though a simple six-digit number in many regions, is a cornerstone of modern domestic banking. It is the silent, efficient mechanism that ensures your money reaches its intended destination with speed and accuracy. Understanding its function, verifying its correctness, and appreciating its role in the broader financial ecosystem are essential for anyone engaging in financial transactions. It is a testament to the power of standardization and precise identification in creating a seamless and reliable banking experience.