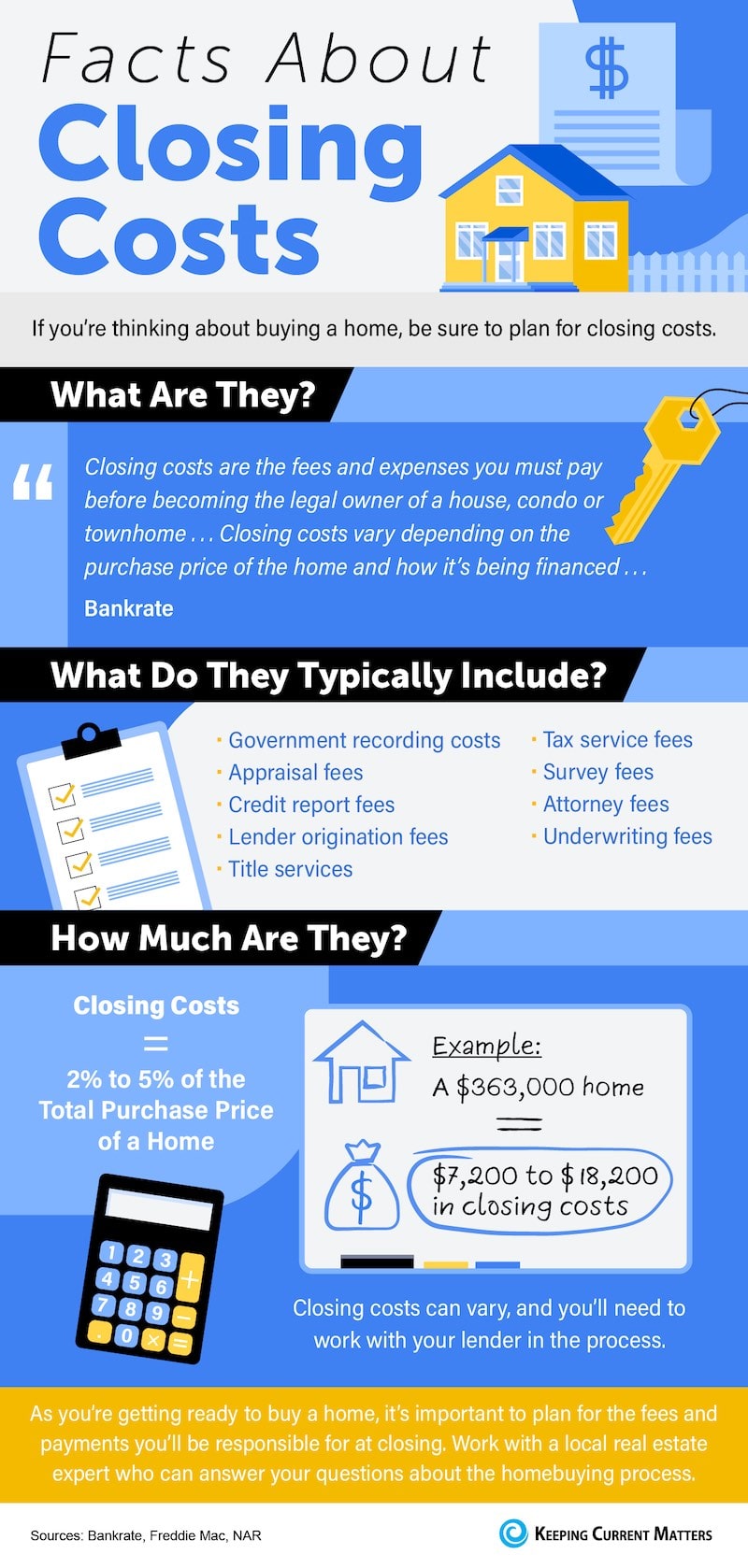

Closing costs are the expenses incurred by buyers and sellers in a real estate transaction, in addition to the property’s purchase price. These costs cover a wide range of services and fees necessary to complete the sale and transfer ownership. Understanding these expenses is crucial for budgeting and financial planning when buying or selling a home.

Understanding the Core Components of Closing Costs

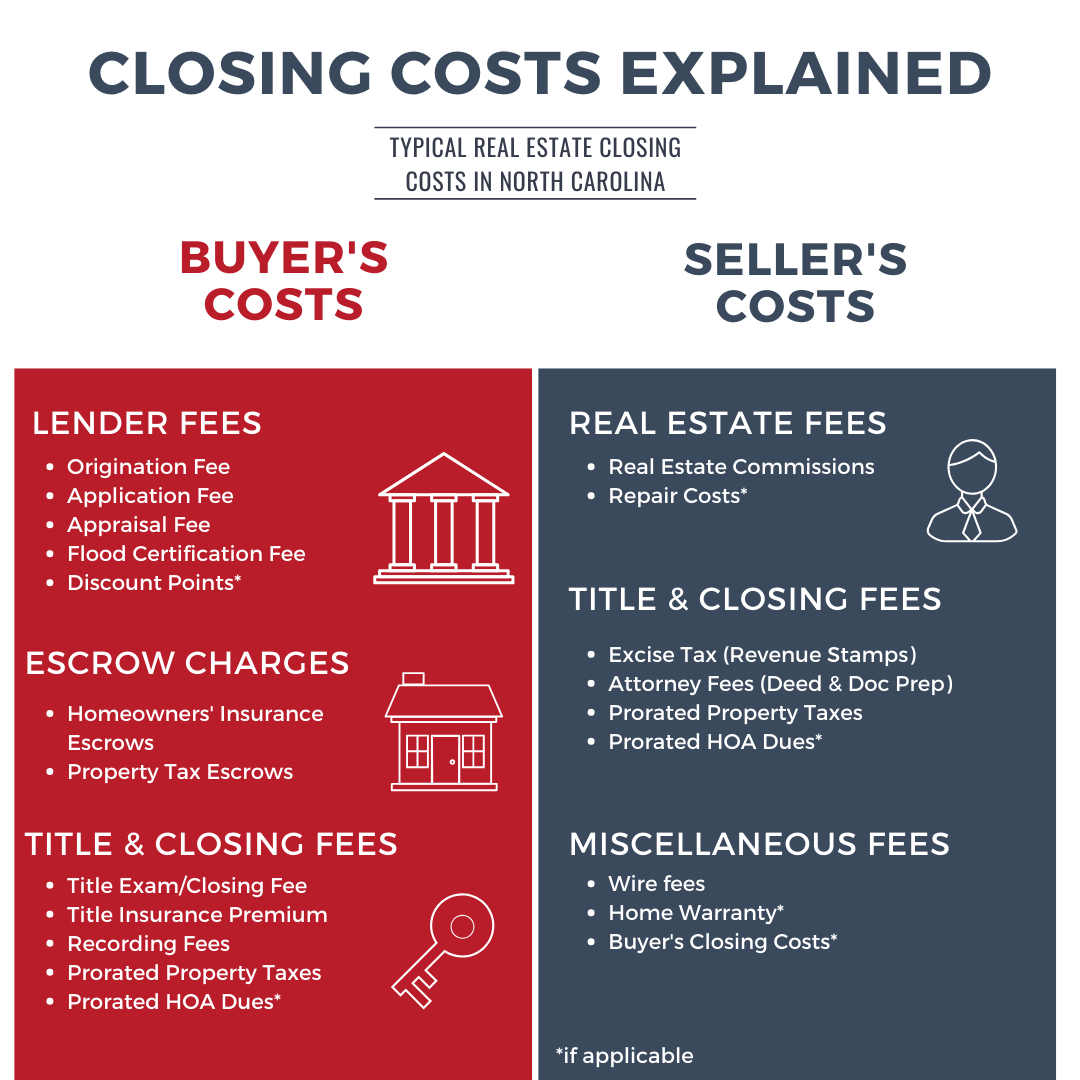

Closing costs represent a significant portion of the overall expense associated with a real estate transaction. They are not a single fee but rather a collection of diverse charges from various parties involved in facilitating the sale. Buyers and sellers often have differing responsibilities for these costs, though negotiations can influence who pays what.

Lender Fees: The Price of Securing Financing

For buyers, a substantial portion of closing costs is directly related to obtaining a mortgage. Lenders charge fees for originating and processing the loan, reflecting the work involved in underwriting, appraising, and managing the financing.

Origination Fee

The origination fee is a charge by the lender for processing the mortgage application. It’s typically a percentage of the loan amount, often ranging from 0.5% to 1%. This fee covers the administrative costs of preparing and underwriting the loan. While it might seem like a single fee, it encompasses several smaller tasks the lender undertakes.

Application Fee

This is a preliminary fee charged when you first apply for a mortgage. It helps cover the initial costs of reviewing your credit report and processing your application. Some lenders may waive this fee, especially if they are offering a promotional rate or if you’ve used them before. It’s a good idea to inquire about this fee early in the process.

Credit Report Fee

When you apply for a mortgage, lenders need to assess your creditworthiness. This fee covers the cost of pulling your credit reports from the three major credit bureaus (Equifax, Experian, and TransUnion). The fee is generally modest, usually between $30 and $50, but it’s an essential step in the loan approval process.

Discount Points

Discount points are fees paid directly to the lender at closing in exchange for a reduced interest rate on the mortgage. One point is equal to 1% of the loan amount. For example, if you take out a $200,000 mortgage and pay two discount points, you’d pay $4,000 at closing. The decision to purchase points depends on how long you plan to stay in the home and the potential savings in interest over time. It’s a strategic financial decision that requires careful calculation.

Private Mortgage Insurance (PMI) or FHA Mortgage Insurance Premium (MIP)

If a buyer makes a down payment of less than 20% on a conventional loan, the lender will typically require Private Mortgage Insurance (PMI). This protects the lender in case the borrower defaults on the loan. PMI is usually paid as a monthly premium, but a portion of the first year’s premium or a lump sum may be due at closing. For FHA loans, a similar insurance is required, known as the FHA Mortgage Insurance Premium (MIP), which can be paid upfront at closing or financed into the loan.

Third-Party Fees: Services Essential for Property Transfer

Beyond the lender, several third-party service providers are involved in a real estate transaction. Their fees are necessary to ensure the property’s title is clear, its value is accurately assessed, and all legal documentation is in order.

Appraisal Fee

An appraisal is an independent assessment of the property’s market value, conducted by a licensed appraiser. Lenders require this to ensure the loan amount does not exceed the property’s worth. The appraisal fee typically ranges from $300 to $600, depending on the property’s size and location. A thorough appraisal is vital for both the buyer and the lender.

Home Inspection Fee

While not always a mandatory closing cost for the lender, a home inspection is highly recommended for buyers. A professional home inspector examines the property’s condition, identifying any potential issues or defects. The fee usually ranges from $300 to $500. This inspection provides buyers with critical information before finalizing the purchase, potentially saving them from costly future repairs.

Title Search and Title Insurance

This is a critical component of closing costs. A title company or attorney conducts a title search to verify that the seller has the legal right to sell the property and that there are no liens, claims, or encumbrances on the title.

Title Search

The title search is the process of reviewing public records to ensure the property’s title is “clear.” This means checking for any past ownership disputes, unpaid taxes, easements, or other legal issues that could affect the property’s ownership.

Title Insurance

Title insurance is a policy that protects the lender and the buyer against financial loss arising from defects in the title that were not discovered during the title search. There are two types: lender’s title insurance (required by the lender) and owner’s title insurance (highly recommended for the buyer). The cost varies based on the property’s purchase price and location, typically ranging from 0.5% to 1% of the loan amount or purchase price.

Survey Fee

In some areas, a property survey is required to confirm the property lines and boundaries. This ensures that no encroachments exist and that the structures on the property are within the legal limits. The cost can range from $300 to $800 or more, depending on the complexity and size of the property.

Attorney Fees

In some states, a real estate attorney is required to be involved in the closing process. Attorneys review all legal documents, ensure compliance with state and local laws, and facilitate the closing. Their fees can vary significantly based on the attorney’s rates and the complexity of the transaction.

Government Fees and Taxes: Statutory Charges

These are fees and taxes imposed by local, state, or federal governments that are part of the real estate transaction. They are often non-negotiable and are essential for the legal transfer of property.

Recording Fees

When a property changes hands, the new deed and mortgage documents must be officially recorded with the local government (usually at the county level). This fee covers the administrative costs of processing and filing these documents, ensuring public record of the ownership transfer. Fees vary by county but are typically in the range of $50 to $200.

Transfer Taxes

Many local and state governments charge a transfer tax when real estate changes ownership. This tax is usually based on the property’s sale price and can be a significant expense. The rate varies widely by jurisdiction, from a fraction of a percent to several percent of the sale price. Who pays this tax (buyer, seller, or split) is often a point of negotiation.

Property Taxes (Prorated)

While not strictly a closing cost in the sense of an upfront fee, buyers are often required to pay a prorated portion of the property taxes at closing. This ensures that the seller pays for the portion of the year they owned the property, and the buyer is covered from the closing date onward. The amount depends on the property’s assessed value and the local tax rate.

Estimating Your Total Closing Costs

Estimating closing costs can be challenging due to the variability of fees, but a general understanding of the percentages involved can provide a helpful benchmark. These estimates are crucial for buyers to secure adequate funds for closing.

The Rule of Thumb: A Percentage of the Loan or Purchase Price

A common guideline is that closing costs for buyers typically range from 2% to 5% of the loan amount for a mortgage. For sellers, closing costs can also be a significant percentage, often ranging from 6% to 10% of the sale price, which includes agent commissions as well as other fees.

Buyer’s Estimated Closing Costs

For buyers, the total closing costs are generally calculated as a percentage of the loan amount. For instance, on a $300,000 loan, closing costs could range from $6,000 to $15,000. This estimate includes lender fees, appraisal, title insurance, recording fees, and prepaid items like homeowners insurance and property taxes.

Seller’s Estimated Closing Costs

Sellers typically face higher closing costs due to real estate agent commissions, which are often the largest single expense. These commissions can range from 5% to 6% of the sale price. In addition to commissions, sellers also incur costs like title fees, escrow fees, attorney fees (if applicable), transfer taxes, and any prorated property taxes or homeowner association dues.

The Loan Estimate and Closing Disclosure: Your Financial Roadmaps

Two essential documents provided by your lender are designed to give you a clear picture of your projected and final closing costs. Understanding these documents is paramount to avoid surprises.

The Loan Estimate (LE)

Within three business days of applying for a mortgage, lenders are required to provide you with a Loan Estimate. This document outlines the estimated interest rate, monthly payment, and estimated closing costs for the loan. It’s designed to be a standardized form, making it easier to compare offers from different lenders. Pay close attention to Section A (Origination Charges) and Section B (Services You Can Shop For), as these are areas where costs can vary.

The Closing Disclosure (CD)

At least three business days before your scheduled closing, you will receive a Closing Disclosure. This document provides the final, binding figures for all your loan terms and closing costs. It’s crucial to compare the Closing Disclosure with your Loan Estimate to ensure accuracy. Any significant discrepancies should be questioned immediately with your lender. The CD details all the fees, who paid them, and when they are due.

Negotiating and Reducing Closing Costs

While some closing costs are fixed, many are negotiable, offering opportunities for buyers and sellers to reduce their overall expenses. Proactive communication and strategic negotiation can lead to significant savings.

Strategies for Buyers to Minimize Expenses

Buyers can employ several strategies to lower their closing costs. These often involve understanding which fees are negotiable and exploring different service providers.

Shopping Around for Lenders and Service Providers

Not all lenders and service providers charge the same fees. Shopping around for a mortgage can reveal significant differences in origination fees, points, and other charges. Similarly, for services like appraisals, title insurance, and home inspections, buyers can often choose their own providers, potentially finding more competitive rates. Always ask for itemized quotes.

Negotiating Lender Fees and Credits

Buyers can attempt to negotiate lender fees, particularly origination fees and discount points. If a lender is eager to secure your business, they may be willing to lower these costs or offer credits towards your closing expenses. Sometimes, asking the seller to contribute towards your closing costs is also an option.

Exploring Seller Concessions

In certain market conditions, sellers may be willing to contribute towards the buyer’s closing costs. This is often referred to as a seller concession and is a negotiated term within the purchase agreement. This can be a valuable tool for buyers who are short on cash for closing.

Strategies for Sellers to Optimize Their Financial Outcome

Sellers also have opportunities to manage their closing costs, particularly by being informed about market norms and potential negotiations.

Understanding Commission Splits and Negotiating Agent Fees

Real estate agent commissions are typically negotiable. Sellers can discuss the commission rate with their agents and explore different commission structures. Understanding how commissions are split between the buyer’s and seller’s agents can also provide leverage.

Reviewing and Challenging Title and Escrow Fees

While title companies set their own rates, sellers can inquire about the breakdown of title and escrow fees and compare quotes from different providers. In some cases, these fees might be slightly negotiable, especially for high-value transactions.

Leveraging Market Conditions

In a seller’s market, sellers generally have more leverage to resist paying buyer closing costs or to negotiate favorable terms for their own expenses. In a buyer’s market, they may be more inclined to offer concessions to facilitate a sale.

Conclusion: Informed Transactions Lead to Successful Homeownership

Closing costs are an integral part of the real estate transaction, representing the essential services and fees required to transfer property ownership. While they can seem daunting, understanding their components, estimating their potential amounts, and actively engaging in negotiation can significantly ease the financial burden. By arming yourself with knowledge about lender fees, third-party services, government charges, and the crucial Loan Estimate and Closing Disclosure documents, you can navigate the closing process with confidence. Ultimately, a well-informed buyer or seller is better equipped to manage these expenses, leading to a smoother, more successful, and financially sound real estate transaction, paving the way for the enjoyment of your new home or the realization of your sale.