The evolution of technology, particularly within sectors like drone operation and advanced manufacturing, has introduced a complex landscape of financial and operational considerations. One such area that has gained significant attention, especially for businesses integrating sophisticated equipment, is the concept of an “embedded lease.” While the term itself might seem arcane, its implications for accounting, asset management, and strategic planning are profound, particularly for organizations heavily reliant on specialized hardware.

For businesses that leverage advanced technologies such as autonomous flight systems, sophisticated sensor arrays, or high-precision robotic arms, understanding embedded leases is not merely an accounting exercise; it’s a critical component of financial transparency and operational efficiency. As companies increasingly opt for leasing arrangements over outright purchases to manage capital expenditure and maintain technological currency, the distinction between a true lease and a service contract can become blurred. This is where the concept of an embedded lease becomes paramount, requiring a nuanced understanding of contractual obligations and their financial reporting consequences.

Understanding the Fundamentals of Embedded Leases

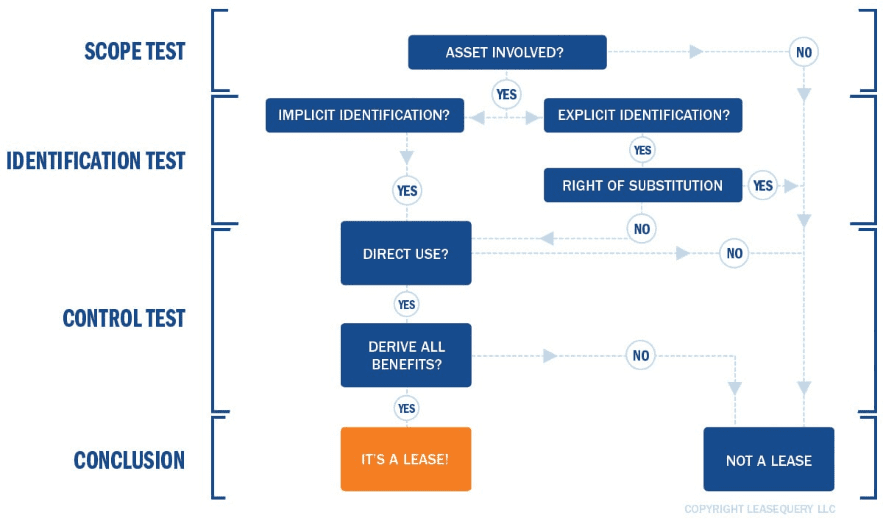

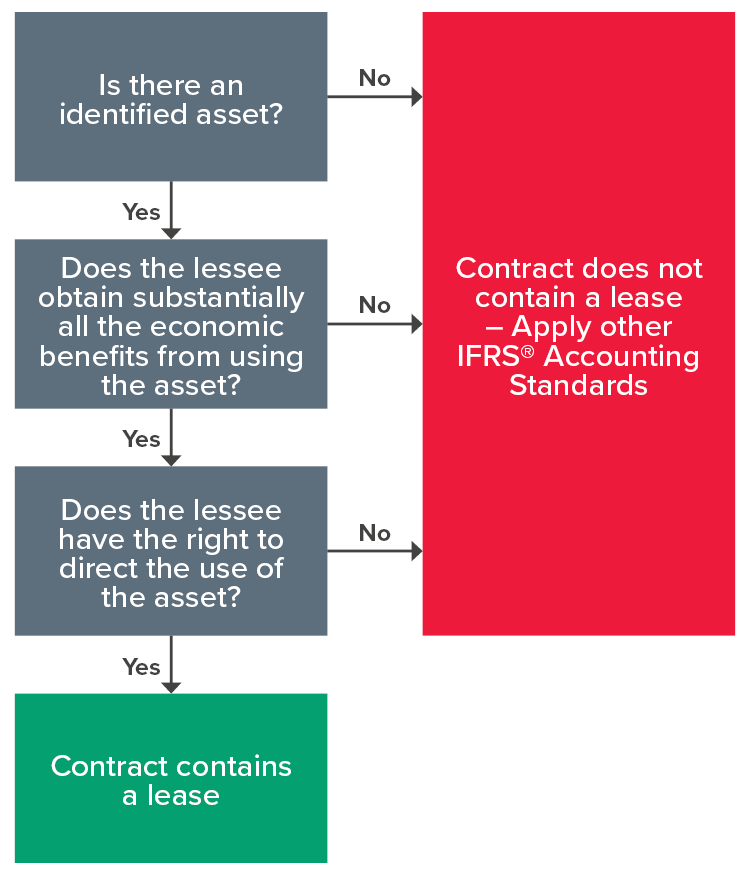

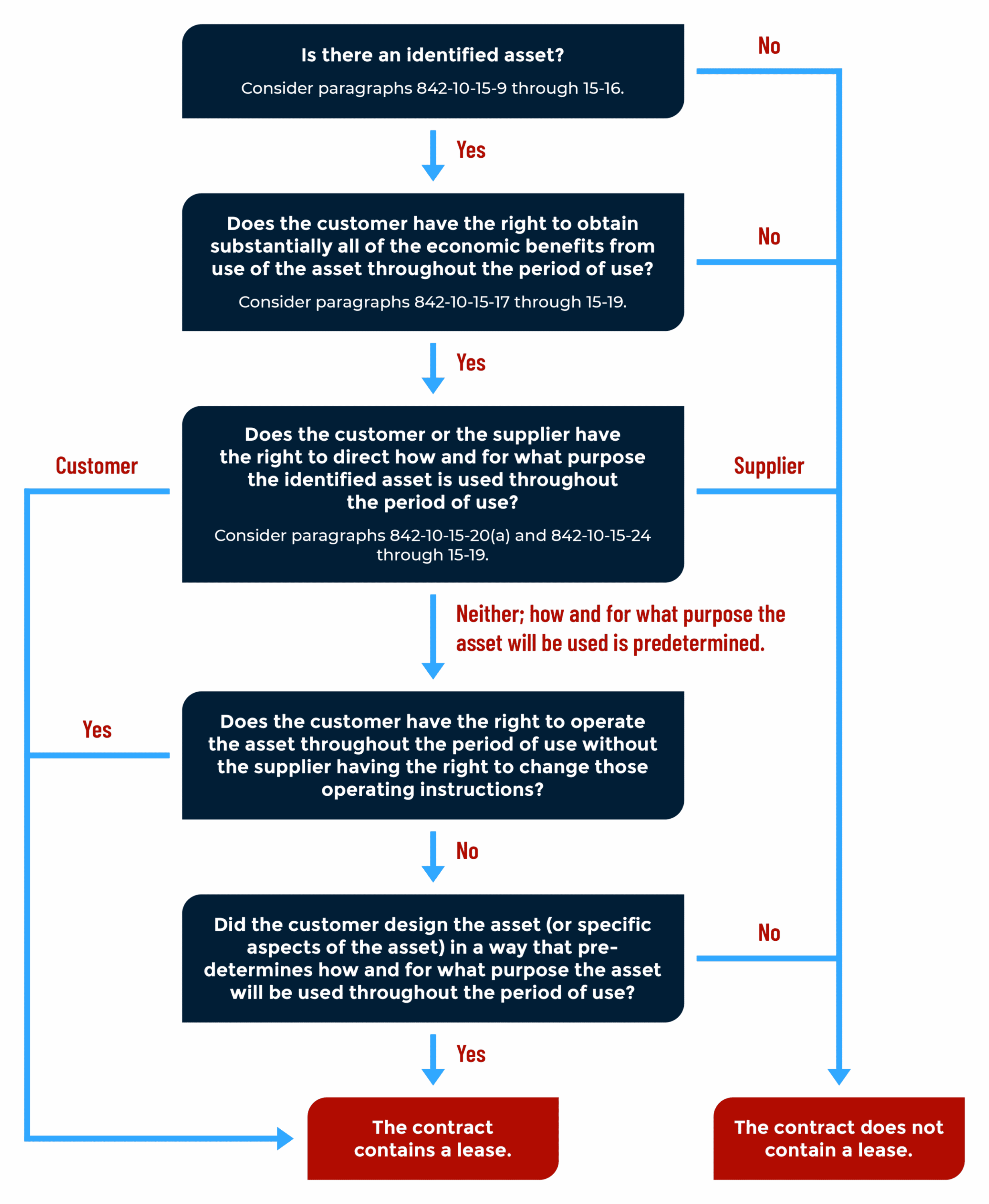

At its core, an embedded lease refers to a contractual arrangement that, while not explicitly labeled as a “lease,” contains terms and conditions that effectively grant a lessee (the user of the asset) the right to control the use of a specific identified asset for a period of time in exchange for consideration. The key phrase here is “control the use of a specific identified asset.” This is a departure from traditional service contracts where the provider retains control and delivers a service, even if it involves the use of their own assets.

The accounting standards governing lease identification, most notably ASC 842 (Leases) in the United States and IFRS 16 internationally, have significantly expanded the scope of what constitutes a lease. These standards aim to bring greater transparency to a company’s balance sheet by requiring lessees to recognize assets and liabilities arising from most leases. Prior to these updates, many arrangements that effectively provided control over an asset were classified as operating expenses. Now, they may need to be capitalized as right-of-use assets and corresponding lease liabilities.

The “Right to Control” Principle

The cornerstone of identifying an embedded lease lies in determining whether the customer has obtained the right to control the use of an identified asset. Accounting standards provide specific criteria to assess this control. Generally, control is obtained if the customer has both:

- The right to direct the use of the identified asset: This means the customer has the ability to determine how and for what purpose the asset is used throughout the period of use. This could involve specifying operational parameters, directing deployment, or modifying operational settings.

- The right to obtain substantially all of the economic benefits from the use of the identified asset: This refers to the ability to derive the majority of the financial advantages that can be obtained from the asset’s use, such as through its output, resale, or lease to another party.

Consider a scenario where a company contracts for advanced aerial surveying services using a specialized drone. If the contract dictates specific flight paths, altitudes, and data acquisition parameters, and the client has the discretion to change these within defined limits, it suggests a right to direct use. If the client is the primary beneficiary of the data collected and can utilize it for their own business purposes without significant further input or cost from the provider, it points to obtaining economic benefits.

Identified Assets: Specificity is Key

For a lease to exist, the asset must be “identified.” This means the asset must be specifically identified in the contract, either by a specific serial number, unique configuration, or by being physically distinct and accessible to the customer. A generic pool of assets from which the provider can choose at their discretion typically does not meet the identified asset criterion.

For instance, a contract for “drone services” might not contain an embedded lease if the service provider uses any available drone from their fleet that meets the general specifications. However, if the contract specifies the use of a particular drone with a unique sensor package or serial number, and the client has specific operational requirements for that exact drone, then it is more likely to be an identified asset.

Common Scenarios and Industry Implications

The implications of embedded leases are particularly relevant in industries that heavily rely on sophisticated technology and often utilize service-based or bundled offerings. For sectors like advanced manufacturing, robotics, and, crucially, the burgeoning drone industry, recognizing these arrangements is vital.

Drones and Autonomous Systems

In the drone sector, companies may enter into agreements for “drone-as-a-service” (DaaS) or bundled solutions that include hardware, software, and operational support. A DaaS agreement might seem like a straightforward service contract. However, if the client dictates specific drone models, customizations, operational parameters, or has the exclusive right to deploy a particular drone for their projects over an extended period, an embedded lease could be present.

- Customized Drone Configurations: If a client commissions a drone with a bespoke sensor payload or specific modifications for a particular project, and the contract grants them the exclusive right to use that customized drone for a set duration, it leans towards an embedded lease. The client is essentially controlling the use of a specific, identified asset.

- Long-Term Operational Contracts: Contracts for continuous aerial monitoring or infrastructure inspection services that involve the use of dedicated drone fleets or specific drones for the client’s exclusive use over several years are prime candidates for embedded leases. The client’s ability to dictate flight schedules, coverage areas, and data acquisition protocols would further strengthen the case for control.

- Software and Hardware Bundles: In complex drone solutions, the hardware (the drone itself) might be bundled with specialized software and operational support. If the contract grants the client control over the use of the drone hardware, even if it’s part of a broader service package, an embedded lease for the drone component may exist.

Robotics and Automation

Similar principles apply to robotic systems in manufacturing or logistics. A company might contract for “robotic automation solutions” that include the installation and maintenance of robots. If the contract specifies particular robots, grants the client the right to direct their operations, and they derive the primary economic benefits, an embedded lease for the robotic equipment could be triggered.

Sensor and Navigation Technology

While sensors and navigation systems are often components of a larger system, specialized agreements for dedicated sensor arrays or advanced GPS/navigation units that are installed for a client’s exclusive use over an extended period could also contain embedded leases. This is particularly true if the client has the ability to direct the calibration, operational modes, or data output of these specific units.

Distinguishing Embedded Leases from Service Contracts

The critical challenge lies in differentiating a true embedded lease from a standard service contract. Service contracts are generally characterized by the provider retaining control over the assets used to deliver the service. The customer is primarily paying for the outcome or the service itself, not necessarily the exclusive use of a specific asset.

Key Indicators of a Service Contract (vs. Embedded Lease)

- Provider’s Ability to Substitute: If the service provider has the practical ability to substitute the asset with another asset that can deliver similar service, and the customer does not have the right to prevent such substitution, it suggests the customer does not control the use of a specific identified asset.

- Provider’s Discretion in Operational Decisions: If the service provider retains significant discretion over how and when the asset is used, and the customer’s role is limited to specifying the desired outcome, it points towards a service contract.

- Customer’s Lack of Economic Benefit Control: If the economic benefits derived from the asset’s use are not substantially all obtained by the customer, or if the provider retains significant residual value or control over the asset’s disposition, it may not be an embedded lease.

For example, a contract for “cloud computing services” is typically a service contract. While it involves the use of computing hardware, the customer does not control specific servers or have the right to direct their use; they are merely consuming processing power and storage. However, if a client contracts for a dedicated server with specific configurations and exclusive access for a set term, it might contain an embedded lease for that server.

Accounting and Reporting Considerations

The identification of an embedded lease has significant implications for financial reporting. Under ASC 842 and IFRS 16, lessees are required to recognize a “right-of-use” (ROU) asset and a corresponding lease liability on their balance sheet for most leases.

The Right-of-Use Asset

The ROU asset represents the lessee’s right to use the underlying asset for the lease term. It is typically measured at the amount of the lease liability, adjusted for any initial direct costs incurred by the lessee, lease payments made at or before commencement, and any incentives received. The ROU asset is then amortized over the lease term or the useful life of the asset, whichever is shorter.

The Lease Liability

The lease liability represents the lessee’s obligation to make lease payments over the lease term. It is measured at the present value of the future lease payments, discounted using the interest rate implicit in the lease or the lessee’s incremental borrowing rate. The lease liability is subsequently reduced by lease payments and increased by interest accretion over the lease term.

Impact on Financial Statements

The capitalization of leases under the new standards leads to:

- Increased Assets and Liabilities: This can significantly alter a company’s balance sheet, affecting financial ratios such as debt-to-equity.

- Recognition of Amortization and Interest Expense: Instead of a single operating lease expense, companies will recognize separate amortization expense (typically straight-line) and interest expense (which is higher in the early periods of the lease).

- Potential for Changes in Key Performance Indicators (KPIs): Financial metrics that rely on metrics like earnings before interest, taxes, depreciation, and amortization (EBITDA) can be impacted, as lease payments previously treated as operating expenses may now be split between interest and amortization.

For businesses in technology-intensive sectors like drone services or advanced automation, meticulously analyzing all significant contractual arrangements for embedded leases is a critical compliance and financial management task. Failure to identify and account for these leases correctly can lead to inaccurate financial statements and potential regulatory scrutiny. The complexity often necessitates collaboration between legal, operational, and accounting departments to ensure proper classification and reporting.