Understanding the Core Concept of Required Minimum Distributions (RMDs)

Required Minimum Distributions (RMDs) represent a crucial aspect of retirement planning, particularly for individuals who have accumulated wealth in tax-deferred retirement accounts. These mandated withdrawals are not merely a suggestion but a regulatory imperative designed to ensure that the government eventually collects taxes on these deferred savings. For those engaged in the dynamic world of tech and innovation, understanding RMDs is paramount, as wealth often accrues rapidly in various investment vehicles, necessitating careful planning to avoid significant tax implications later in life.

At its heart, an RMD is the minimum amount an account holder must withdraw from certain retirement accounts each year, starting when they reach a specific age. This requirement applies to traditional IRAs, SEP IRAs, SIMPLE IRAs, 401(k)s, 403(b)s, 457(b)s, and other defined contribution plans. Roth IRAs, however, are exempt for the original owner, as contributions to Roth accounts are made with after-tax dollars, and qualified distributions are tax-free. This distinction is particularly relevant for tech innovators who often diversify their investment portfolios across various account types. The intent behind RMDs is to prevent individuals from perpetually deferring taxes on their retirement savings, ensuring that these funds are eventually distributed and taxed during their lifetime. This regulatory framework plays a significant role in the broader financial ecosystem, influencing capital flows and investment strategies, even within the tech sector.

The concept of RMDs also extends to inherited retirement accounts, with specific rules varying based on the relationship of the beneficiary to the original account holder. For a spouse beneficiary, for example, there’s often more flexibility, including the option to roll over the inherited IRA into their own. Non-spouse beneficiaries, however, typically face stricter withdrawal schedules, underscoring the importance of understanding these nuances for comprehensive estate planning, especially for those whose wealth is tied to volatile yet high-growth tech ventures. The complexity of these rules underscores the need for sound financial planning and potentially leveraging innovative financial technology solutions to manage and forecast these obligations effectively.

Who is Subject to RMDs and When They Begin

The obligation to take Required Minimum Distributions is triggered by a combination of factors, primarily the account holder’s age and the type of retirement account involved. Understanding these triggers is fundamental for anyone planning their financial future, especially entrepreneurs and investors in the tech space who often navigate complex financial landscapes.

Historically, RMDs began at age 70½. However, legislative changes through the SECURE Act and SECURE Act 2.0 have shifted this age. For individuals born between 1951 and 1959, RMDs typically begin at age 73. For those born in 1960 or later, the starting age for RMDs is further delayed to 75. This evolving timeline provides a longer tax-deferred growth period for retirement savings, a beneficial aspect for those with significant capital locked in growth-oriented tech investments. It allows for additional years of compound interest, potentially enhancing the overall retirement nest egg.

While most traditional retirement accounts are subject to RMDs, employer-sponsored plans (like 401(k)s) offer a notable exception for individuals still working. If you are still employed by the company sponsoring the plan, you may be able to delay your 401(k) RMDs until you retire, regardless of your age, provided you are not a 5% owner of the company. This “still working” exception does not apply to IRAs. This distinction is particularly relevant for many in the tech industry who often continue working past traditional retirement ages, either as consultants, entrepreneurs, or in leadership roles within innovative companies. Such individuals benefit from expert advice or advanced financial platforms that can track these nuanced eligibility rules.

For inherited IRAs, the rules differ significantly and often require distributions sooner. Spouses generally have the most flexibility, potentially rolling over the inherited IRA into their own and deferring RMDs until their own RMD age. Non-spousal beneficiaries, on the other hand, typically fall under the “10-year rule” for deaths occurring after 2019. This rule generally requires the entire inherited account to be distributed by the end of the tenth calendar year following the year of the original account holder’s death. There are exceptions for “eligible designated beneficiaries” such as minor children, disabled individuals, chronically ill individuals, and beneficiaries not more than 10 years younger than the deceased. Navigating these rules for inherited accounts necessitates detailed planning, especially when dealing with substantial assets, which is common among successful tech sector participants.

The Mechanics of RMD Calculation and Distribution

Calculating and executing Required Minimum Distributions involves specific methodologies and careful adherence to IRS guidelines. Understanding these mechanics is crucial for ensuring compliance and optimizing tax efficiency, especially for individuals whose wealth management strategies might be complex due to diverse investments in the tech and innovation sectors.

The calculation of an RMD is primarily based on two factors: the account balance as of December 31st of the previous year and a life expectancy factor provided by the IRS. For most account holders, the IRS’s Uniform Lifetime Table is used to determine this factor. This table provides a divisor based on your age, which, when divided into the prior year’s account balance, yields the minimum amount that must be withdrawn. For example, if your account balance was $1,000,000 at the end of the previous year and your life expectancy factor from the Uniform Lifetime Table is 27.4, your RMD for the current year would be approximately $36,496 ($1,000,000 / 27.4). For beneficiaries of inherited IRAs, different life expectancy tables or rules (like the 10-year rule) apply, adding another layer of complexity.

It is important to note that if you have multiple traditional IRAs, the total RMD is calculated by summing the year-end balances of all your traditional IRAs. However, you can withdraw the total RMD amount from any one or a combination of your traditional IRAs. This flexibility can be beneficial for strategic tax planning or for consolidating withdrawals. For employer-sponsored plans like 401(k)s, RMDs must typically be calculated and taken separately from each plan, unless the plan explicitly allows for aggregation. This differentiation necessitates a clear understanding of each account type and its specific rules, potentially leveraging advanced financial software to consolidate and manage these obligations seamlessly.

The deadline for taking RMDs is generally December 31st of each year. The first RMD, however, has a special deadline: you can delay it until April 1st of the year following the year you reach your RMD age. While this provides a small window of flexibility, delaying your first RMD means you would have to take two RMDs in that single year—your first (for the prior year) and your second (for the current year). This acceleration of income into a single tax year could potentially push you into a higher tax bracket, diminishing the strategic advantage of deferring. Therefore, careful consideration and potentially professional advice are recommended to weigh the pros and cons of utilizing this delay option, particularly for those with substantial tech-driven income.

Navigating Penalties and Strategic Planning for RMDs

Failing to take a Required Minimum Distribution or withdrawing less than the required amount can result in significant financial penalties from the IRS. Beyond mere compliance, strategic planning around RMDs can also offer opportunities for tax optimization, a critical consideration for individuals with complex financial portfolios often found in the tech and innovation sectors.

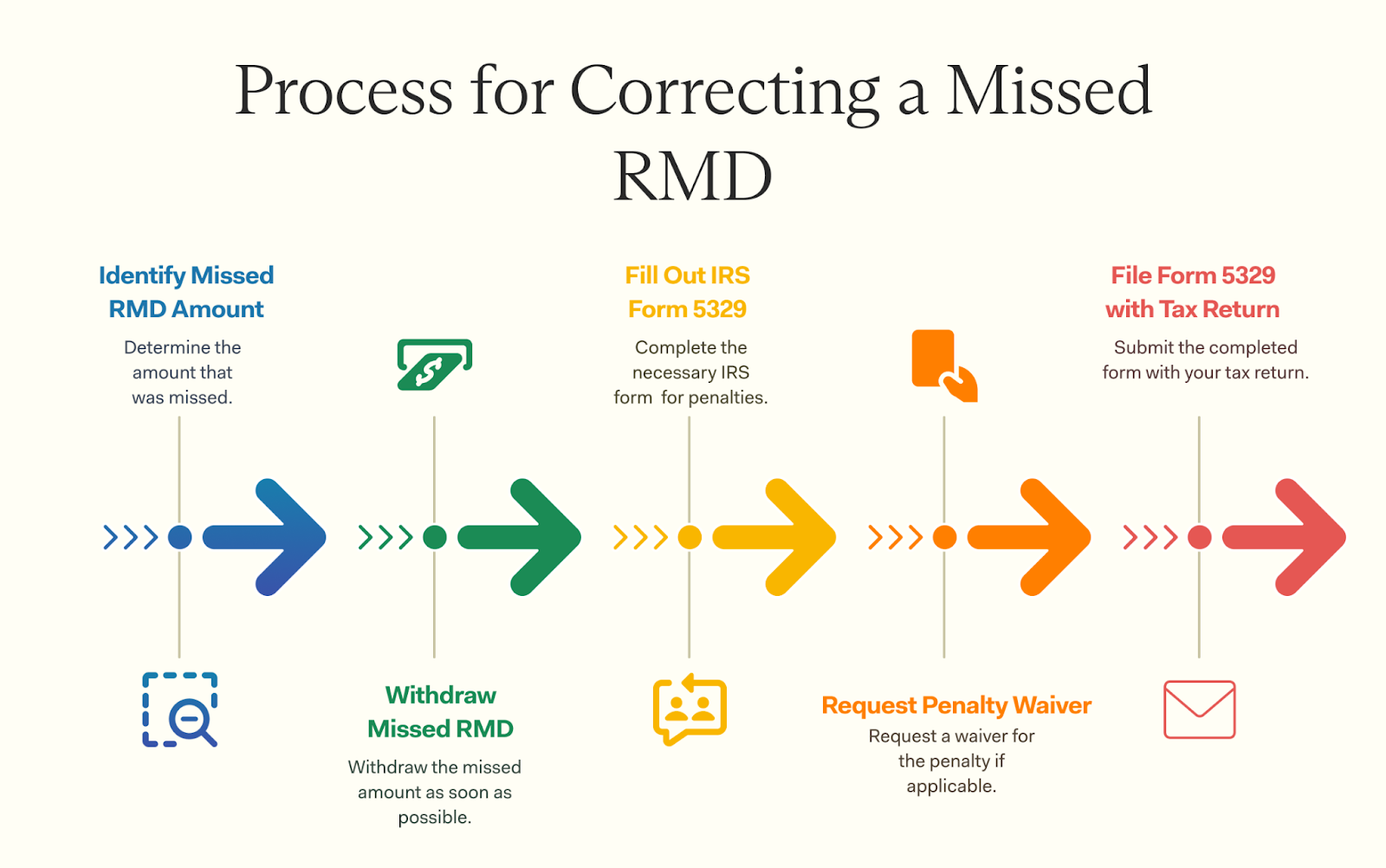

The penalty for not taking an RMD, or for taking an insufficient amount, is a substantial excise tax. Historically, this penalty was 50% of the amount not withdrawn. However, the SECURE Act 2.0 reduced this penalty to 25%, and further to 10% if the taxpayer corrects the shortfall within a specified correction period. While this reduction offers some leniency, it still represents a significant financial loss that is entirely avoidable with proper planning. This penalty underscores the IRS’s serious approach to ensuring timely taxation of deferred retirement assets. For tech entrepreneurs and investors, who might be accustomed to managing high-risk, high-reward ventures, overlooking these seemingly administrative requirements can lead to unnecessary financial setbacks.

Effective RMD management extends beyond merely avoiding penalties; it encompasses strategic tax planning to minimize the overall impact on your financial health. One common strategy is to consider a Qualified Charitable Distribution (QCD). If you are 70½ or older, you can distribute up to $100,000 directly from your IRA to an eligible charity, and this amount can count towards your RMD. A QCD is not included in your gross income, which can be advantageous for tax purposes, particularly for those who are charitably inclined and face substantial RMDs. This approach allows individuals to fulfill their RMD obligations while supporting causes they believe in, without increasing their taxable income.

Another strategic consideration for managing RMDs, especially relevant for those with substantial assets, is the use of Roth conversions. While converting traditional IRA assets to a Roth IRA will trigger an immediate tax liability on the converted amount, it eliminates future RMDs for the owner of the Roth IRA (and potentially for their spouse beneficiary). This strategy can be particularly powerful during years when an individual anticipates being in a lower tax bracket or when they want to proactively manage future tax burdens, especially given the potential for significant appreciation in their tech-related investments. By converting to a Roth, funds grow tax-free and are distributed tax-free, offering substantial long-term benefits. These sophisticated strategies often require the insight of financial professionals who can leverage advanced data analytics and planning tools to model various scenarios, aligning RMD management with broader financial and estate planning goals.