The realm of car insurance is often perceived as a complex tapestry of risk assessment, premium calculations, and coverage options. Within this intricate framework, the concept of anti-theft devices plays a significant, albeit sometimes overlooked, role. These technological and mechanical deterrents are not merely add-ons; they represent a proactive approach to mitigating the risk of vehicle theft, a factor that directly influences insurance premiums and policy terms. Understanding what constitutes an anti-theft device in the context of car insurance requires a deep dive into their types, their efficacy, and how insurers evaluate their impact on underwriting decisions.

The Multifaceted Landscape of Anti-Theft Devices

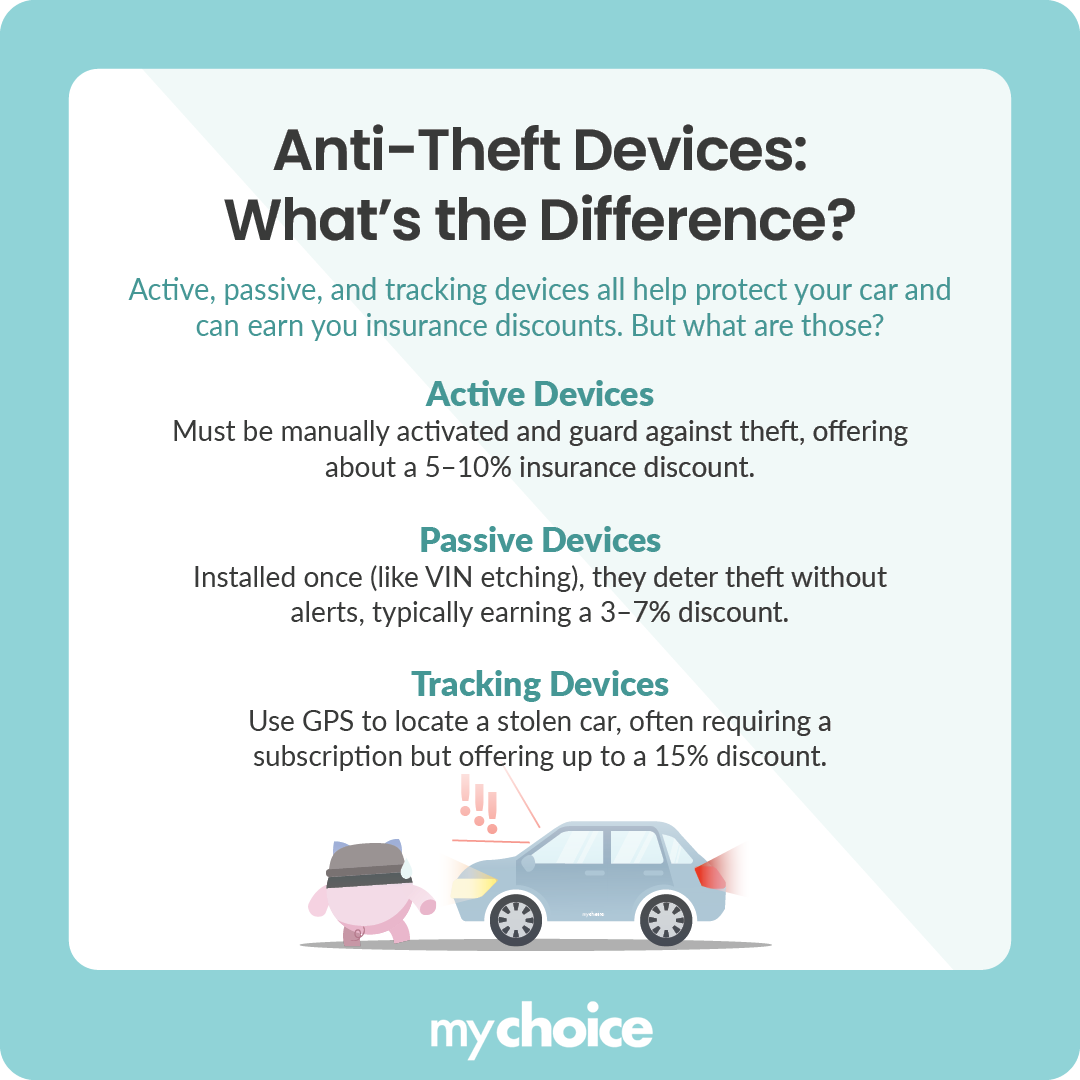

Anti-theft devices encompass a broad spectrum of technologies and mechanisms designed to prevent unauthorized access, disable a vehicle’s operation, or facilitate its recovery in the event of a theft. Insurers generally categorize these devices based on their primary function and their level of sophistication. This categorization is crucial because it allows them to assess the potential reduction in risk associated with each type of device.

Immobilization Systems

Perhaps the most prevalent category of anti-theft devices are those designed to immobilize a vehicle, rendering it inoperable without the proper authorization.

Factory-Installed Immobilizers

Most modern vehicles come equipped with factory-installed engine immobilizers as standard. These systems typically utilize a transponder chip embedded within the ignition key or key fob. When the key is inserted into the ignition (or the fob is present in the vehicle), the car’s computer system reads a unique code from the chip. If the code matches the code stored in the vehicle’s immobilizer module, the engine control unit (ECU) will allow the engine to start and run. If an unauthorized key or a key with a blank chip is used, the immobilizer will prevent the fuel pump, ignition system, or starter motor from engaging, effectively immobilizing the vehicle. Insurers view these systems as a fundamental layer of security, contributing to a baseline reduction in theft risk.

Aftermarket Immobilizers

Beyond factory-fitted systems, a variety of aftermarket immobilizers are available. These can range from simple kill switches, which interrupt a vital electrical circuit (like the fuel pump or ignition), to more complex electronic systems that require a specific code or a unique key fob to disarm. Some advanced aftermarket immobilizers can also incorporate motion sensors or tilt sensors, triggering an alarm if the vehicle is tampered with while the immobilizer is active. The effectiveness of aftermarket immobilizers can vary widely depending on the quality of installation and the sophistication of the system itself. Insurers will often require proof of installation by a certified professional for these systems to be considered for premium discounts.

Tracking and Recovery Systems

Another significant category of anti-theft devices focuses on locating a stolen vehicle and aiding in its recovery. These systems leverage various technologies to transmit the vehicle’s location to authorized personnel or owners.

GPS Tracking Devices

Global Positioning System (GPS) technology has revolutionized vehicle recovery. GPS tracking devices, often discreetly installed within the vehicle, utilize satellite signals to pinpoint the vehicle’s exact location. This data is then transmitted wirelessly to a monitoring center or directly to the owner’s smartphone or computer. When a vehicle is reported stolen, law enforcement can use the real-time location data to track and apprehend the thieves and recover the vehicle. The speed and accuracy of GPS tracking significantly enhance the chances of recovery, thereby reducing the overall financial loss for both the owner and the insurance company.

LoJack and Similar Systems

Systems like LoJack employ radio frequency (RF) technology in conjunction with GPS. While traditional GPS systems rely on satellite signals, RF-based trackers can often operate in areas where GPS signals may be weak or blocked, such as enclosed parking garages. LoJack units communicate with a network of police-equipped receivers. When a vehicle equipped with a LoJack system is reported stolen, police can activate the unit remotely, and the receiver can detect the signal, guiding officers to the vehicle’s location. The combination of technologies in some advanced tracking systems offers a robust solution for vehicle recovery.

Telematic Systems

Modern telematic systems, often integrated into vehicle infotainment systems or offered as standalone devices, combine GPS tracking with other data collection capabilities. These systems can monitor driving behavior, speed, and location, and in the event of a theft, the tracking component can be activated to locate the vehicle. The data collected by telematic systems can also be used by insurers to assess driver behavior, potentially leading to usage-based insurance programs.

Alarm and Deterrent Systems

While not always capable of preventing a theft outright, alarm and deterrent systems are designed to draw attention to the unauthorized use of a vehicle and scare off potential thieves.

Vehicle Alarms

Standard car alarms are typically triggered by physical disturbances, such as doors being opened, windows being broken, or the vehicle being jolted. These alarms emit loud audible sirens and may also flash the vehicle’s lights to attract attention. While a basic alarm might deter a casual thief, more determined criminals may disregard them. More sophisticated alarms can incorporate features like shock sensors, glass breakage sensors, and even tilt sensors.

Audible and Visual Deterrents

Beyond traditional alarms, various deterrents aim to make a vehicle a less attractive target. These can include steering wheel locks, pedal locks, and VIN etching (permanently marking the vehicle’s identification number onto its windows and other parts). While these are often considered visible deterrents, their effectiveness can be limited by the determination of the thief.

Advanced Security Technologies

The evolution of automotive technology has also led to more integrated and advanced anti-theft solutions.

Keyless Entry and Start Systems with Enhanced Security

While convenient, keyless entry and start systems have also presented new vulnerabilities, primarily through relay attacks where thieves amplify the signal from a key fob inside a home to unlock and start the car. Manufacturers are increasingly implementing more robust security measures, such as rolling codes for fobs that change with each use and proximity sensors that disable the system when the fob is not within a certain range. Insurers are keenly aware of these advancements and may offer discounts for vehicles equipped with the latest, more secure keyless entry technologies.

Biometric Authentication

Emerging technologies are exploring the integration of biometric authentication, such as fingerprint scanners or facial recognition, as a means of authorizing vehicle ignition. While still not widespread, these systems offer a highly secure method of preventing unauthorized access, as they are tied to the individual’s unique biological traits. As these technologies mature, they are likely to become a significant factor in insurance risk assessment.

The Insurance Perspective: Why Anti-Theft Devices Matter

Insurance companies view anti-theft devices not just as security features but as tangible risk mitigation tools. The presence of such devices can directly influence the likelihood of a vehicle being stolen, the cost associated with a theft (e.g., recovery expenses), and the overall financial exposure for the insurer.

Risk Reduction and Premium Discounts

The primary way anti-theft devices impact car insurance is through potential premium discounts. Insurers operate on the principle of pooling risk; they charge premiums to cover the potential for losses. If a device demonstrably reduces the risk of a specific loss – in this case, vehicle theft – then it logically follows that the associated premium should be reduced.

The extent of the discount often correlates with the perceived effectiveness of the device. Factory-installed immobilizers and advanced GPS tracking systems are typically more likely to garner significant discounts than basic audible alarms or visible deterrents. Insurers often have specific lists of approved anti-theft devices and may require documentation or verification of installation and functionality.

Classification and Underwriting

During the underwriting process, insurance companies classify vehicles based on various factors, including make, model, year, and the presence of security features. Vehicles equipped with robust anti-theft systems are often categorized as lower risk. This classification can lead to more favorable insurance rates and even access to broader coverage options that might not be available for high-risk vehicles.

Conversely, vehicles with a known history of being targeted by thieves and lacking adequate security measures may face higher premiums or may be considered uninsurable by some companies. The investment in an anti-theft device can therefore be seen as an investment in both personal security and financial savings on insurance.

Enhanced Recovery Prospects

In the unfortunate event of a vehicle theft, the presence of an effective tracking and recovery system significantly increases the chances of the vehicle being found quickly and undamaged. This rapid recovery minimizes the financial loss for the insurance company. Instead of a total loss claim, the insurer may only be liable for temporary damage sustained during the theft or for the cost of recovery. This increased likelihood of recovery translates into a more favorable risk profile for the insured vehicle.

Compliance and Policy Requirements

While less common for standard passenger vehicles, certain types of vehicles or vehicles used for specific purposes might have anti-theft device requirements stipulated by their insurance policies. For example, high-value classic cars, exotic vehicles, or commercial fleets might be mandated to have certain security systems in place as a condition of coverage. Failure to comply with these requirements could lead to denied claims or policy cancellation.

Choosing and Verifying Anti-Theft Devices for Insurance Purposes

Selecting the right anti-theft device and ensuring it is recognized by your insurance provider is a two-fold process. It requires understanding your vehicle’s vulnerabilities and communicating effectively with your insurer.

Researching Device Effectiveness

Before purchasing an anti-theft device, it is prudent to research its effectiveness. Look for devices that have a proven track record, are recommended by reputable consumer organizations, and ideally, are certified by industry standards. Consider not only the prevention capabilities but also the recovery potential, especially for GPS tracking systems.

Consulting Your Insurance Provider

The most critical step is to consult with your insurance provider before or shortly after installing an anti-theft device. Inquire about:

- Eligible Devices: Ask if they have a list of approved devices that qualify for discounts.

- Discount Amounts: Understand the percentage or dollar amount of the premium reduction associated with specific devices.

- Verification Process: Determine what documentation or proof of installation is required. This might include invoices from certified installers, device serial numbers, or certificates of authenticity.

- Policy Limitations: Be aware of any limitations or exclusions related to anti-theft devices in your policy.

Professional Installation

For most sophisticated anti-theft systems, professional installation is highly recommended and often a prerequisite for insurance discounts. Certified installers ensure that the device is correctly integrated into the vehicle’s electrical system and functions optimally. Improper installation can not only render the device ineffective but may also void the vehicle’s warranty or even create safety hazards.

Maintaining Device Functionality

It is essential to ensure that your anti-theft device remains functional throughout the life of your policy. This may involve periodic maintenance, software updates for electronic systems, or ensuring that tracking devices have active subscriptions. If a device malfunctions and is not repaired or replaced, you could lose any associated discounts, and your vehicle’s risk profile might change.

In conclusion, anti-theft devices are a vital component in the equation of car insurance. They represent a tangible commitment by vehicle owners to protect their property, a commitment that insurers recognize and reward through reduced premiums and more favorable policy terms. By understanding the various types of devices available, their impact on risk, and the importance of consulting with your insurance provider, you can leverage these technologies to enhance your vehicle’s security and potentially lower your insurance costs.