The term “balance credit card” is often encountered in discussions about personal finance, credit management, and the strategic use of credit to optimize financial health. While not a specific product branded as a “Balance Credit Card” by a single issuer, it refers to a type of credit card feature or a strategic approach to using credit cards, primarily focused on managing existing debt. Understanding this concept is crucial for anyone looking to improve their credit score, reduce interest payments, or gain more control over their financial obligations.

At its core, a balance credit card revolves around the transfer of outstanding debt from one or more credit cards to a new credit card. This is most commonly facilitated through a “balance transfer” promotion, which is a feature offered by many credit card companies. The primary allure of such a feature is the opportunity to consolidate multiple credit card debts into a single payment, often with a significantly lower introductory interest rate. This can be a powerful tool for debt reduction and financial restructuring.

Understanding the Mechanics of Balance Transfers

The concept of a balance transfer is relatively straightforward. Imagine you have a significant amount of debt spread across two or three credit cards, each with a different interest rate, some of which might be quite high. You can apply for a new credit card that advertises a balance transfer option. If approved, you provide the details of your existing credit card accounts, and the new credit card issuer will pay off those balances. Your debt is then consolidated onto the new card.

The Introductory Offer: The Main Draw

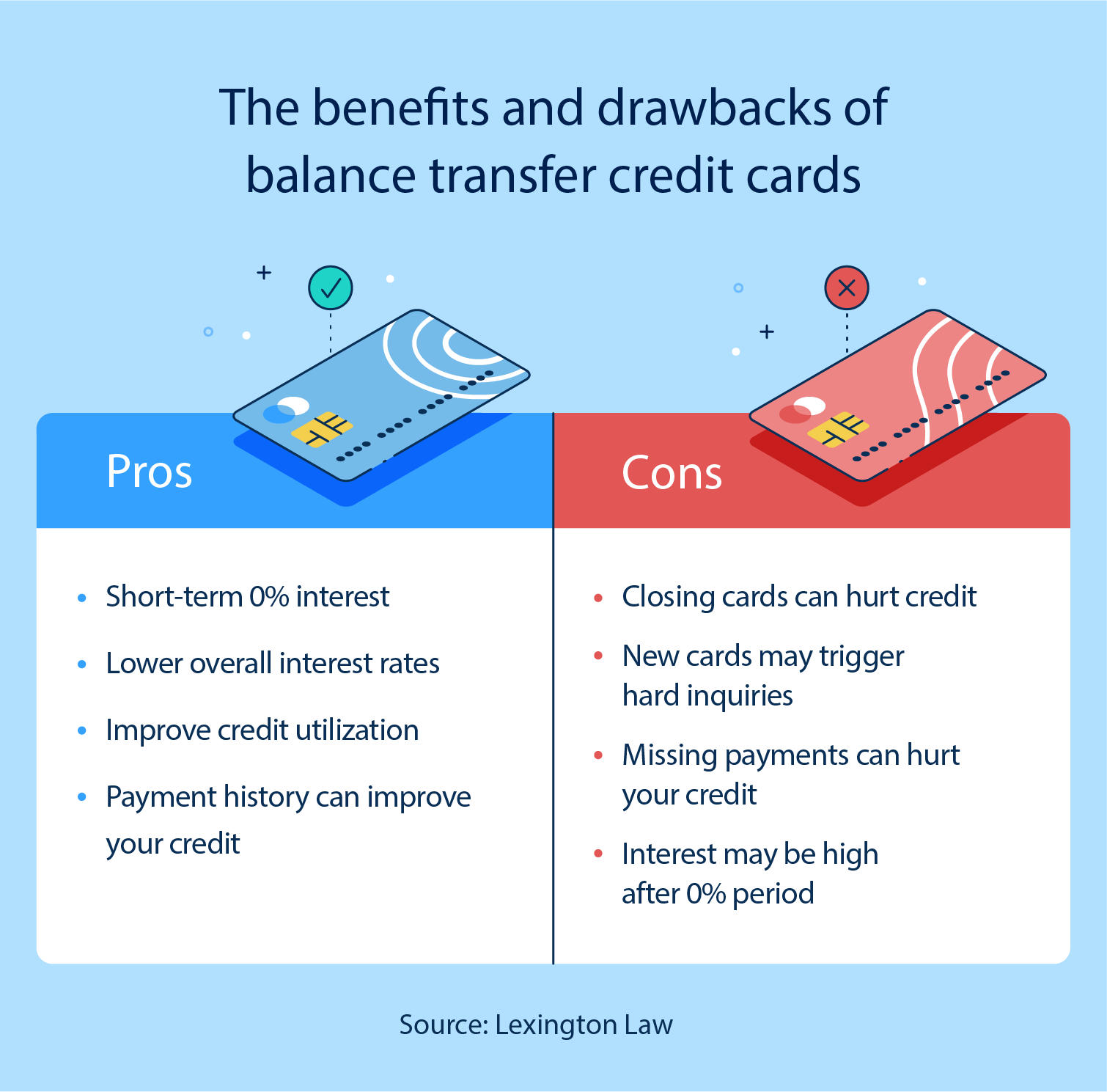

The most significant aspect of a balance transfer offer is the introductory Annual Percentage Rate (APR). Many credit cards will offer a 0% APR for a promotional period, which can range from six months to 18 months or even longer. This means that for the duration of the introductory period, any payments you make towards your transferred balance will go directly towards reducing the principal amount of your debt, rather than being consumed by interest charges. This is a substantial benefit, especially if you are carrying a large balance on high-interest cards.

Fees Associated with Balance Transfers

It’s important to note that balance transfers are not entirely free. Most credit card issuers charge a balance transfer fee, typically a percentage of the amount transferred. This fee can range from 3% to 5% of the transferred balance. For example, if you transfer $10,000, a 3% fee would cost you $300. This fee should be factored into the overall cost-effectiveness of a balance transfer. If the savings from the 0% APR outweigh the fee, then it can be a worthwhile strategy.

The Post-Introductory APR

Once the introductory 0% APR period expires, the remaining balance on the new credit card will be subject to the card’s standard variable APR. This is a critical point to consider. If you haven’t managed to pay off the entire transferred balance by the end of the promotional period, you will start accruing interest at the regular rate. These rates can be substantial, so it’s imperative to have a clear plan for paying down the debt during the 0% APR window.

Strategic Applications of Balance Credit Cards

The strategic use of balance credit cards can be incredibly beneficial when approached with a well-defined plan. It’s not simply about moving debt around; it’s about using the grace period of a low or 0% APR to aggressively tackle outstanding balances.

Debt Consolidation and Simplification

One of the primary benefits is debt consolidation. Instead of juggling multiple due dates and minimum payments for several different credit cards, you have a single statement and a single payment to manage. This can significantly reduce the mental burden and the risk of late payments, which can incur fees and damage your credit score.

Accelerated Debt Reduction

When you transfer a high-interest balance to a card with a 0% introductory APR, every dollar you pay goes directly towards reducing the principal. This accelerates your debt repayment timeline considerably compared to paying down the debt on a high-interest card where a large portion of your payment is eaten up by interest. This can save you a significant amount of money in interest charges over time.

Improving Credit Score

By consolidating debt and making on-time payments on the new card, you can positively impact your credit score. Reducing the overall utilization ratio (the amount of credit you’re using compared to your total available credit) is a key factor in credit scoring. By transferring balances and then diligently paying them down, you can lower this ratio, which is a strong indicator to credit bureaus that you are managing your credit responsibly.

Utilizing a Financial “Breather”

A balance transfer can provide a much-needed financial “breather.” It allows you to pause the relentless accumulation of interest on your existing debt and focus your resources on eliminating the principal. This can be particularly helpful during periods of financial strain or when you’re working towards a specific savings goal.

Considerations and Potential Pitfalls

While balance credit cards offer significant advantages, they are not without their potential drawbacks. A lack of careful planning or understanding can lead to more debt rather than less.

The Temptation to Overspend

One of the most significant risks is the temptation to overspend on the old cards that are now clear of their balances, or even on the new card itself. The 0% APR can create a false sense of financial security. It’s crucial to maintain discipline and continue spending responsibly, treating the transferred balance as a strict debt repayment target.

Missing the Introductory Period Deadline

As mentioned earlier, the transition from a 0% APR to a standard variable APR can be costly if you haven’t cleared the balance. It’s vital to be aware of the exact end date of the introductory offer and to have a concrete payment plan in place to pay off as much of the balance as possible before that date.

Balance Transfer Fees vs. Interest Savings

Always calculate whether the balance transfer fee is worth the interest savings. If the amount of interest you would have paid on the old cards during the introductory period is less than the balance transfer fee, it might not be financially advantageous.

Credit Score Requirements

To qualify for a balance transfer offer, particularly those with the most attractive 0% APR periods, you typically need a good to excellent credit score. Issuers want to see a history of responsible credit management. If your credit score is lower, you may be offered a card with a less appealing introductory rate or higher fees.

Not All Purchases Qualify

Balance transfer offers specifically apply to transferring existing debt. New purchases made on the card may not qualify for the introductory 0% APR and might accrue interest at the standard purchase APR from day one, or have a separate introductory purchase APR.

How to Effectively Use a Balance Credit Card

To maximize the benefits and minimize the risks associated with balance credit cards, a strategic approach is paramount.

Step 1: Assess Your Current Debt

Before applying for a new card, thoroughly review your existing credit card debt. Note the balances, interest rates, and minimum payments for each card. This will help you understand how much you can save by transferring the debt.

Step 2: Research Balance Transfer Offers

Shop around for balance transfer offers from various credit card issuers. Compare the length of the introductory 0% APR period, the balance transfer fee, the standard APR after the introductory period, and any other card benefits. Look for offers that provide the longest 0% APR period possible to give you ample time to pay down the debt.

Step 3: Calculate the True Cost

Factor in the balance transfer fee. If you transfer $5,000 with a 3% fee, that’s $150. Determine if the interest you would pay on that $5,000 over the introductory period on your old cards would exceed this fee. Use online calculators or spreadsheets to estimate potential savings.

Step 4: Create a Strict Repayment Plan

Once you’ve secured a balance transfer card, create a realistic and aggressive repayment plan. Divide the transferred balance by the number of months in the introductory period to determine the minimum monthly payment required to pay off the entire balance before the 0% APR expires. Aim to pay more than this minimum if possible.

Step 5: Avoid New Debt Accumulation

Resist the urge to use your old credit cards or the new balance transfer card for new purchases that will add to your debt. Treat the balance transfer card as a debt repayment tool, not an extension of your spending power.

Step 6: Monitor Your Credit

Keep an eye on your credit reports and scores throughout the process. Making consistent, on-time payments will generally improve your creditworthiness.

![]()

Conclusion

The “balance credit card” concept, primarily manifested through balance transfer offers, is a powerful financial tool when used strategically. It offers a pathway to significant interest savings and accelerated debt reduction by consolidating existing balances onto a new card, often with a 0% introductory APR. However, its effectiveness hinges on careful planning, disciplined spending, and a commitment to paying down the debt before the promotional period ends. By understanding the fees, potential pitfalls, and employing a rigorous repayment strategy, individuals can leverage balance credit cards to take a substantial step towards financial well-being and a healthier credit profile. It’s a tactic that, when executed correctly, transforms debt management from a burden into an opportunity for financial improvement.