The world of financial messaging is complex and often opaque to those outside of it. Within this intricate system, specific message types serve as the backbone for global transactions. One such crucial message is the MT103. While the title might sound technical and perhaps even intimidating, understanding the MT103 is fundamental for anyone involved in international trade, finance, or even just curious about how money moves across borders. This article will demystify the MT103, exploring its purpose, structure, and significance in the modern financial landscape.

The Role of the MT103 in Global Payments

The MT103, formally known as a “Single Customer Credit Transfer,” is a standardized message format developed and maintained by SWIFT (Society for Worldwide Interbank Financial Telecommunication). SWIFT is a cooperative that provides a network that enables financial institutions worldwide to send and receive information about financial transactions in a standardized and secure manner. The MT103 is one of the most frequently used message types within the SWIFT network.

Core Purpose: Facilitating Funds Transfer

At its heart, the MT103 is designed to instruct a financial institution to transfer funds from one account to another. This transfer can be domestic or, more commonly, international. It serves as the primary vehicle for a bank’s customer (an individual or a business) to initiate a payment order. When you instruct your bank to send money to someone in another country, it’s highly probable that an MT103 message is generated to facilitate this transfer.

Key Information Conveyed

An MT103 message is packed with essential details to ensure the smooth and accurate processing of a payment. These details include:

- Sender’s Information: Details about the remitter (the person or entity sending the money), including their name and account number.

- Beneficiary’s Information: Details about the recipient, including their name, account number, and the bank they hold their account with.

- Amount and Currency: The exact amount of money to be transferred and the currency in which the transaction is to be made.

- Value Date: The date on which the funds are expected to be credited to the beneficiary’s account.

- Ordering Institution: The bank that sends the MT103 message on behalf of its customer.

- Intermediary Banks (if applicable): In international transfers, there might be one or more intermediary banks involved in routing the funds. The MT103 will specify these if necessary.

- Charges Information: Details on who will bear the costs associated with the transfer (e.g., sender pays all, receiver pays all, or shared).

- Remittance Information: This is a crucial field where the sender can provide details about the payment, such as an invoice number, contract reference, or a brief description of the goods or services being paid for. This helps the beneficiary reconcile the payment with their records.

Why SWIFT and the MT103 are Important

Before the widespread adoption of SWIFT and standardized messages like the MT103, international money transfers were a cumbersome and often unreliable process. Each bank had its own proprietary system, leading to delays, errors, and increased costs. SWIFT brought a much-needed layer of standardization and security, making global payments significantly more efficient.

The MT103, as the primary credit transfer message, ensures that:

- Clarity and Consistency: All parties involved in the transaction understand the exact instructions without ambiguity.

- Efficiency: Automated processing of payments is possible, reducing manual intervention and speeding up settlements.

- Security: SWIFT employs robust security protocols to protect the integrity and confidentiality of messages.

- Traceability: The standardized format allows for easy tracking and auditing of transactions.

Deconstructing the MT103 Structure

The MT103, like other SWIFT messages, is structured into various fields, each denoted by a specific tag. These tags are typically three digits long and are preceded by a colon (e.g., :20:). The fields are grouped into different categories, providing a logical flow of information. Understanding these fields is key to comprehending the precise details of a payment.

Key Fields within an MT103

While an MT103 can contain many fields, some are more critical than others and are almost always present. Here are some of the most important ones:

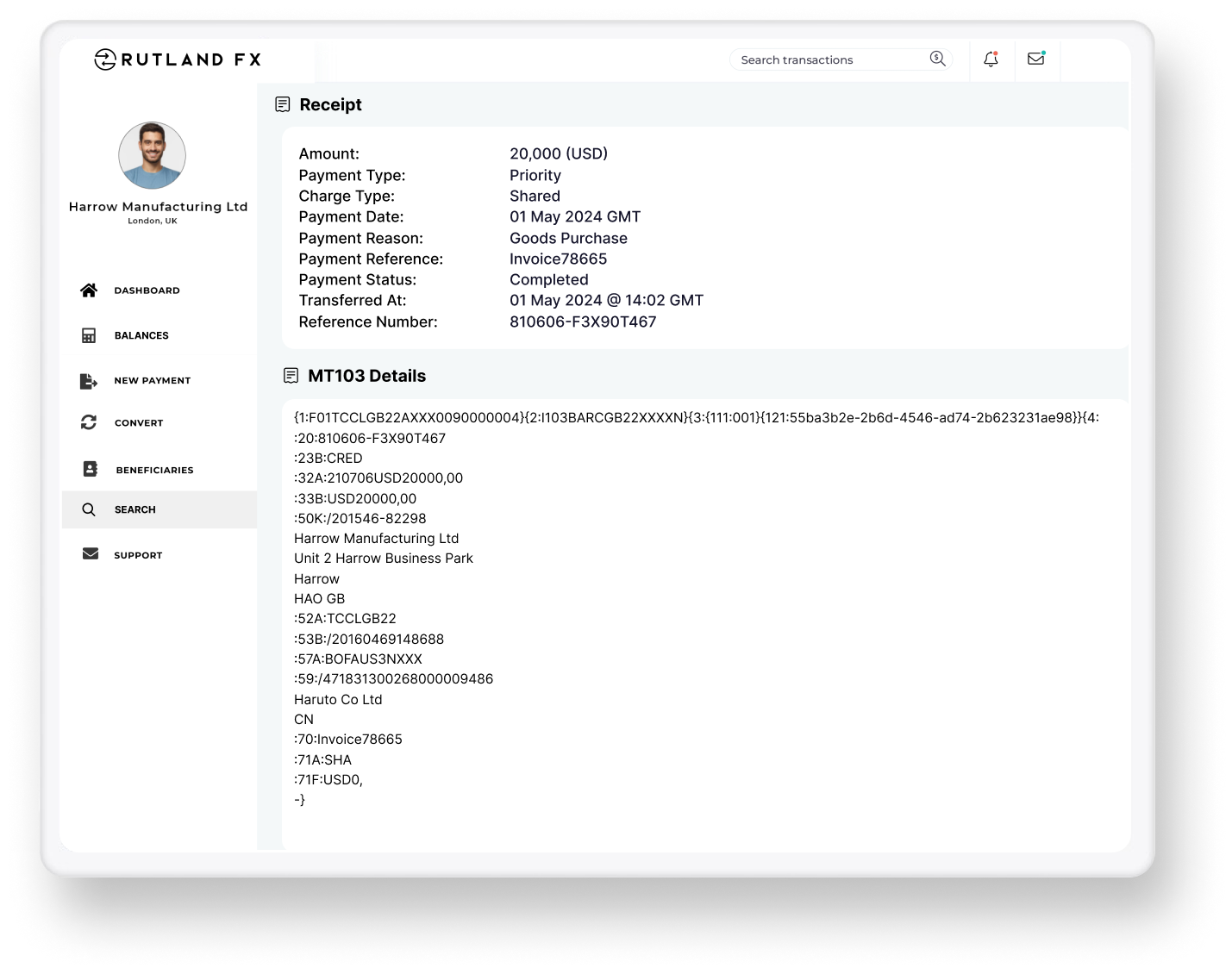

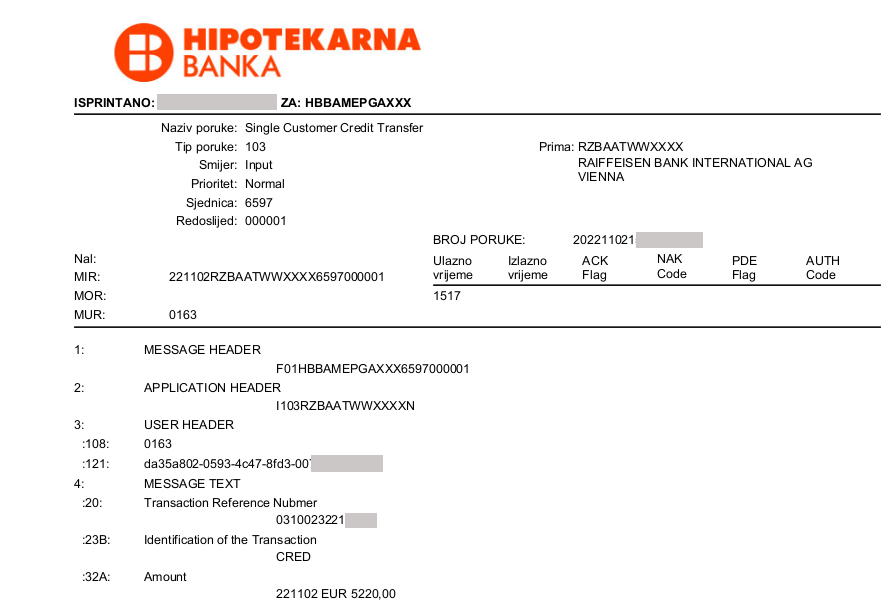

:20: Transaction Reference Number: This is a unique reference number assigned by the sender’s bank to identify the specific transaction. It’s crucial for tracking and referencing the payment.:23B: Bank Operation Code: This code indicates the type of transaction, such as “CRED” for credit transfer.:32A: Value Date, Currency Code, Amount: This field provides the date by which the funds should be available, the currency of the transfer, and the exact amount. For example,231231USD1000,00would indicate a value date of December 31, 2023, in US Dollars, for an amount of 1,000.00.:50: Ordering Customer: This field contains the details of the customer who initiated the payment. It includes their name and address.:52A: Ordering Institution: This specifies the bank that is sending the payment.:59: Beneficiary Customer: This field details the recipient of the funds, including their name and account number. If the account number is not available, it might contain an IBAN (International Bank Account Number) or other relevant identifier.:71A: Details of Charges: This indicates which party is responsible for the transaction charges (e.g., OUR for sender pays, BEN for beneficiary pays, SHA for shared).:70: Remittance Information: This is a free-format field where the sender can provide additional details about the payment. This is where invoice numbers, customer references, or payment descriptions are typically included.

Variations of the MT103

It’s important to note that there are variations of the MT103, such as:

- MT103 STP (Straight Through Processing): This refers to an MT103 message that can be processed automatically by all participating banks without any manual intervention. This requires the message to be perfectly formatted and contain all necessary information in the correct fields.

- MT103 Direct/Customer Transfer: This is the standard customer credit transfer.

- MT103 202: This refers to a specific type of MT103 used for interbank transfers, often referred to as a “MT202 COV” when it’s used in conjunction with a Cover Payment message to provide transparency on underlying customer transfers. This distinction is important for anti-money laundering (AML) and know your customer (KYC) regulations.

The MT103 in the Context of International Trade and Finance

The MT103 plays an indispensable role in the global economy, underpinning a vast array of financial activities.

Supporting Global Commerce

For businesses engaged in international trade, the MT103 is a daily workhorse. When a company imports goods, it uses an MT103 to pay its foreign supplier. Conversely, when a company exports its products, it receives payments via MT103 messages initiated by its international customers. The ability to reliably and efficiently transfer funds across borders is fundamental to the smooth functioning of global supply chains.

Impact on Financial Institutions

Financial institutions rely heavily on the MT103 for their payment processing operations. Banks use these messages to:

- Execute Customer Orders: Fulfilling customer requests for making payments.

- Reconcile Accounts: Matching incoming and outgoing payments.

- Manage Liquidity: Understanding the flow of funds through their systems.

- Comply with Regulations: Providing auditable trails of transactions for regulatory purposes.

Challenges and Considerations

Despite its efficiency, the MT103 is not without its challenges:

- Charges: International transfers can incur significant charges from various banks involved, including correspondent banks. Understanding the

:71A:field is crucial for both sender and receiver. - Delays: While STP aims to minimize delays, issues such as incorrect information in the message, compliance checks, or problems at intermediary banks can still lead to extended processing times.

- Information Scarcity: In some cases, the

:70:remittance information might be too sparse, making it difficult for the beneficiary to identify the payment. - Compliance and AML/KYC: With increasing regulatory scrutiny, banks must ensure that the information provided in MT103 messages, particularly concerning the origin and beneficiary of funds, is accurate and sufficient to meet AML and KYC requirements. This has led to the increased importance of accompanying messages like the MT202 COV when the underlying transfer is for a customer.

The Evolution and Future of Financial Messaging

The MT103, while a cornerstone of current financial messaging, is part of a broader evolution in how financial information is transmitted. SWIFT has been transitioning to a new generation of messaging standards, known as ISO 20022.

The Shift to ISO 20022

ISO 20022 is a more modern, richer, and extensible messaging standard that uses XML (Extensible Markup Language). It offers greater data capacity, improved interoperability, and the ability to convey more complex information compared to the fixed-format MT messages.

Implications for the MT103

As financial institutions migrate to ISO 20022, the traditional MT message formats, including the MT103, will eventually be phased out. New messages, such as the MX messages (e.g., pacs.008 for credit transfers), will replace them. This transition is designed to enhance the efficiency, transparency, and capabilities of global payment systems.

However, the MT103 is likely to remain in use for a considerable period during this transition. Its established prevalence means that a wholesale and immediate replacement is not feasible. The principles behind the MT103 – clear instruction, detailed information, and standardization – will continue to be fundamental, even as the underlying technology and format evolve.

In conclusion, the MT103 is a vital component of the global financial infrastructure, enabling billions of dollars to be transferred daily. Its structured format and SWIFT’s robust network ensure that payments are processed accurately and efficiently. While the financial messaging landscape is evolving, understanding the MT103 provides essential insight into the mechanics of international payments that power global commerce and finance.