The concept of a “simple trust” is a cornerstone of estate planning and personal finance, often discussed in the context of managing assets for beneficiaries. While the term itself might sound straightforward, understanding its nuances is crucial for anyone looking to establish or benefit from such a structure. At its core, a simple trust is a legal arrangement designed to hold and distribute assets for designated beneficiaries, characterized by specific operational requirements and limitations.

The Fundamental Nature of a Simple Trust

A simple trust is defined by its tax treatment and its operational parameters. For tax purposes, a trust is generally considered “simple” if it meets two primary conditions annually: it must distribute all of its income to beneficiaries, and it cannot make any charitable contributions. Additionally, it cannot distribute any of its principal (corpus) to beneficiaries. This distinction is vital because it dictates how the trust’s income is taxed and where the tax burden ultimately falls.

Income Distribution Requirements

The most defining characteristic of a simple trust is the mandate to distribute all its income annually. This income can include dividends from stocks, interest from bonds or savings accounts, rental income from properties held within the trust, and any other earnings generated by the trust’s assets. The trustee is legally obligated to ensure that every penny of this income is paid out to the named beneficiaries within the tax year it is received. Failure to distribute all income means the trust would no longer qualify as a simple trust for that year and would be treated as a complex trust, with different tax implications.

Prohibitions on Principal Distributions

Unlike more complex trust structures, a simple trust explicitly prohibits the distribution of its principal to beneficiaries during the trust’s existence. The principal, also known as the corpus, refers to the original assets transferred into the trust, such as the initial cash, securities, or real estate. While the income generated by these principal assets must be distributed, the assets themselves are intended to remain within the trust until its termination, as stipulated by the trust document. This feature makes simple trusts ideal for long-term wealth preservation and for ensuring that the underlying assets are preserved for future generations or for a specific eventual purpose.

No Charitable Contributions

Another critical defining feature of a simple trust is the inability to make charitable contributions. If a trust document allows for distributions to charitable organizations, or if the trustee makes such distributions, the trust will be classified as a complex trust. This limitation is a key differentiator from other trust types that may have provisions for philanthropic giving as part of their objectives.

Key Advantages and Applications of Simple Trusts

The restrictive nature of a simple trust, while seemingly limiting, offers significant advantages and makes it a preferred choice for specific estate planning goals. Its simplicity in operation and tax treatment often translates into lower administrative costs and greater predictability for both the grantor (the person creating the trust) and the beneficiaries.

Asset Management and Preservation

Simple trusts are excellent tools for managing and preserving assets over extended periods. By keeping the principal intact, they ensure that the core wealth remains shielded from premature depletion. This is particularly useful when the grantor wishes to provide ongoing financial support to beneficiaries without enabling them to spend down the inherited capital. For example, a parent might set up a simple trust to provide for their children’s education and living expenses throughout their college years, ensuring that the funds are used for their intended purpose and that the principal is still available for other future needs or inheritance.

Avoiding Probate

One of the most significant benefits of establishing any trust, including a simple trust, is its ability to avoid the probate process. When an individual passes away, their assets are typically subject to probate, a court-supervised process that can be time-consuming, expensive, and public. Assets held within a trust, however, are not part of the deceased’s probate estate. Upon the grantor’s death, the trustee can distribute the trust assets directly to the beneficiaries according to the trust’s terms, bypassing probate entirely. This ensures a more private, efficient, and often faster transfer of wealth.

Tax Efficiency (for Beneficiaries)

While the trust itself may have certain tax reporting requirements, the income distributed from a simple trust is generally taxed at the beneficiary’s individual income tax rate. This can be more tax-efficient than if the income remained within the trust, where it might be subject to higher trust tax rates. By passing the income directly to the beneficiaries, the tax burden is effectively shifted to those individuals who are likely in a lower tax bracket than the trust itself might face if it retained the income.

Flexibility for Specific Needs

Despite its restrictions, a simple trust can be tailored to meet specific needs. For instance, it can be established to provide for a minor child until they reach a certain age, or to support a dependent relative who may not be financially responsible enough to manage a large inheritance directly. The trustee’s role is to ensure that the distributed income is used for the beneficiary’s benefit as outlined in the trust agreement.

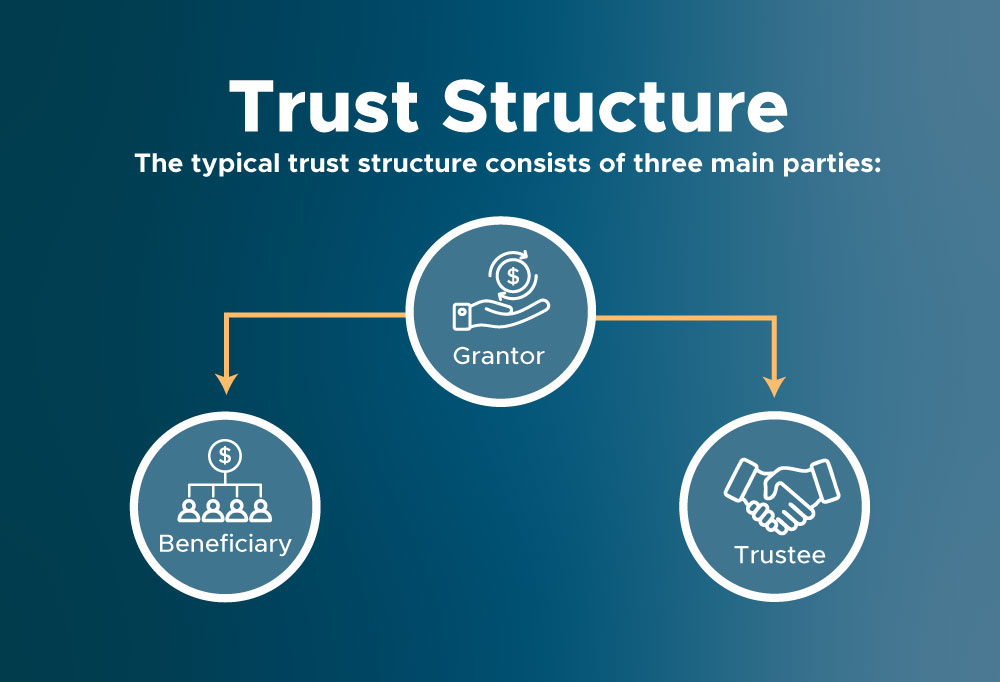

The Trustee’s Role and Responsibilities

The trustee is the central figure in administering a simple trust. This individual or entity is entrusted with the legal ownership of the trust assets and is responsible for managing them according to the grantor’s wishes and the terms of the trust document. For a simple trust, the trustee’s duties are clear but require diligent adherence.

Fiduciary Duty

A trustee owes a fiduciary duty to the beneficiaries of the trust. This is a legal obligation to act in the best interests of the beneficiaries with utmost good faith, loyalty, and prudence. This duty encompasses several key responsibilities, including:

- Duty of Loyalty: The trustee must act solely in the interest of the beneficiaries, avoiding any self-dealing or conflicts of interest.

- Duty of Prudence: The trustee must manage the trust assets with the care and skill that a reasonably prudent person would exercise in managing their own affairs. This involves making sound investment decisions and safeguarding the assets.

- Duty to Administer Impartially: If there are multiple beneficiaries, the trustee must treat them impartially, ensuring that the benefits and burdens of the trust are distributed fairly.

Income Distribution

As highlighted earlier, a primary responsibility of the trustee in a simple trust is to ensure that all income generated by the trust is distributed to the beneficiaries annually. This requires meticulous record-keeping to track all income received and to ensure timely disbursement. The trustee must also understand the definition of “income” as it applies to the trust’s assets and relevant legal statutes.

Record Keeping and Tax Reporting

Trustees are responsible for maintaining accurate records of all trust transactions, including income received, expenses paid, and distributions made. This is essential for proper accounting and for fulfilling tax reporting obligations. A simple trust generally does not pay income tax on the income it distributes because that income is reported on the beneficiaries’ tax returns. However, the trust itself may still need to file an annual informational tax return (Form 1041 in the United States) to report its activities.

Investment Management

While a simple trust does not distribute its principal, the trustee is still responsible for prudently managing and investing the trust’s assets to generate income. This involves understanding investment strategies, diversifying assets to mitigate risk, and making investment decisions that align with the trust’s objectives and the beneficiaries’ needs. The trustee must always act with a view to preserving the principal while maximizing income generation.

Distinguishing Simple Trusts from Complex Trusts

The distinction between simple and complex trusts is fundamental in estate planning and taxation. Understanding these differences is crucial for choosing the right trust structure for specific financial goals.

Complex Trusts Defined

A complex trust, in contrast to a simple trust, has more flexibility in its distribution powers and tax treatment. A trust is considered complex if it:

- Distributes income to beneficiaries, but not necessarily all of it.

- Can distribute principal to beneficiaries.

- Makes charitable contributions.

- Is established for the care of an animal.

Key Differences Summarized

| Feature | Simple Trust | Complex Trust |

|---|---|---|

| Income Distribution | Must distribute all income annually | May distribute some or all income annually |

| Principal Distribution | Cannot distribute principal during its existence | May distribute principal to beneficiaries |

| Charitable Gifts | Cannot make charitable contributions | Can make charitable contributions |

| Tax Treatment | Income taxed to beneficiaries | Income taxed to trust or beneficiaries, depending on distribution |

| Flexibility | More restrictive, focused on income distribution | More flexible, broader distribution powers |

| Administrative Needs | Generally simpler administration | Can involve more complex administration and accounting |

The choice between a simple and a complex trust depends heavily on the grantor’s objectives. If the primary goal is to provide steady income to beneficiaries while preserving the original capital, and there is no intention for charitable giving, a simple trust is often the most appropriate and efficient choice. If, however, the grantor wishes to grant the trustee discretion over income and principal distributions, or intends to support charitable causes, a complex trust offers the necessary flexibility.

Conclusion: The Enduring Value of Simplicity

In the intricate landscape of estate planning, the “simple trust” stands out for its clarity of purpose and straightforward operational requirements. While its name suggests a lack of sophistication, its design offers powerful benefits for asset preservation, efficient wealth transfer, and predictable income support for beneficiaries. By adhering to its core principles – distributing all income annually, preserving the principal, and refraining from charitable gifts – a simple trust provides a robust framework for managing wealth in a manner that aligns with the long-term financial well-being of its designated recipients. Its ability to bypass probate further solidifies its position as a valuable tool for individuals seeking to secure their financial legacy with an emphasis on clarity, control, and enduring value.