Index annuities represent a sophisticated financial instrument within the broader landscape of retirement planning and wealth accumulation. These products, offered by insurance companies, are designed to provide a unique blend of principal protection, tax-deferred growth, and the potential for market-linked returns. Unlike traditional fixed annuities which offer a predetermined, guaranteed interest rate, or variable annuities that directly expose funds to market fluctuations, index annuities derive their interest crediting from the performance of an external market index, such as the S&P 500. This structure aims to capture some of the upside potential of equity markets while insulating the principal from direct market losses. Understanding the mechanics, benefits, and limitations of index annuities is crucial for anyone considering them as part of their long-term financial strategy.

Understanding the Basics of Index Annuities

At its core, an index annuity is a contract between an individual and an insurance company. The individual makes a payment (either a lump sum or a series of payments), and in return, the insurance company agrees to pay out an income stream at a later date, or allow for withdrawals. The distinguishing feature of an index annuity lies in how its growth is determined, connecting it to the performance of a selected stock market index without direct investment in the index itself.

What is an Annuity?

Before delving deeper into the “index” component, it’s important to grasp what an annuity generally entails. An annuity is a long-term investment contract, primarily used for retirement planning. It serves as a vehicle to accumulate funds on a tax-deferred basis and then convert those funds into a guaranteed income stream, often for life. Annuities come in various forms, including immediate versus deferred, and fixed versus variable. An index annuity is a type of deferred annuity, meaning the payouts begin at a future date, allowing the accumulated funds to grow over time. The primary role of annuities in financial planning is to provide a reliable income source during retirement, mitigating the risk of outliving one’s savings.

The “Index” Component

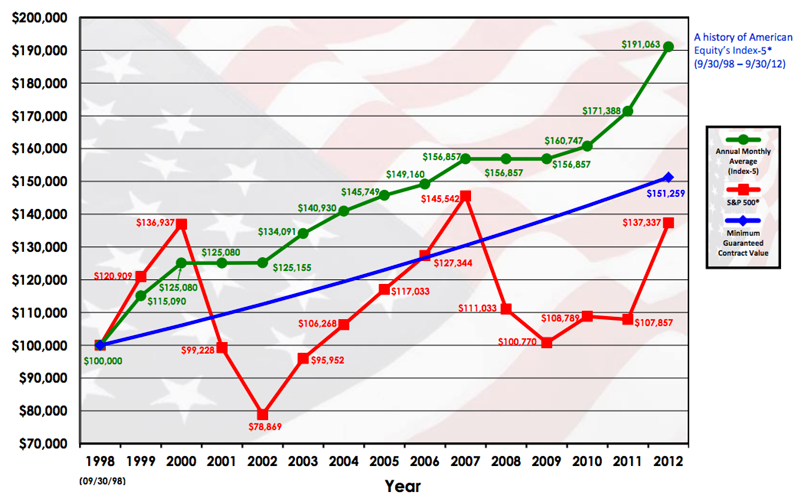

The “index” in an index annuity refers to a specific stock market index, such as the S&P 500, Nasdaq 100, or a custom index developed by the insurance company. Instead of directly investing in the stocks that comprise these indexes, an index annuity credits interest based on a portion of the index’s positive performance. Crucially, if the chosen index declines, the annuity typically guarantees that the principal investment will not lose value due to market downturns. This principal protection feature is a significant draw for risk-averse investors seeking market participation without direct exposure to market volatility. The insurance company achieves this protection by investing a significant portion of the premium in safe, conservative assets (like bonds) to guarantee the principal, and a smaller portion in options linked to the index to capture potential upside.

How Index Annuities Work

The mechanism by which index annuities credit interest is more intricate than a simple correlation to index performance. Various crediting methods and participation limits are employed by insurance companies to manage their risk and define the potential returns for the annuity holder. These features include participation rates, cap rates, spread or margin rates, and floor rates. Understanding these elements is key to evaluating the true growth potential and cost of an index annuity.

Crediting Methods

Index annuities typically use one of several crediting methods to calculate the interest credited to the annuity. The most common methods include:

- Annual Reset: Interest is calculated based on the change in the index from the beginning to the end of each year. Gains are locked in annually, meaning previous gains cannot be lost in subsequent down years.

- Point-to-Point: Interest is calculated based on the change in the index from the annuity’s purchase date (or a specific anniversary) to the end of the contract term (e.g., 5 or 7 years). This method can lead to higher gains if the market finishes strong but also means intervening gains can be lost if the market drops before the measurement period ends.

- Monthly Averaging: Interest is determined by comparing the average of the index’s values over a certain period (e.g., 12 months) to its value at the beginning of the period. This method smooths out market volatility, potentially reducing exposure to sharp market drops but also limiting exposure to rapid upward spikes.

- Monthly Sum: All positive monthly index changes (up to a certain cap) are added together to determine the annual interest credit. Negative months are ignored, contributing zero to the sum, but they do not subtract from previous gains.

Each method has implications for how an annuity performs in different market conditions, and investors should carefully review the specific crediting method offered.

Participation Rate

The participation rate determines how much of the index’s growth is credited to the annuity. For example, if an index increases by 10% and the annuity has a participation rate of 70%, the annuity holder would be credited with 7% interest (70% of 10%). Participation rates can vary significantly between products and may also change at the discretion of the insurance company after an initial guarantee period. A higher participation rate generally allows for greater potential gains from the index’s performance.

Spread/Margin

Some index annuities apply a spread or margin to the index’s performance. This is a percentage that is subtracted from the index’s positive return before any interest is credited. For instance, if an index gained 10% and the annuity has a 2% spread, the effective gain before other limits would be 8%. Spreads effectively reduce the credited interest, acting as an embedded cost within the annuity structure.

Cap Rate

The cap rate is the maximum interest rate an annuity can earn during a specific crediting period, regardless of how well the underlying index performs. If the index gains 15% but the annuity has a 10% cap rate, the annuity holder will only be credited with 10% interest. Cap rates are a key mechanism insurance companies use to limit their risk and ensure profitability, but they also limit the investor’s upside potential in strong bull markets.

Floor Rate

The floor rate is the minimum interest rate the annuity will earn, typically 0%. This is the principal protection feature in action. If the underlying index declines or performs poorly, the annuity’s value will not fall below the previous year’s credited value (minus any withdrawals). The floor rate guarantees that the principal investment is shielded from market downturns, providing a sense of security.

Types of Index Annuities

While often referred to broadly as “index annuities,” these products fall under the umbrella of Fixed Indexed Annuities (FIAs) and can be designed with different primary objectives, such as growth or income generation.

Fixed Indexed Annuities (FIAs)

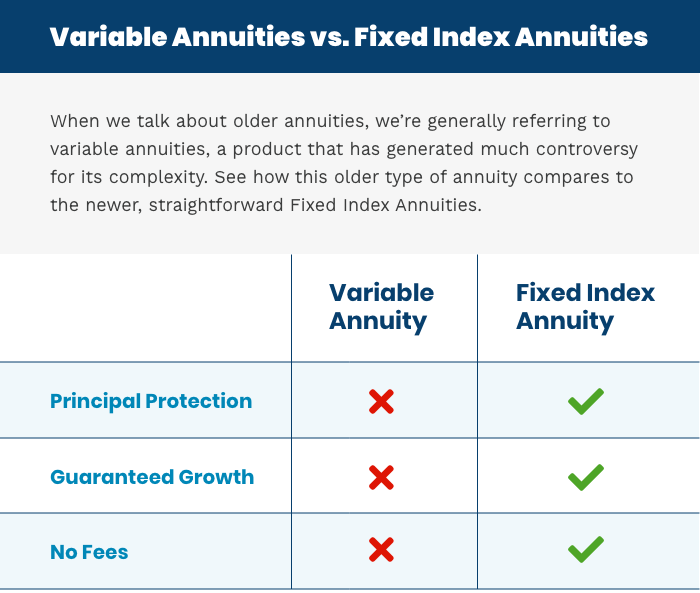

Fixed Indexed Annuities (FIAs) are the most common term for index annuities. They are considered a hybrid product, blending characteristics of fixed annuities (principal protection, guaranteed minimum interest rate) with features reminiscent of variable annuities (market-linked growth potential). FIAs appeal to those who seek more growth potential than a traditional fixed annuity offers but are unwilling to accept the market risk associated with variable annuities or direct stock market investments. They often come with surrender charges for early withdrawals, making them a long-term commitment.

Growth vs. Income Focus

Index annuities can be designed with a primary focus on either wealth accumulation (growth) or guaranteed income during retirement.

- Growth-focused FIAs emphasize maximizing the tax-deferred growth of the initial premium through market participation. They typically have longer accumulation phases and may offer more aggressive crediting methods or higher caps to enhance potential returns.

- Income-focused FIAs often incorporate riders or guaranteed lifetime withdrawal benefits (GLWBs). These riders, usually for an additional fee, guarantee a certain percentage of the annuity’s value can be withdrawn annually for life, regardless of market performance or the annuity’s account value. This feature makes them attractive for individuals concerned about outliving their savings.

The choice between a growth-focused or income-focused FIA depends heavily on an individual’s specific retirement goals and needs.

Pros and Cons of Index Annuities

Like any financial product, index annuities come with a distinct set of advantages and disadvantages that investors must weigh carefully against their personal financial situation and risk tolerance.

Potential Benefits

- Principal Protection: One of the most significant advantages is the protection against market losses. The principal investment is guaranteed not to decline due to negative index performance, offering peace of mind to conservative investors.

- Market-Linked Growth Potential: Index annuities offer the opportunity to participate in stock market gains, providing a higher growth potential than traditional fixed annuities, even with the limitations imposed by caps and participation rates.

- Tax-Deferred Growth: Earnings within an index annuity grow tax-deferred until withdrawal, allowing for compounding returns without annual tax liabilities. This can be a significant advantage over taxable investment accounts.

- Guaranteed Income Stream: Through annuitization or the use of income riders, index annuities can convert accumulated funds into a reliable, guaranteed income stream for retirement, potentially for life.

- Bypass Probate: In many cases, annuity contracts allow for naming beneficiaries, enabling a direct transfer of assets upon death, bypassing the often lengthy and costly probate process.

Potential Drawbacks

- Limited Upside Potential: The cap rates, participation rates, and spreads inherently limit the maximum potential gains an investor can achieve, even in strong bull markets. This means investors might miss out on significant portions of market rallies.

- Complexity and Lack of Transparency: The various crediting methods, rates, and rider options can make index annuities complex and difficult to understand, potentially obscuring the true costs and potential returns.

- Liquidity Constraints: Index annuities are designed for long-term savings. They typically come with surrender charges that can last for several years (e.g., 5 to 10 years), penalizing early withdrawals and limiting access to funds.

- Inflation Risk: While offering principal protection, the capped returns might not always keep pace with inflation over the long term, potentially eroding purchasing power.

- Opportunity Cost: The funds locked into an index annuity cannot be invested in other vehicles that might offer higher returns or greater flexibility.

Is an Index Annuity Right for You?

Deciding whether an index annuity aligns with your financial objectives requires a thorough evaluation of your current situation, future goals, and risk profile. These products are not suitable for everyone and are often best suited for specific types of investors.

Considering Your Financial Goals

Index annuities are generally most appropriate for individuals who:

- Are nearing or in retirement and seek to preserve their principal while still having some potential for growth.

- Are risk-averse and uncomfortable with the direct market exposure of equities or variable annuities.

- Have already maximized contributions to other tax-advantaged retirement accounts (like 401(k)s and IRAs).

- Desire a guaranteed income stream in retirement to cover essential living expenses.

- Are willing to commit their funds for the long term due to surrender charges.

They are typically less suitable for those who need immediate access to their funds, are comfortable with higher investment risk for greater potential returns, or prefer direct investment in market indexes without the limitations of caps and participation rates.

Seeking Professional Advice

Given the complexity and long-term nature of index annuities, it is highly recommended to consult with a qualified financial advisor. A knowledgeable professional can help assess your complete financial picture, explain the intricacies of various index annuity products, compare them with other investment options, and determine if an index annuity fits into your overall retirement strategy. They can also help clarify the specific terms, crediting methods, fees, and riders that apply to any particular product, ensuring you make an informed decision aligned with your individual needs and objectives.