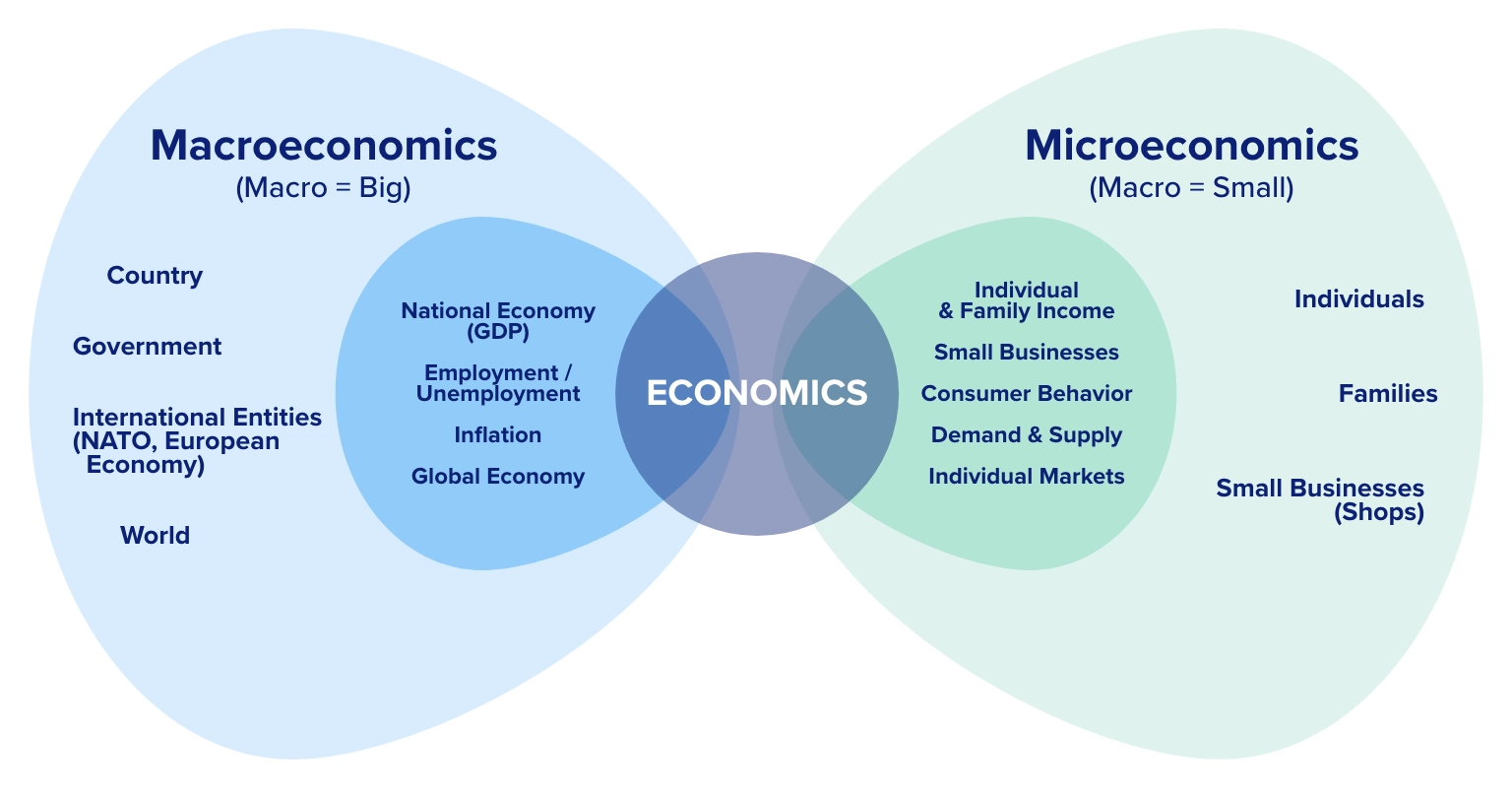

AP Economics, or Advanced Placement Economics, is a rigorous college-level curriculum designed to introduce high school students to the fundamental principles of economics. This subject area is broadly divided into two distinct but interconnected courses: AP Macroeconomics and AP Microeconomics. Both aim to equip students with a sophisticated understanding of how economies function, from the smallest individual and firm decisions to the grandest national and global trends. The skills honed in AP Econ extend far beyond memorization; they involve critical thinking, data analysis, and the ability to apply economic theory to real-world scenarios. This analytical foundation is invaluable, preparing students not only for further academic pursuits in economics, business, or finance, but also for informed citizenship in an increasingly complex global marketplace.

AP Macroeconomics: The Big Picture

AP Macroeconomics focuses on the aggregate economy, examining the economy as a whole. It delves into the study of national income, unemployment, inflation, and the factors that influence economic growth and stability. Students learn to analyze the behavior of the entire economy and the policies governments and central banks use to manage it.

National Income and Product Accounts

A core component of macroeconomics is understanding how we measure the health of a nation’s economy. This involves the study of the National Income and Product Accounts (NIPA), which track the overall production of goods and services.

Gross Domestic Product (GDP)

Gross Domestic Product (GDP) is the most widely cited measure of a nation’s economic output. It represents the total market value of all final goods and services produced within a country in a given period. AP Macroeconomics students learn to calculate GDP using the expenditure approach (C + I + G + NX), the income approach, and the production (or value-added) approach. Understanding the components of GDP allows for analysis of economic activity and its drivers.

Nominal vs. Real GDP

A crucial distinction is made between nominal and real GDP. Nominal GDP is calculated using current prices, while real GDP adjusts for inflation, providing a more accurate picture of changes in the actual volume of goods and services produced. This distinction is vital for understanding economic growth over time and for making meaningful comparisons.

The GDP Deflator

The GDP deflator is a price index that measures the average level of prices for all new, domestically produced, final goods and services in an economy. It is derived by dividing nominal GDP by real GDP and multiplying by 100. The GDP deflator is used to convert nominal GDP into real GDP and is a key indicator of inflation.

Economic Growth and Productivity

Long-term economic growth is a primary concern in macroeconomics. This involves understanding the factors that contribute to increased output per capita over time.

The Production Function

The production function, often represented as Y = f(K, L, A), illustrates the relationship between inputs (capital, labor, and technology/land) and output. AP Macroeconomics explores how increases in these inputs, particularly through investment in physical capital, human capital, and technological advancements, can lead to sustained economic growth.

Productivity and its Determinants

Productivity, defined as output per unit of input, is the engine of long-run economic growth and rising living standards. Students learn about the factors that enhance productivity, including education and training (human capital), the stock of equipment and structures (physical capital), technology, and natural resources.

Unemployment and Inflation

These are two of the most significant challenges faced by national economies. AP Macroeconomics provides the tools to understand their causes, consequences, and potential policy responses.

Unemployment

Unemployment refers to individuals who are actively seeking employment but are unable to find work. The course examines different types of unemployment: frictional (due to normal job turnover), structural (due to mismatches in skills or location), and cyclical (due to downturns in the business cycle). The natural rate of unemployment, the sum of frictional and structural unemployment, is a key concept.

Inflation

Inflation is a sustained increase in the general price level of goods and services in an economy over a period of time. AP Macroeconomics investigates the causes of inflation, including demand-pull inflation (excess aggregate demand) and cost-push inflation (rising production costs). The impacts of inflation on purchasing power, investment, and income distribution are also analyzed.

Aggregate Demand and Aggregate Supply

These models are central to macroeconomic analysis, explaining the overall price level and output in an economy.

Aggregate Demand (AD)

Aggregate Demand represents the total demand for goods and services in an economy at a given price level. The AD curve slopes downward, reflecting the wealth effect, interest rate effect, and exchange rate effect. Factors that shift the AD curve include changes in consumption, investment, government spending, and net exports.

Aggregate Supply (AS)

Aggregate Supply represents the total supply of goods and services that firms in a national economy plan on producing during a specific time period. The short-run aggregate supply (SRAS) curve is upward sloping, while the long-run aggregate supply (LRAS) curve is vertical, representing the economy’s full employment output. Shifts in the AS curve are driven by changes in input prices, productivity, and government policies.

Monetary and Fiscal Policy

Governments and central banks employ various tools to influence macroeconomic outcomes.

Monetary Policy

Monetary policy is conducted by central banks, such as the Federal Reserve in the United States. It involves managing the money supply and interest rates to achieve macroeconomic objectives like stable prices and maximum employment. Key tools include open market operations, the reserve requirement, and the discount rate.

Fiscal Policy

Fiscal policy is enacted by the government and involves the use of government spending and taxation to influence the economy. Expansionary fiscal policy (increased spending, reduced taxes) aims to boost aggregate demand during recessions, while contractionary fiscal policy (decreased spending, increased taxes) aims to curb inflation.

AP Microeconomics: The Individual and Firm Perspective

AP Microeconomics zooms in on the behavior of individual economic agents – households and firms – and their interactions in markets. It explores how prices are determined, how resources are allocated, and how markets can lead to efficiency or, at times, market failures.

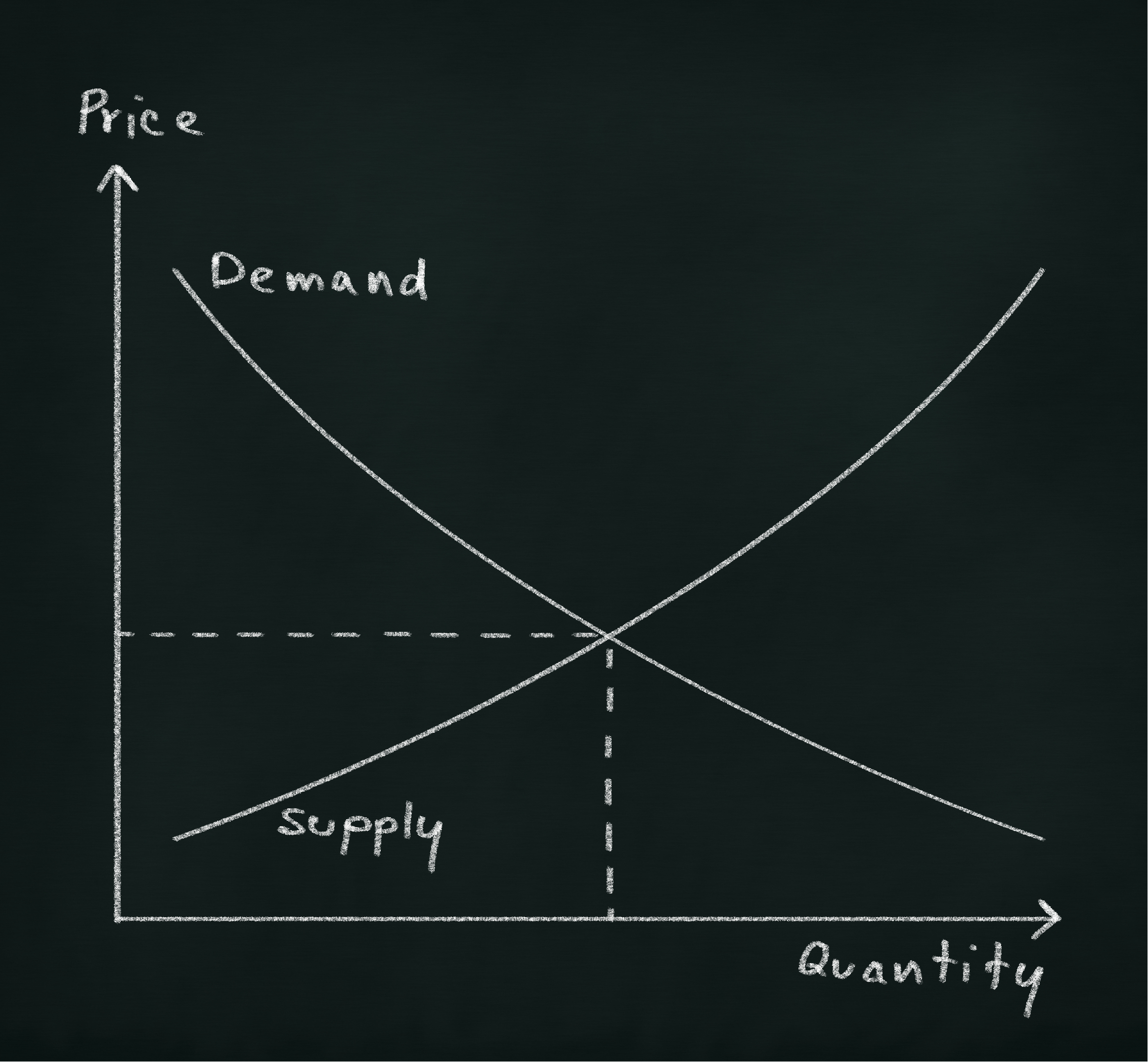

The Fundamentals of Supply and Demand

The cornerstone of microeconomic analysis is the interaction of supply and demand in individual markets.

Demand

Demand represents the quantity of a good or service that consumers are willing and able to purchase at various prices. The law of demand states that, ceteris paribus, as the price of a good falls, the quantity demanded rises, and vice versa. Factors that shift the demand curve include changes in consumer income, the prices of related goods (substitutes and complements), consumer tastes and preferences, expectations, and the number of buyers.

Supply

Supply represents the quantity of a good or service that producers are willing and able to offer for sale at various prices. The law of supply states that, ceteris paribus, as the price of a good rises, the quantity supplied rises, and vice versa. Factors that shift the supply curve include changes in input prices, technology, government policies (taxes and subsidies), the number of sellers, and expectations.

Market Equilibrium

Market equilibrium occurs at the price where the quantity demanded equals the quantity supplied. This intersection point determines the equilibrium price and equilibrium quantity. Deviations from equilibrium create surpluses (when price is above equilibrium) or shortages (when price is below equilibrium), which market forces tend to correct.

Elasticity

Elasticity measures the responsiveness of one variable to a change in another. In microeconomics, understanding elasticity is crucial for analyzing market behavior.

Price Elasticity of Demand

Price elasticity of demand measures how much the quantity demanded of a good responds to a change in its price. It is calculated as the percentage change in quantity demanded divided by the percentage change in price. Goods with highly elastic demand are sensitive to price changes, while those with inelastic demand are not.

Price Elasticity of Supply

Price elasticity of supply measures how much the quantity supplied of a good responds to a change in its price. It is calculated as the percentage change in quantity supplied divided by the percentage change in price.

Income Elasticity of Demand and Cross-Price Elasticity of Demand

These concepts analyze how demand changes with income (normal vs. inferior goods) and the price of other goods (substitutes vs. complements), respectively.

Consumer Behavior

Microeconomics examines how consumers make choices to maximize their utility, given their budget constraints.

Utility

Utility refers to the satisfaction or benefit a consumer derives from consuming a good or service.

Marginal Utility

Marginal utility is the additional satisfaction gained from consuming one more unit of a good. The law of diminishing marginal utility states that as a consumer consumes more of a good, the marginal utility gained from each additional unit tends to decrease.

Budget Constraints and Consumer Choice

Consumers face budget constraints, meaning they can only purchase combinations of goods that they can afford. Consumer choice involves finding the combination of goods that maximizes utility subject to the budget constraint.

Producer Behavior and Market Structures

AP Microeconomics analyzes how firms make decisions regarding production and pricing in different market structures.

Costs of Production

Firms incur various costs to produce goods and services. These include fixed costs (which do not vary with output) and variable costs (which vary with output). Total cost is the sum of fixed and variable costs.

Marginal Cost and Average Costs

Marginal cost is the additional cost of producing one more unit of output. Average total cost, average fixed cost, and average variable cost are also key measures. Firms aim to produce at a level where marginal cost equals marginal revenue to maximize profits.

Market Structures

Microeconomics identifies four main market structures:

- Perfect Competition: Characterized by a large number of small firms selling identical products, with no barriers to entry or exit. Firms are price takers.

- Monopoly: A single seller of a unique product with no close substitutes and significant barriers to entry. The monopolist is a price maker.

- Monopolistic Competition: Many firms selling differentiated products, with relatively easy entry and exit.

- Oligopoly: A few large firms dominate the market, with significant barriers to entry and interdependence among firms’ decisions.

Market Failures and Government Intervention

While markets are often efficient, they can sometimes fail to allocate resources optimally.

Externalities

Externalities occur when the production or consumption of a good affects a third party not directly involved in the transaction. Positive externalities (e.g., vaccination) benefit society, while negative externalities (e.g., pollution) impose costs.

Public Goods

Public goods are non-excludable (difficult to prevent people from consuming them) and non-rivalrous (one person’s consumption does not diminish another’s). The market often under-provides public goods due to the free-rider problem.

Information Asymmetry

When one party in a transaction has more or better information than the other, it can lead to market inefficiencies (e.g., adverse selection and moral hazard).

Government Intervention

Governments can intervene to correct market failures through policies such as taxes, subsidies, regulation, and the provision of public goods. However, government intervention can also create inefficiencies.

In conclusion, AP Economics offers a comprehensive introduction to the study of how societies allocate scarce resources. Whether focusing on the grand sweep of national economies in AP Macroeconomics or the intricate workings of individual markets and decision-makers in AP Microeconomics, the courses provide students with a powerful analytical framework for understanding the economic forces that shape our world.