In the ever-evolving landscape of personal finance, understanding the intricate mechanisms that drive growth is paramount. Among the most fundamental yet often misunderstood metrics is the Annual Percentage Yield (APY) associated with savings accounts. Far from being a mere academic concept, APY represents the tangible outcome of technological sophistication applied to financial instruments. It’s the engine that powers the growth of your hard-earned money, a testament to the innovative ways financial institutions leverage data, algorithms, and computational power to offer returns. This article delves into the core of APY, dissecting its components, its significance in the modern financial ecosystem, and how technological advancements continually shape its calculation and application.

Understanding the Mechanics: The Technological Underpinnings of APY

At its heart, APY is a measure designed to provide a standardized and transparent comparison of interest-earning financial products. While seemingly simple, its accurate calculation and presentation are deeply rooted in technological innovation. The shift from simple interest calculations to the compounding methods that define APY is a direct consequence of advancements in computational power and data processing.

The Power of Compounding: An Algorithmic Advantage

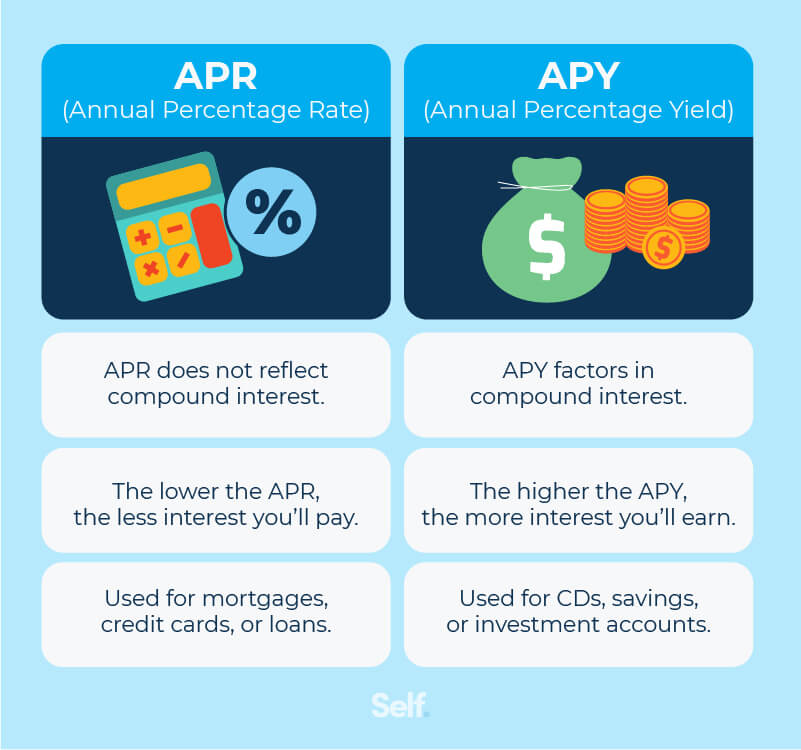

The fundamental difference between APY and its simpler cousin, the Annual Percentage Rate (APR), lies in the concept of compounding. APR represents the simple interest rate applied over a year. APY, on the other hand, accounts for the effect of compounding, meaning that the interest earned is added to the principal, and then future interest is calculated on this new, larger principal. This is where technology plays a crucial role.

Early financial calculations were often manual, making the complexities of frequent compounding cumbersome. However, with the advent of sophisticated algorithms and powerful computing, financial institutions can now precisely model and implement daily, monthly, or even more frequent compounding periods. These algorithms are designed to:

- Track Principal Changes: With each compounding period, the principal amount increases. Algorithms meticulously track these increments, ensuring that the subsequent interest calculation is based on the most up-to-date principal.

- Calculate Interest Accurately: Mathematical functions within these algorithms are employed to calculate the interest for each period based on the prevailing interest rate and the current principal. This accuracy is vital for demonstrating the true growth potential.

- Aggregate and Report: The technology aggregates the interest earned over all compounding periods within a year and presents it as a single, annualized percentage – the APY. This provides a clear, consolidated view of the account’s earning potential, eliminating the need for users to perform complex manual calculations.

The efficiency and precision offered by these technological tools allow for a more accurate reflection of the actual return on investment, making APY a more valuable metric for consumers seeking to maximize their savings.

The Role of Data and Infrastructure

The ability to offer competitive APYs is also heavily dependent on the technological infrastructure of financial institutions. This includes:

- Robust Databases: Large-scale databases are essential for storing and managing customer account information, transaction histories, and interest rate data. These systems must be secure, scalable, and capable of real-time data retrieval.

- Secure Transaction Processing: The technology underpinning transaction processing ensures that interest calculations and account updates are performed securely and without error. This involves intricate systems for authentication, authorization, and data integrity.

- Predictive Analytics and Risk Management: While not directly part of the APY calculation itself, the underlying technological capabilities in data analysis and risk management enable financial institutions to set competitive interest rates. By analyzing market trends, economic indicators, and their own financial health, they can determine rates that are attractive to customers while remaining sustainable for the institution. The ability to process vast amounts of economic data and employ predictive models allows for informed decisions on interest rate setting, directly impacting the APY offered.

Essentially, the technological backbone of a financial institution dictates its capacity to offer efficient, transparent, and competitive savings products, with APY serving as a key indicator of this technological prowess.

APY in the Digital Age: Innovation and Consumer Empowerment

The digital revolution has profoundly impacted how APY is not only calculated but also communicated and utilized by consumers. FinTech innovations have democratized access to financial information and empowered individuals to make more informed decisions about their savings.

The Rise of Online Banks and Digital Platforms

The emergence of online-only banks has been a significant disruptor in the financial industry, largely due to their ability to leverage technology to offer higher APYs. Without the overhead costs associated with physical branches, these institutions can often pass on those savings to their customers in the form of more attractive interest rates.

The technological advantages they possess include:

- Streamlined Operations: Digital platforms allow for highly automated account opening, management, and customer service processes. This reduces operational expenses, freeing up capital that can be directed towards higher APYs.

- Data-Driven Personalization: Advanced analytics enable these institutions to understand customer behavior and preferences, allowing them to tailor product offerings and potentially offer personalized APY structures or bonuses for specific customer segments.

- Agile Rate Adjustments: Digital platforms facilitate quicker and more responsive adjustments to interest rates in response to market changes. This agility ensures that online banks can often remain competitive by swiftly updating their APYs to reflect current economic conditions.

These technological efficiencies translate directly into higher APYs for consumers, making online savings accounts a compelling option for those looking to maximize their returns.

Transparency and Comparison Tools

Technological advancements have also led to the development of sophisticated online tools and comparison websites that allow consumers to easily compare APYs across different financial institutions. These platforms aggregate data, analyze offerings, and present the information in an easily digestible format.

Key technological enablers of these tools include:

- Web Scraping and Data Aggregation: Automated systems can efficiently “scrape” data from financial institution websites, collecting information on savings account features, including APYs. This data is then aggregated into a centralized database.

- API Integrations: Increasingly, financial institutions are using Application Programming Interfaces (APIs) to allow authorized third-party platforms to directly access product and rate information. This facilitates more real-time and accurate data synchronization.

- User-Friendly Interfaces: The development of intuitive web and mobile applications provides consumers with easy-to-use interfaces for filtering, sorting, and comparing savings accounts based on various criteria, including APY, minimum balance requirements, and other features.

- Algorithmic Ranking and Recommendation: Some platforms employ algorithms to rank savings accounts based on their overall value proposition, taking into account APY, fees, and other contributing factors, and may even offer personalized recommendations.

This technological empowerment allows consumers to move beyond passive saving and become active participants in optimizing their financial growth, using APY as a primary metric for making informed decisions.

Future Trends in APY and Savings Technology

The trajectory of APY and savings account technology is one of continuous innovation, driven by advancements in AI, blockchain, and personalized financial management. These trends promise to further refine how savings grow and how financial products are offered.

Artificial Intelligence and Personalized APYs

Artificial intelligence (AI) is poised to play an increasingly significant role in the future of savings accounts and APY. AI’s ability to process vast datasets and identify complex patterns can lead to more sophisticated and personalized financial offerings.

Potential applications include:

- Dynamic APY Adjustments: AI could enable financial institutions to offer dynamic APYs that adjust based on a customer’s overall relationship with the bank, their saving habits, or even their creditworthiness, within regulatory boundaries. This moves beyond a one-size-fits-all approach.

- Predictive Savings Tools: AI-powered tools could proactively advise customers on how to optimize their savings strategy to maximize APY, identifying opportunities for higher interest earnings based on individual financial behavior and market conditions.

- Fraud Detection and Security Enhancements: AI’s advanced pattern recognition capabilities can be employed to enhance the security of savings accounts, detecting and preventing fraudulent activities more effectively, thus protecting the principal on which APY is calculated.

- Automated Financial Advice: AI chatbots and virtual assistants could provide personalized guidance on savings strategies, explaining APY concepts in a clear and accessible manner, and helping users select the most beneficial savings products.

Blockchain Technology and Decentralized Finance (DeFi)

While traditional savings accounts are regulated by central financial institutions, the principles of APY are also being explored and innovated upon within the decentralized finance (DeFi) space, powered by blockchain technology.

- Decentralized Savings Protocols: Platforms built on blockchain technology allow users to deposit digital assets into smart contracts that automatically distribute rewards, effectively acting as a form of decentralized savings account. The “APY” in these contexts is often determined by the protocol’s underlying algorithms and the demand for its services.

- Transparency and Immutability: Blockchain’s inherent transparency means that all transactions and reward distributions can be publicly audited, offering a different form of trust compared to traditional financial systems. The immutable nature of blockchain records ensures that once a transaction is recorded, it cannot be altered.

- Programmable Interest: Smart contracts allow for programmable interest rates, which can fluctuate based on various predefined parameters, offering a dynamic and potentially higher-yield alternative to traditional savings accounts.

While DeFi involves different risks and regulatory frameworks than traditional banking, it represents a significant technological frontier where the concept of earning yield on assets is being fundamentally re-imagined. The technology enabling these protocols is actively pushing the boundaries of what’s possible in financial innovation.

The Continued Evolution of User Experience

Beyond the core calculations and underlying technology, innovation is also focused on improving the user experience of managing savings accounts. This includes:

- Intuitive Mobile Banking Apps: Enhanced mobile applications that provide real-time updates on APY, interest earned, and projections for future growth, making it easier than ever for users to monitor their savings progress.

- Gamification of Savings: Some platforms are exploring gamified approaches to encourage saving, where reaching certain savings milestones or maintaining a consistent saving habit could unlock bonus APY or other rewards.

- Seamless Integration with Other Financial Tools: The future likely holds greater integration of savings accounts with budgeting apps, investment platforms, and other financial management tools, allowing for a holistic view of personal finances and enabling users to make more informed decisions about where to allocate their funds for optimal yield.

In conclusion, APY on a savings account is more than just a percentage; it’s a reflection of the technological advancements that drive financial growth. From the intricate algorithms powering compound interest to the sophisticated digital platforms empowering consumers, technology is at the forefront of making savings more accessible, transparent, and rewarding. As innovation continues to accelerate, we can expect even more dynamic and personalized ways for our money to grow in the future.