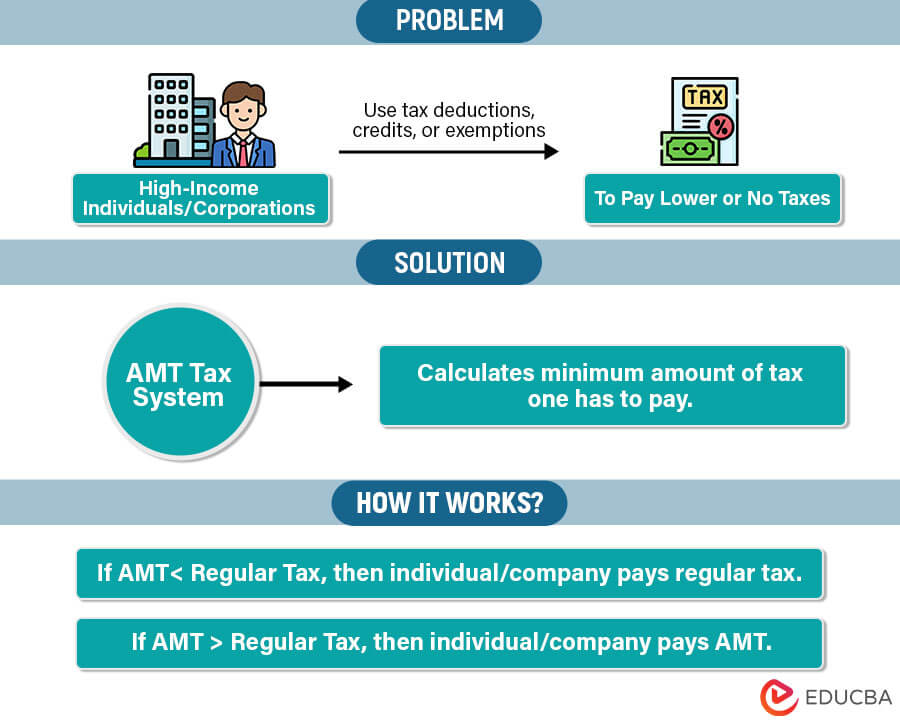

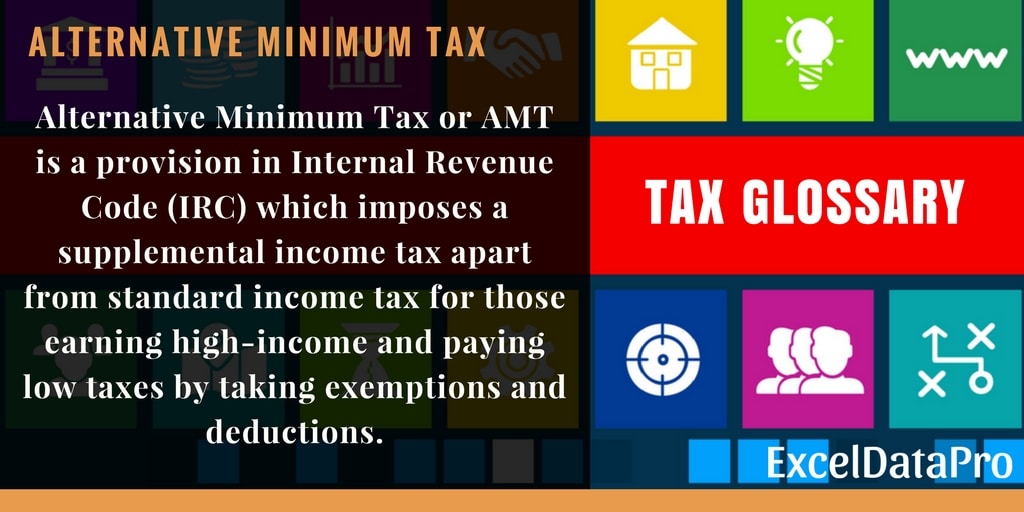

The Alternative Minimum Tax (AMT) is a parallel tax system designed to ensure that high-income individuals and corporations pay at least a minimum amount of tax, even if they utilize numerous deductions and credits that would otherwise significantly reduce their regular tax liability. While the concept of AMT might seem abstract and primarily relevant to tax accountants, understanding its components, including the AMT exemption, is crucial for individuals and businesses navigating their tax obligations. This article delves into the intricacies of the AMT exemption, exploring its purpose, how it functions, who it affects, and the various ways it can be claimed or adjusted.

The AMT exemption is a critical element of the AMT system. It acts as a threshold below which an individual or corporation’s alternative minimum taxable income (AMTI) is not subject to the AMT. In essence, it’s a deduction specifically for AMT purposes, effectively reducing the base upon which the AMT is calculated. Without this exemption, a much broader range of taxpayers would likely fall under the AMT’s purview, leading to a more complex and potentially burdensome tax landscape.

Understanding the Alternative Minimum Tax (AMT)

Before delving into the exemption, it’s essential to grasp the fundamental concept of the AMT itself. The AMT operates alongside the regular income tax system. Taxpayers are required to calculate their tax liability under both systems and then pay the higher of the two. The AMT is triggered when a taxpayer’s “tax preferences” and “adjustments” exceed certain thresholds, which can significantly lower their regular tax bill.

The Purpose of the AMT

The primary objective behind the creation of the AMT was to promote tax fairness and ensure that taxpayers with substantial income did not escape taxation entirely through extensive use of tax shelters, deductions, and credits. Proponents argue that the AMT acts as a backstop, preventing the erosion of the tax base and maintaining a minimum level of contribution from those who can most afford it. It targets situations where the regular tax system might produce an unintendedly low or zero tax liability for wealthy individuals or profitable corporations.

How AMT is Calculated: The Role of Adjustments and Preferences

The calculation of AMT involves taking a taxpayer’s regular taxable income and then making specific adjustments and adding back certain tax preferences. These adjustments and preferences are items that reduce regular taxable income but are considered less essential or more prone to abuse in the AMT framework. Common adjustments include:

- State and Local Tax (SALT) Deductions: While deductible for regular tax purposes, many SALT deductions are disallowed for AMT.

- Miscellaneous Itemized Deductions: Many of these deductions that are limited or disallowed for regular tax purposes are also disallowed for AMT.

- Depreciation Adjustments: Accelerated depreciation methods allowed for regular tax purposes may need to be recalculated using a slower method for AMT, leading to an adjustment.

- Passive Activity Losses: Limitations on passive activity losses for regular tax might differ for AMT.

- Incentive Stock Options (ISOs): The bargain element when exercising ISOs, which is generally not taxed for regular tax until the stock is sold, is often treated as income for AMT in the year of exercise.

These adjustments and preferences increase the taxpayer’s Alternative Minimum Taxable Income (AMTI).

The AMT Exemption: A Crucial Buffer

The AMT exemption is a dollar amount that is subtracted from a taxpayer’s AMTI before the AMT tax rate is applied. This exemption significantly reduces the number of taxpayers subject to the AMT by providing a substantial deduction. Without it, the AMT would likely ensnare many more individuals and businesses whose tax preferences, while legitimate, push their AMTI high enough to trigger the tax.

How the AMT Exemption Works

The exemption amount is not static; it is adjusted annually for inflation. For a given tax year, a taxpayer calculates their AMTI. Then, they subtract the applicable AMT exemption amount to arrive at their “net minimum tax.” This net minimum tax is then subject to the AMT tax rates.

For example, if a taxpayer has an AMTI of $200,000 and the AMT exemption for that year is $70,000, they would subtract this $70,000 to arrive at a taxable amount of $130,000 for AMT purposes. This $130,000 would then be multiplied by the applicable AMT tax rate.

Phase-Out of the AMT Exemption

A critical feature of the AMT exemption is its phase-out. As a taxpayer’s AMTI increases beyond a certain threshold, the exemption amount begins to be reduced. This means that higher-income taxpayers receive a smaller AMT exemption. The phase-out rate is typically 25%.

The phase-out works as follows: For every dollar by which AMTI exceeds the phase-out threshold, the AMT exemption is reduced by $0.25. This continues until the exemption is completely eliminated for extremely high AMTI levels. This mechanism ensures that the AMT continues to serve its purpose of taxing higher earners more effectively, even with the existence of the exemption.

For instance, if the phase-out threshold is $100,000 and a taxpayer has an AMTI of $140,000, their AMTI exceeds the threshold by $40,000. This excess triggers a reduction in their AMT exemption by $40,000 * 0.25 = $10,000. If their full exemption would have been $70,000, it would now be reduced to $60,000.

Who is Affected by the AMT Exemption?

The AMT exemption, and the AMT itself, primarily impacts individuals and corporations who have significant tax preferences or adjustments that reduce their regular tax liability. While the AMT was initially conceived to target very wealthy individuals, changes in tax laws and the indexing of the exemption for inflation have caused its reach to fluctuate over the years.

Individual Taxpayers

For individual taxpayers, the AMT exemption is particularly relevant for those who:

- Have substantial state and local tax (SALT) deductions: Prior to recent federal tax law changes that capped the SALT deduction for regular tax purposes, this was a major driver of AMT for residents of high-tax states.

- Exercise Incentive Stock Options (ISOs): The difference between the market price and the exercise price of ISOs can create a large AMT adjustment.

- Benefit from certain tax credits: Some tax credits that are beneficial for regular tax calculation may not be available or may be limited for AMT.

- Incur significant miscellaneous itemized deductions: While often limited, these can still contribute to AMT.

- Own rental properties and utilize passive activity losses: These can create differences between regular tax and AMT calculations.

The phase-out of the exemption means that higher-income individuals are more likely to experience a reduced exemption and thus be more susceptible to the AMT.

Corporate Taxpayers

Corporations are also subject to the AMT, though the rules and exemption amounts differ. The Corporate AMT was repealed by the Tax Cuts and Jobs Act of 2017. However, it’s important to note that this repeal was for tax years beginning after December 31, 2017, and before January 1, 2027. This means that the Corporate AMT is currently suspended but could be reinstated. When it was in effect, corporations calculated their AMTI and applied an AMT exemption.

The Importance of Tax Planning

Given the complexities of the AMT and its exemption, proactive tax planning is essential. Taxpayers who suspect they might be subject to the AMT should consult with a tax professional. They can help analyze their tax situation, identify potential AMT triggers, and explore strategies to minimize their AMT liability. This might involve:

- Timing the recognition of income and deductions: Shifting certain income or deductions between tax years could help avoid AMT in a particular year.

- Managing the exercise of ISOs: Strategic timing of ISO exercises can be critical.

- Understanding the impact of state and local taxes: While recent federal changes have limited the SALT deduction for regular tax, its disallowance for AMT remains a significant factor.

- Exploring AMT credits: Certain tax payments made in prior years under AMT may generate credits that can offset future AMT liabilities.

Navigating AMT with Tax Law Changes

Tax laws are dynamic, and changes can significantly impact the applicability and calculation of the AMT and its exemption. The AMT exemption has been a subject of frequent legislative adjustments over the years, often with the intent of making it more accessible to middle-income taxpayers or to increase the AMT burden on higher earners.

Legislative History and Adjustments

The AMT exemption has been adjusted numerous times by Congress. These adjustments often occur as part of broader tax reform packages or as standalone legislative acts. The intention behind these adjustments is usually to:

- Preserve the AMT’s intended scope: By indexing the exemption for inflation and adjusting it periodically, lawmakers aim to prevent the AMT from impacting unintended groups of taxpayers due to the erosion of purchasing power.

- Target specific income levels: Legislators may intentionally adjust the exemption levels and phase-out thresholds to focus the AMT on higher-income individuals or to provide relief to middle-income taxpayers.

- Respond to economic conditions: In times of economic uncertainty, tax relief measures, including adjustments to AMT provisions, might be considered.

For instance, in some years, the exemption has been significantly increased to provide widespread relief, while in other periods, it has been maintained at a lower level to ensure the AMT system captures more revenue. The temporary repeal of the Corporate AMT is a prime example of a significant legislative change.

The AMT Credit

For taxpayers who have paid AMT in prior years, they may be eligible for an AMT credit. This credit can be used to reduce their regular tax liability in future years when their regular tax exceeds their tentative minimum tax. The AMT credit is designed to prevent taxpayers from being double-taxed on income that was subject to AMT but is also taxed again under the regular tax system in a later year. This credit is particularly relevant for individuals who experience fluctuations in their income or tax preferences from year to year.

Seeking Professional Guidance

The complexities surrounding the AMT and its exemption, coupled with the ever-changing landscape of tax legislation, underscore the importance of professional tax advice. A qualified tax advisor can:

- Perform accurate AMT calculations: They can precisely determine if a taxpayer is subject to AMT and calculate their potential liability.

- Identify tax planning opportunities: They can advise on strategies to minimize AMT exposure, such as timing income and deductions, or managing investments.

- Navigate complex forms and regulations: Taxpayers can be assured that their AMT calculations and filings are accurate and compliant with current tax laws.

- Advise on the utilization of AMT credits: They can help taxpayers understand and effectively use any AMT credits they may have.

In conclusion, the Alternative Minimum Tax exemption is a vital component of the AMT system, providing a crucial buffer against this parallel tax regime. Understanding its purpose, how it functions, its phase-out mechanism, and the legislative factors that influence it is paramount for taxpayers seeking to manage their tax obligations effectively and avoid unexpected tax liabilities. While the AMT itself can be complex, a clear grasp of its exemption is a significant step towards tax preparedness.